Basiq and Ernst and Young Australia have teamed up to write a comprehensive white paper looking at the future of Write Access in Australia.

It compares and contrasts two implementations of Write Access for third party payment initiation, proving that the Consumer Data Right is a world leading piece of legislation, drawing upon lessons from the UK and EU.

What are some of the key takeaways from the White Paper?

Payment initiation – The most common form of payment initiation is direct debit but this doesn’t leverage data to ensure payment success. Two new approaches have emerged to solve for this with the NPP & CDR Action Initiation.

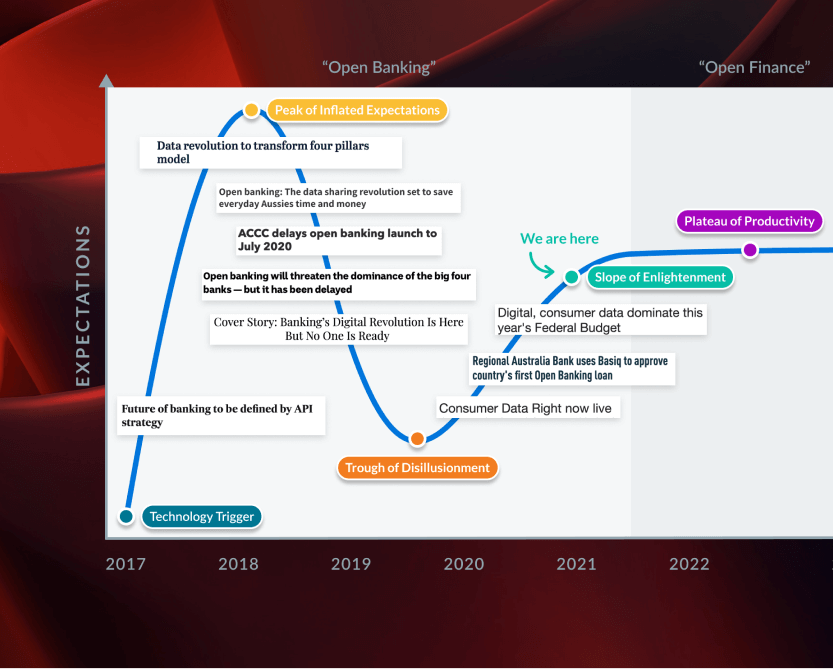

Evolution of Open Banking – Open Banking enables consumers to freely share their consented financial data with trusted third parties. The CDR is currently predicated on ‘read access’ only.

Benefits of smart payments – The use of data in executing payments eliminates many issues currently faced with direct debits. These include the elimination of dishonour fees, avoiding failed payments and reducing the incidence of fraud.

The Australian Consumer Data Right (CDR) is designed as an exceptionally forward-thinking policy. However we are only scraping the surface of its potential.

This white paper takes a forward looking view at the Open Banking regime’s future, cemented in four novel use cases.

What are some of the key takeaways from the White Paper?

Novel use cases – New use cases will emerge at the intersection of insights and action. These include Rules and event-based payment initiation, Dynamic credit risk decisioning and Autonomous personal finance.

Towards Open Banking – Historically, consumers have only had the ability to interact with their data via technology known as ‘screen scraping’ but the roll out of Open Banking has accelerated.

What the future holds – Open Banking will be bedded down over the next five years. As the CDR moves into other sector such as energy and telco, innovation will accelerate at an economy wide level.

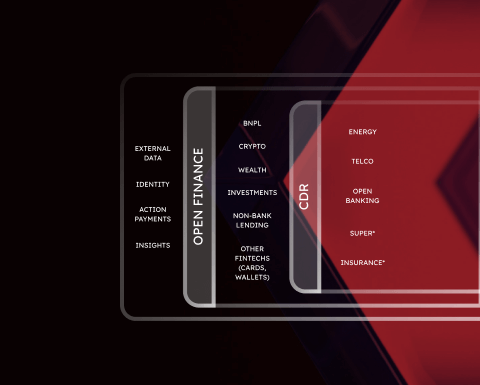

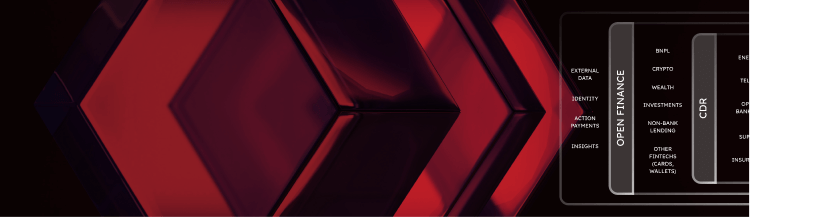

‘Open Finance’ is a term used to describe the accessibility of core financial services made available through APIs. This allows for the sharing of data across multiple financial institutions driven by consumer consent, as well as being able to do something with that data once shared, such as a payment.

The following white paper visualises what a truly Open Finance ecosystem looks like, with references drawn to Australia where necessary to add additional context.

What are some of the key takeaways from the White Paper?

Open Finance ecosystem model – An interconnected Open Finance ecosystem requires the core layers of Data, Insights and Actions. The proposed model outlines how the core layers interact with other inputs and outputs in the broader economy.

Open Finance components – There are four critical components that are required to create and enable an Open Finance ecosystem. This includes consent, data, insights and actions.

Benefits of Open Finance – While complex, Open Finance presents benefits to consumers including increased consumer empowerment, innovation and competition, increased financial literacy and consumer choice.

As more financial institutions share data via Open Banking, there are specific requirements when it comes to both access and usage. Ensure you’re prepared for the transition by considering the key areas including your UX, Accreditation and Security.

Your handy guide + checklist and prepare for your transition to receiving Open Banking data

Accreditation

In order to use Open Banking under the Consumer Data Right, organisations must choose a pathway for participation in the CDR from a range of models. Which model is best for your organisation?

User Experience

Customer consent underpins the CDR, so the communication of consent along the customer journey is critical. Also what is the actual experience like when it transitions from your app to the banks’ app to sign in?

Security

The CDR sets out specific requirements on the level of security you need in order to be able to use Open Banking data. What documentation do you have and what controls are in place?

We are proud to announce the launch of our improved affordability solution – Basiq Insights. Leveraging a variety of data sources including Open Banking, our uplifted Insights solution offers a holistic approach to financial data analysis and decision making in the lending industry by bringing together the power of Basiq’s API with the simplicity of a no-code dashboard.

Navigating the complexities of modern lending

In today’s rapidly evolving financial landscape, lenders face a multitude of challenges that can hinder their efficiency and effectiveness. From the intricacies of regulatory compliance to the need for technological agility, these challenges demand innovative and adaptable solutions. Basiq Insights emerges as a pivotal tool in addressing these complexities. Let’s explore some of the key challenges in the lending space and how Basiq Insights provides effective solutions:

Manual Assessments and Accuracy Issues: Automated solutions reduce the reliance on manual methods, enhancing accuracy and security.

Disjointed Customer Experience: Streamlined data processing improves the customer journey in loan applications.

Navigating Regulatory Obligations: Compliance becomes more manageable with automated data handling and open banking integration.

Overcoming Technological Limitations: The combination of API and no-code dashboard ensures that lenders are not left behind due to outdated tech stacks.

Screen scraping regulations: With Treasury considering the ban of screen scraping of financial data from bank accounts. Lenders using decisioning platforms that solely rely on screen scraping will be left without access to their customers’ financial information as banks move to use Open Banking.

Powerful APIs for bespoke decisioning Basiq’s API forms the backbone of the affordability solution, allowing lenders to delve deep into financial data with enriched transaction details, ensuring precise and reliable insights tailored to their specific needs.

It is an unparalleled tool, empowering you to create bespoke decision making for your customers that align with your specific use case. It boasts the most comprehensive library of data points, metrics and categories available in the market, enabling you to go beyond using templated reports from conventional providers.

Basiq’s No-Code Dashboard – empowering teams beyond development The no-code dashboard revolutionises the experience for non-developer teams. Designed for seamless integration with the API or as an independent solution, it simplifies interaction with Basiq’s robust reporting API. The dashboard provides access to data aggregation, enrichment, and insights, all without requiring specialised coding skills or the development of custom applications. Its user-friendly interface bridges the gap between complex data handling and operational ease, enabling you to focus on creating value for your end users.

Key features of Basiq Insights: Consumer Affordability reporting solution

Across the Basiq API and Dashboard you can access a range of features and capabilities.

Access to data from CDR, Web connectors & Uploads: Future proof your solution by accessing web connectors (screen scraping) and Open Banking via a single platform. Be prepared to make the switch when banks transition away from screen scraping and leverage even more data insights with Open Banking.

Extensive data library: Includes thousands of data points, over 60 groups, 50+ metrics, and more than 500 merchant categories, continually updated for comprehensive reporting.

Comprehensive transaction data access: Offers access to over 12 months of transaction data from various financial institutions, providing a detailed view of a customer’s financial health.

Advanced data categorisation: Features enriched transaction details, including merchant, location, and category, with expenses categorised into more than 500 categories based on ANZSIC classifications for detailed spend behaviour analysis.

Customisable reporting: Allows for the generation of customised reports to meet unique decisioning criteria using a growing library of data points and metrics.

Enhanced decisioning tools: Includes a continuously expanding set of groups and metrics to refine decision-making processes.

Consolidated multi-account reporting: Integrated consent UI enables consolidated reporting across multiple bank accounts, allowing for individual or combined reports for multiple applicants.

Predefined Risk Flags: Benefit from our extensive library of risk flags, meticulously designed for comprehensive decisioning. These predefined flags are instrumental in identifying gaps in financial information, ensuring thorough and accurate assessments in your lending processes.

Powerful enrichment overlay services: Utilises machine learning for transaction cleansing and categorization, enhancing data quality for deeper insights.

Export options: Provides the ability to export reports in PDF or CSV formats for record-keeping and detailed transaction analysis.

Bank statement export capability: Enables easy export of bank statements to support lending decisions.

Transforming lending with Basiq Insights

Basiq Insights stands as a beacon of innovation in the financial sector, particularly in the realm of lending. Seamlessly blending the technological prowess of its API with the accessibility of a no-code dashboard, this solution not only meets the current demands of the lending industry but also anticipates its future needs.

Basiq Insights is not just a tool but a comprehensive solution, tailored to meet the diverse needs of the modern lending landscape. With its array of advanced features, it offers unparalleled depth and breadth in financial data analysis and reporting across its API and No-Code Dashboard solutions. Here’s a look at some of the key features that make Basiq Insights a leader in its field:

Enhanced Loan Processing Efficiency: Automation and real-time data access lead to faster and more accurate loan decisioning.

Data Enrichment and Classification: Enhanced transaction details for precise financial assessments.

Customer Consent Management: Ensuring data privacy and compliance.

Tailored Financial Insights: Customisable options for specific lending needs.

Superior User Experience: A streamlined and intuitive interface for both lenders and their customers.

Automated Data Aggregation and Insights: Streamlines operational processes.

Compliance with Regulations: Particularly beneficial in the Australian banking sector.

Improved Mortgage Pre-Approval Processes: Ongoing consent and open banking facilitate quicker pre-approval renewals.

The robust features underscore Basiq’s commitment to driving efficiency, accuracy, and user satisfaction. More than just a tool, Basiq Insights is a strategic ally for lenders, empowering them with the data and insights needed to navigate the complexities of the financial landscape. With a forward-thinking approach to data privacy, regulatory compliance, and user experience, Basiq Insights is setting a new standard for consumer affordability solutions. As the lending industry continues to evolve in this digital age, Basiq Insights is undoubtedly leading the charge, paving the way for smarter, faster, and more customer-centric lending practices.

Embrace the future of lending with Basiq Insights, where innovation meets efficiency and customer satisfaction.

Well, a whirlwind few days in Melbourne for Intersekt23. This year I thought I’d put some of my thoughts down on paper to share. Tried to keep it short but there was so much content ?

Scraping v CDR

The CDR sparked significant discussions over the course of two days. There was no mistaking the significance when I saw The Hon. Stephen Jones take the stage – it was evident he was about to announce something. True enough, the unveiling of a discussion paper advocating for the banning of screen scraping lived up to the anticipation. Given his previous discussions on the matter, the release was not unexpected, making it only a question of timing.

This indicates promising progress ahead. The Government views the CDR as a tool with the potential to significantly decrease scams and financial crimes, which currently costs the Australian economy nearly $3 billion a year. His words were very clear… “Screen scraping runs counter to the goals of CDR.” While complexities will arise for organisations currently using scraping, embracing the CDR is the optimal path for consumers seeking a secure and trustworthy method to share their data.

However, expediting adoption entails more than just prohibiting scraping. Given its nature as a “consumer” data right, it’s logical to assume we should have a means to measure the number of consumers who are actively sharing their data via the CDR. Presently, our metrics encompass data holders and their up time, but the absence of information regarding the volume of consumers engaging with the CDR is perplexing. As Peter Drucker says, “if you can’t measure it, you can’t manage it,” so what gives?

Then there are the challenges organisations encounter trying to get accredited, whether they’re going through direct channels or via access models. On one hand, there’s an understanding of the necessity to safeguard consumers, but on the flip side, certain requirements placed on organisations such as “adequate” insurance requirements can often lead to them being excluded from the CDR ecosystem. Finding the right balance is crucial to ensure the ecosystem’s growth and, ultimately, to increase the number of consumers who feel comfortable sharing their data.

“We need more CDR use cases!” Really?

A prevalent theme I heard across numerous sessions, emphasised the need for “more use cases” beyond just Lending, Personal Financial Management (PFMs), and Product comparison. ? Perhaps this sentiment arises from a lack of awareness, but upon closer examination of organisations already using CDR Open Banking, you come to realise that we in fact have a number of use cases!

Climate change: calculate carbon emissions from bank transactions – Greener

Property management: tools for property managers – PropertyMe

Collections: create payment plans to optimise repayments – Panthera Finance

Charity: round ups on everyday transactions to make a donation – PokitPal

Recycling: account verification to deposit funds – TOMRA

Accounting: software for accountants to manage their client’s books – Olivs

Beyond that, the use of CDR data for Lending can be extended beyond the credit application process. This includes using the CDR to understand a customer’s financial position to provide more contextually relevant products, and monitoring for changes in financial position that could indicate financial hardship.

And as Jake Osborne from Lendela said in his “Fireside Chat: CDR and Life Events,” … “while we often think about building new products, CDR can also be used for improving processes.”

Many of the organisations currently using Open Banking do so via the CDR representative model through intermediaries who are Accredited Data Recipients. If you’re looking for use cases, have a look at who these organisations are.

Consent is a central figure

Scott Farrell from King & Wood Mallesons in his talk on “Fintech Next: People, Value, Trust” elaborated on what he saw as the “why” of CDR. He broke it down into 4 main constructs that included Competition, Innovation, Financial Inclusion and Consumer Protection. In my mind this was a simple and clear way to articulate it. He continued by emphasising that “information” and “money” should be considered the same thing. I guess the saying “time is money” can also be extend to “information is money”. So being able to control your own information and knowing who and how it’s being used should be important to all consumers. Just look at all the social media platforms we use like Facebook, Instagram, and Twitter (errr “X”) – do we know how our data is being used? And how much money is being made off our information?

As you delve deeper, the significance of consent in relation to information becomes increasingly apparent. This point was highlighted during the panel discussion on “The Convergence of Data, Identity, and Payments,” featuring Damir Ćuća (Basiq), Nathan Churchward (Cuscal), Clare Rhodes (Identitii) & Josh Read (IDVerse).

The three fundamental components – Data, Identity and Payments – are integral to any financial services application we engage with. But these are often looked at in silos which is even more pronounced given there are 3 separate regulations/industry initiatives impacting these areas – CDR for Data, NPP for Payments, and TDIF for Identity. Consumer consent serves as a key foundation. Establishing consent as the interconnected layer that links these three areas holds utmost importance.

But what does it mean for the consumer? Different consent processes for different processes in the same app? That’s not an interconnected experience. For example when PayTo proliferates, there will be consumer friction. What’s the experience on an app when (1) I need to verify myself (one consent), (2) I want to share my data via CDR (second consent) and then (3) I want to set up a payment with PayTo (third consent)? Let’s think about the consumer in all of this. Can I just give you consent once?

If as Scott Farrell said, information is money, give me a good digital experience when it comes to managing my information! And when Scott was asked what he would do if he could wave a magic wand on the CDR and do whatever he wanted, his answer was … “Weave digital Identity into the CDR and Payments. That’s the missing pillar.” And we come full circle. Data, Payments and Identity.

Right product, right channel, right time

As a marketing practitioner the concept of a consumer getting the right product, through the right channel and at the right time is the holy grail. I talk about this often in my teaching at Sydney University and I’ve often referred to it as the “golden triangle”. Get it right and you’ve hit the mark. Easier said than done. You could have the best product, but if it’s not available in the right channel and at the right time, it’s meaningless.

The session from Visa’s Matthew Wood on “Emerging Payment Trends in Asia Pacific” highlighted how the lines of finance are blurring. Product alone is no longer enough, it’s about distribution. Embedding finance in customer journeys is critical for success. When it comes to e-commerce, social media has played a big role in driving take up – think influencers, think embedded stores within social media platforms. The next phase? “Commerce will have its ChatGPT moment”!

The panel on “How Open Data is Shaping the Future of Personal Finance” talked about a similar theme with respect to context. Jason Leong (PocketSmith), Simone Jemmett (Experian), Dan Jovevski (WeMoney) & Adam Gulden (Moneythor) talked about the importance of contextual relevance when it comes to personal finance. If you’re going to make a decision about your personal finances, it has to be contextually relevant – right time, right place, right moment. That’s the “value exchange”. If you get this right it will lead to better engagement and uptake. That to me is the “golden triangle”.

A few other things I found interesting

AI & Data Hacks AI. Still mind boggling what is possible. In the session on “Data Hacks to Banking Collapses: What Have We Learnt in the Last 12 Months,”Alisdair Faulkner from Darwinium said that “any digital signal a human creates can be accessed and replicated by AI. Voice. Keystrokes. Visual. This is scary!? Dan Draper from CipherStash ended the panel with “Shit happens. Don’t think it won’t happen to you?”

Ethics Judo Bank’s Joseph Healy in the session on “Ethics in Fintech”talked about the need to be a values driven organisation. Numerous fintechs set out their their journey with a purpose and set of values in mind, but as they grow, the challenge becomes hiring the right people and consistently viewing decisions through the lens of these values. This becomes even more critical when business choices could potentially impact those very values. From my perspective having the right leaders who share the same values play a critical role in maintaining accountability and staying steadfast amidst external influences.

DIY or Partner? In the session with James Read from Send Payments on “How can Fintechs unlock success? Innovate of Integrate”he talked about the challenge of whether you should build or partner? This can be tied what your exit strategy is. If you’re aiming for a trade sale then maybe innovating and owning your own stack is more important. But if you’re aiming for an IPO then maybe partnering and acquiring customers rapidly is the focus. In that same session Imelda Newton from Tic:Toc looked at it from a different lens. You also have to consider internal development teams wanting to build things themselves but P&L owners wanting to derisk delivery and potentially wanting to involve 3rd parties to some degree. Getting that balance right can be challenging.

Digital Identity Lastly, a notable facet of digital identity that caught my attention was the discussion panel titled “Digital Identity: Defining Excellence and the Path Forward.” During this panel, Jason-Urranndulla Davis from Hold Access delved into scenarios where individuals face a significant challenge due to a “lack of identity” resulting from insufficient documentation. This particularly impacts First Nations people and those with limited documentation, posing substantial barriers to accessing essential services. Thus, the question arises: How can we ensure that promoting inclusivity remains a central focus when implementing any changes to the 100-point identity verification system which is currently outdated and not fit for purpose?

The After party

And #Intersekt23 wouldn’t be complete without Basiq’s After Party. Thanks to everyone who attended. It’s always great to have the opportunity to bring people together. Here’s the photo gallery from the night.

Sharing of banking data has been a service provided in Australia in an unregulated capacity for many years. Open Banking has formalised this capability via the Consumer Data Right (CDR) that is mandated and regulated by the Australian Government.

Let’s touch on some factors that contribute to the safety and security of CDR Open Banking for consumers.

Consumers have full control over their banking data

Consumersmust provide explicit consent before their data is shared with third-party providers. They have the ability to choose what data is shared, for what purpose and for how long. They can also revoke consent at any time, giving them greater control over their information.

Strong authentication that does not include password sharing

Open Banking requires strong customer authentication to prevent unauthorised access. Unlike screen scraping it doesn’t involve customers sharing their online banking password, and instead uses some form of Multi Factor Authentication such as a mobile SMS or in app verification code.

Sharing data via secure banking APIs

Open Banking relies on secure Application Programming Interfaces (APIs) for data sharing between Data Holders (such as banks) and Data Recipients (such as third party apps). These APIs follow strict security specifications such as Financial-grade API (FAPI) and standards such as OAuth 2.0 and OpenID Connect to ensure data is transmitted securely.

Consumers are protected by strict privacy regulations

Open Banking operates under strict privacy regulations, including the Privacy Act 1988 and the Australian Privacy Principles. Data Holders and Data Recipients are required to handle consumer data responsibly, ensuring its confidentiality, integrity, and protection. They must have robust data protection measures in place to safeguard against breaches or unauthorised use.

Compliance is regulated by the ACCC

Open Banking in Australia is regulated by the Australian Competition and Consumer Commission (ACCC) and Office of the Australian Information Commissioner (OAIC). These regulatory bodies ensure that Data Holders and Data Recipients adhere to security standards and compliance requirements. Ongoing monitoring and auditing help identify any vulnerabilities or risks and ensure the safety of consumer data.

Ongoing Government commitment to security

Finally, the government is maintaining it’s investment in a safer digital future, this year’s Federal Budget included a further investment in the Consumer Data Right of $88.8 million over two years, with a focus on several areas including:

cyber security improvements across all CDR agencies to reflect the evolving data landscape. This includes constant assessment and updates to the security standards adopted.

expanding awareness of the CDR brand as a trusted, safer data-sharing model that allows consumers to easily identify CDR-enabled providers, products and services. Consumers will become more security aware when sharing their data and will be choosing CDR data share options over less secure alternatives.

For many, June 30 is an annual milestone loaded with stress and confusion. Not only are the rules and regulations around tax law continually changing, but many individuals don’t know their financial position until it’s time to lodge their tax return.

For companies, accounting software has made it easy to keep tabs on their tax position. But for individuals, self-managing their taxes has been clunky, time-consuming and clouded in uncertainty.

That’s exactly what TaxTank is on a mission to solve. TaxTank is a low-cost, cloud-based software helping to simplify tax for everyday Australians.

Loaded with smart tax tools and automated bank feeds powered by Open Banking, TaxTank makes it easy to maximise deductions, minimise tax and reduce end-of-financial-year stress for property investors, sole traders and individual taxpayers.

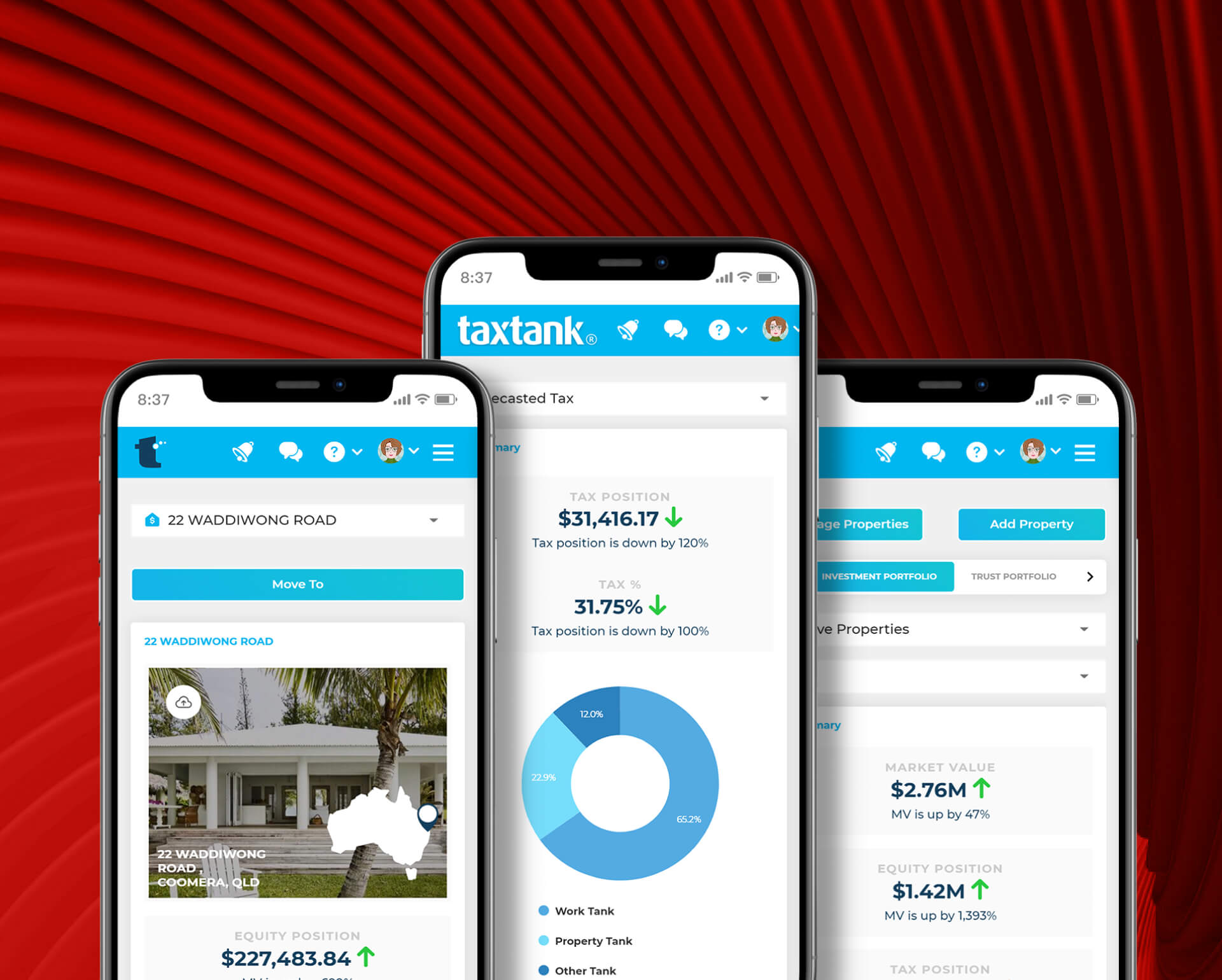

What is TaxTank?

At its core, TaxTank aims to help individuals make informed financial decisions ahead of tax time. The software is cloud-based and low-cost (starting at just $6 per month), packed with features designed to make self-managing income, assets, expenses and overall financial position stress-free.

For founder and Gold Coast-based tax specialist Nicole Kelly, the platform champions a fairer, more transparent tax system for individuals.

Amidst the ever-increasing cost of ATO scrutiny, TaxTank was born from the belief that tax simply cannot be a once-a-year event and be effective. There had to be a better way to improve compliance whilst still making tax simple to manage, easy to understand and hassle-free for everyday Australian taxpayers.

To achieve this, TaxTank empowers customers with the tools they need to plan, manage and simplify their tax affairs in real-time.

Nicole Kelly, Founder of TaxTank says, “working as a CPA and taxation specialist for nearly 10 years, I would see client after client struggling to keep on top of their tax affairs. At tax time it’s a mad rush to consolidate expenses while spending hours searching for receipts to substantiate any deductions for the past year.”

“We wanted to develop a platform that gives the individual taxpayer the ability to not only manage their taxes more effectively but provides a transparent view of their real-time tax and financial position, 365 days a year. This gives the individual and those working with an accountant the opportunity to identify and take advantage of additional tax saving opportunities before the financial year ends,” Nicole added.

TaxTank uses a range of ‘tanks’ or digital containers that store different parts of an individual’s information:

Work Tank manages work-related income using live bank feeds, along with storing receipts for work-related expenses.

Property Tank keeps tabs on an investor’s properties and portfolios to monitor the cash, tax and equity positions.

Sole Tank is designed to help sole traders manage their income, with invoicing and reporting tools, too.

Holdings Tank is designed to manage investors’ stocks, shares and cryptocurrencies, keeping tabs on their portfolio’s value and any gains or losses they’ve made.

Spare Tank is a secure storage area for paperwork, receipts and deduction information.

What sets TaxTank apart is its focus on real-time data, keeping individuals informed about their financial position all year round. Rather than spending hours at tax time collating documents and nervously submitting their return, the platform provides up-to-date tax summaries to save them both time and money and enable better decision-making.

Committed to building a platform that solves the real-world tax problems of everyday Australians, TaxTank surveyed over 33,200 people to find out what features mattered most to them.

Here’s what they’ve delivered:

Real-time reporting with detailed, interactive tax position reports and forecasts.

Live bank feeds that offer real-time tax position summaries.

Secure document storage for receipts, statements and warranties (making a shoebox of faded receipts a thing of the past).

Simple, smart and automated depreciation tools to maximise tax benefits without the hassle.

Smart property value forecasting using CoreLogic’s industry-leading insights (perfect for property investors).

Automate tax position estimates and recommendations for ways to maximise deductions.

The result? TaxTank makes it easy for individuals to claim everything they’re entitled to, while ensuring they’ve got the right records to back up their claims with the ATO. The platform even produces a comprehensive range of tax reports, including the myTax report, allowing users or their accountants to lodge their tax returns with speed and confidence.

Solving tax time stress with smart tax tools

For individuals, lodging their tax returns often comes with fear and uncertainty. Will they receive the sizable refund they were hoping for, or will they be hit with a large, unexpected tax bill?

Plus, the process can take hours out of their week as individuals scramble to gather invoices, receipts and documents from the past 12 months. For many, forking out hundreds (if not thousands) of dollars on an accountant is the only way to get this process sorted.

But with TaxTank’s smart tax tools, individuals can self-manage their tax affairs with confidence. The platform offers travel logbooks, capital gains tax calculators, home office logbooks, depreciation calculators and more to help Australians make informed decisions all year round (not just when lodging their tax return).

Harnessing live bank feeds, powered by Open Banking

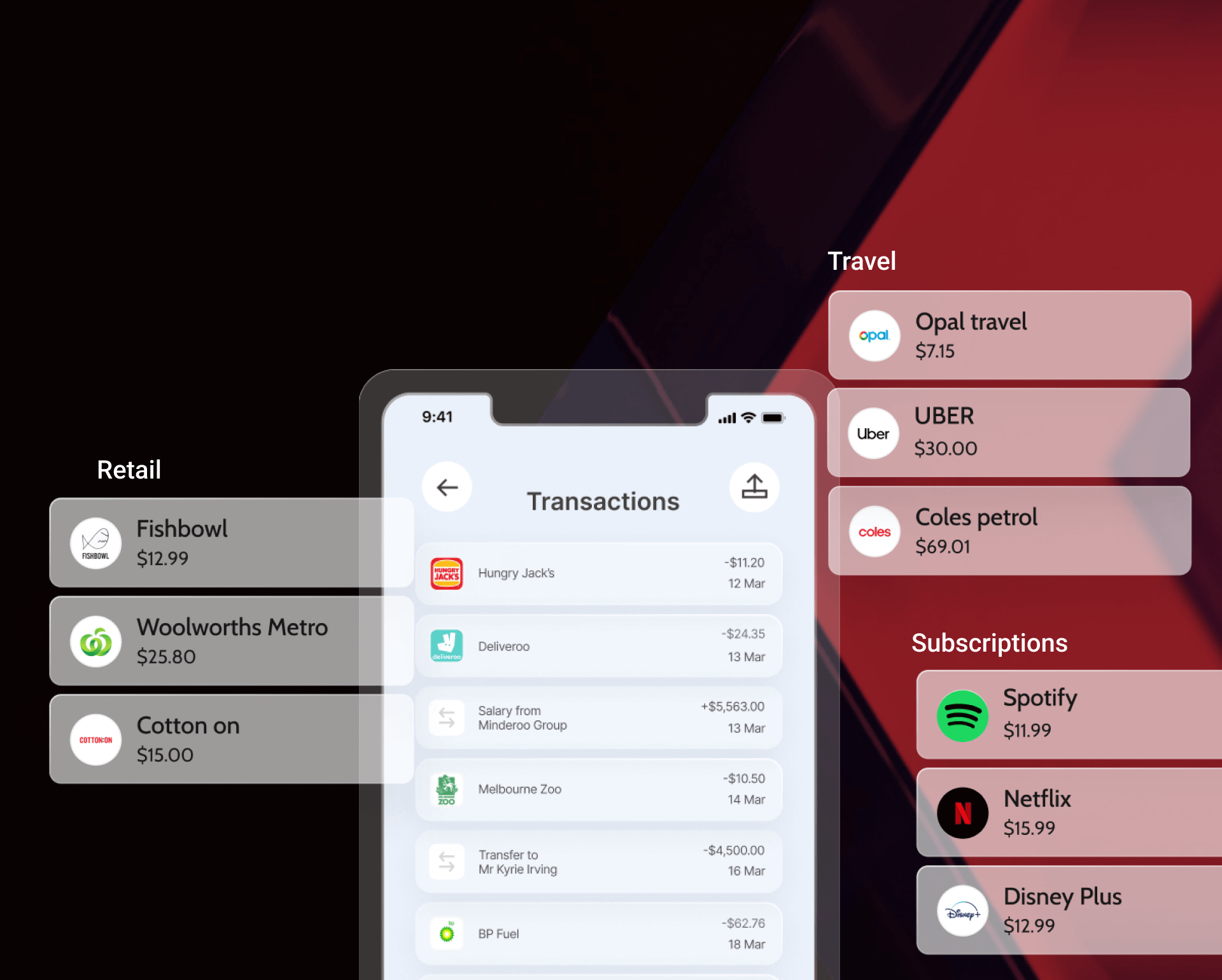

TaxTank is pioneering a new way of approaching tax management, the first platform in Australia to tap into bank feeds (powered by Open Banking) gives taxpayers real-time access to their financial position.

While live bank feeds are commonly used for business accounting software, individuals have been forced to tackle the process of gathering receipts and lodging their returns manually.

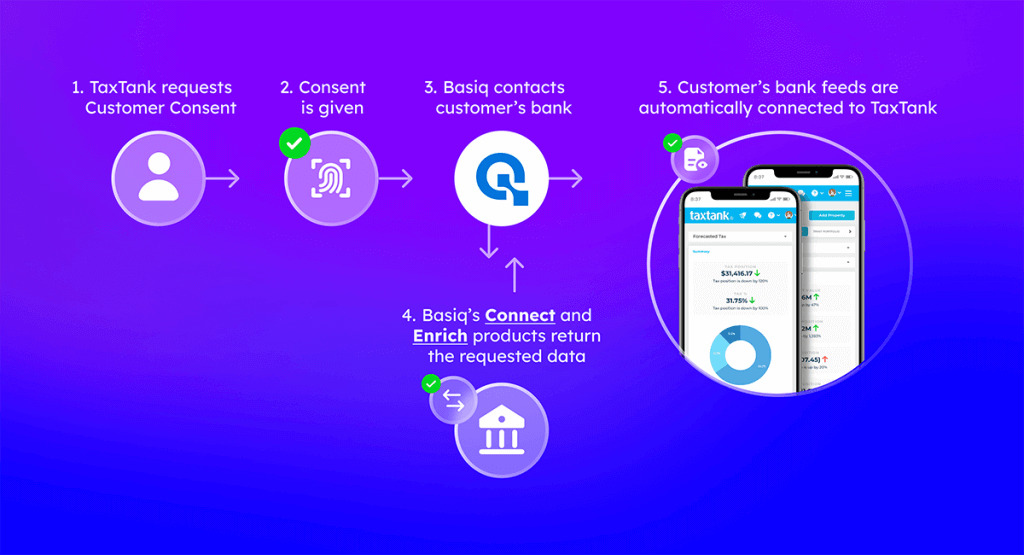

How TaxTank and Basiq work together

By harnessing Open Banking and Basiq’s Connect and Enrich products, TaxTank harnesses live bank feeds to run its entire platform. This live, standardised and categorised data gives individuals the ability to ensure they’re claiming everything they’re eligible for as a tax deduction (lowering the chance of human error or missing valuable deductions).

Allocating loans and overdrafts to properties also enables a real-time overview of equity, interest rates and accurate growth forecasts over time for informed decisions without the guesswork.

Here’s how it works:

TaxTank requests customer consent to access live bank feeds via Basiq’s Consent UI

Customer accepts or declines permission

If consent is given, Basiq contacts the customer’s bank

Customer bank returns the requested bank data using Basiq’s Connect and Enrich products.

They are ready to roll! Every time a customer logs on their live bank feeds are automatically connected, ready for use on the TaxTank platform – until consent is withdrawn or expires.

It’s never been more important for individuals to have a watertight record-keeping system for tax-related receipts and documents. In fact, changes to tax legislation now mean the ATO is laser-focused on preventing fraudulent activity among investment property owners.

These recent changes mean the ATO is now able to access bank transactions related to these properties to compare them with an individual’s tax declaration).

For individuals, gaining access to live bank feeds through TaxTank is a game-changer, giving them clear oversight of their records and financial position well ahead of tax time.

The future of smarter tax-time decision-making

TaxTank is passionate about leveraging Open Banking to revolutionise the way individuals manage their finances.

To date, individuals have had few options when it comes to proactively preparing for tax time. Large accounting firms have come with high price tags and have been moving away from working with individuals, instead focusing on more lucrative ongoing partnerships with businesses.

Powered by live bank feeds, TaxTank’s software makes accounting and tax support accessible to everyone, from sole traders to individual taxpayers and even property investors.

Individuals can allocate just 10 minutes a week to reviewing transactions and uploading receipts (rather than spending hours scrambling to gather their records at tax time). Plus, there are serious cost savings for taxpayers, in particular investors, who can score upwards of a 60% cost saving by using TaxTank to self-manage throughout the year and engaging TaxTank’s specialist team of virtual accountants to review and lodge painlessly at tax time.

With the ability to review their financials at any time, forecast potential tax scenarios and pinpoint deduction opportunities, individuals are better placed to take control of their finances (which is becoming increasingly important in today’s turbulent economic climate).

Building financial wellness has big benefits for both customers and financial service providers in deepening relationships and sustainability. But learning how to wrangle our finances can seem complex, tedious and even overwhelming.

For banks, lenders and financial institutions, finding innovative ways to engage customers helps them stand out in a competitive landscape. For customers, being disengaged with their finances means they are missing out on big opportunities to grow their wealth, and for small banks & financial institutions, this poses a risk to relevancy & retention.

That’s where generating behavioural data within a game-based framework comes in. Moroku is leading the way in pioneering the next generation of online banking experiences. Founder Colin Weir believes that gamification and behavioural economics can revolutionise financial education and help people build better financial habits.

By recognising the need for play, our inherent love of challenges and incentives and rewards, Moroku is helping banks, wealth providers and fintechs to win by helping customers win.

What is Moroku?

The aim of Moroku is two-fold: gamifying the banking experience helps financial institutions deeply engage with their customers, while also empowering customers to foster better money habits to grow their wealth.

Moroku builds disruptive, digital banking experiences designed to inject fun into banking. The team’s cutting-edge behavioural banking engine uses AI and the power of game design to help financial service providers acquire, engage and retain customers.

With more competition in the financial services space than ever before, finding ways to stand out has never been more important. But according to Cap Gemini’s 2022 retail banking report, nearly half of the respondents feel their current banking relationships aren’t rewarding them (49%).

By tapping into the power of AI, Moroku is passionate about helping institutions deeply understand the needs of customers and deliver hyper-personalised, engaging user experiences.

Colin believes, “the future of banking is focused on the customer and helping them thrive with their money.”

Moroku, through their Odyssey platform, helps customers build financial fitness with personalised, game-inspired journeys that offer helpful nudges, tailored support and the ability to unlock content, money systems, rewards and awards that recognise and reward effort and loyalty.

The Moroku founder story

Moroku’s founder Colin has always had a passion for the power of data and AI.

Before founding Moroku, Colin used his background in forestry and data science to build models for predicting ecosystem growth. This experience sparked the idea of using data to understand customer growth in banking.

With a deep interest in what the next generation of banking looks like, Colin left Microsoft to set Moroku up as a “laboratory for figuring out where customers are on the journey, and how they’re growing. Thinking about how we understand that growth and how to build a data model around this growth.”

Who is Moroku for?

At the core of Moroku’s mission is the question: “How do we help banks win by helping their customers win?”

The platform has been developed with two core audiences in mind: the financial institutions that integrate Moroku into their operations, and the customers of these institutions who are interested in learning more about making their money work harder for them.

It’s the perfect solution for banks and fintechs who want to stay ahead of the competition by putting financial education and customer success at the centre of their decision-making.

“For us, we’re here to help banks and fintechs support, reward, and encourage customers as they start to build good money habits.”

Whether it’s first home buyers, budding investors, or helping Gen Z’s learn the basics of managing their money, Moroku’s AI gaming models reward customers for learning more about money and building good financial habits.

How does Moroku work?

Moroku’s flexible platform integrates with each service provider’s core banking system and user apps, helping to gamify the everyday experiences of mobile banking (from paying bills to hitting savings goals).

Its main purpose is to provide a unique and engaging customer experience by offering three key components:

Player Maps – this feature provides knowledge of where a customer is on their player journey, from novice to master.

Money Systems and Subsystems – these are money tools and capabilities that are unlocked by players as they master their money.

Rewards and Awards – these are the ‘nudges’ that support the customers, incentivise engagement and let them know how they’re progressing on their journey.

Player Maps are inherent to games. As players level up they are presented with increasing levels of difficulty, missions and challenges (all link back to elements of money, from saving to investing). This keeps the game interesting and potentially endless while sparking meaningful behaviour change.

Banks have enormous numbers of tools and systems available for customers to take the guesswork out of money mastery. Yet knowing when and how to use all of these money systems is not obvious.

A good example of this is PayID in Australia. Being able to send money to someone’s mobile phone number or email address is a fabulous innovation. Yet less than half the country has set theirs up. Unlocking PayID as a spending weapon once you have passed level one makes this task fun, flipping it from a chore to an award to be won.

By sitting in the background of an institution’s existing architecture, Moroku’s engagement engine allows for a more authentic way to connect with the customer. It helps them build skills, overcome challenges and provides an enormous number of moments to engage customers and deepen the relationship.

It’s a win-win situation for both financial institutions and their customers.

Using games and data to build financial wellness

Why is it so hard to create (and sustain) good money habits? Colin points to two things: present bias and the need for immediate gratification, two key principles in behavioural economics.

“Part of behavioural economics is the idea of present bias. It’s this idea that we overly discount future gain. We’d rather have $1 now than have $2 tomorrow. We immediately feel a sense of loss,” Colin explains.

The science here is fascinating. Instead of focusing on long-term goals (which can feel abstract and even unattainable), Moroku helps customers celebrate small wins that get them closer to their end money goal. Colin goes on to explain how saving often feels like a loss, and why speaking to logic isn’t always the answer.

“We connect with people on an emotional level. As soon as the brain activity starts to move here, we move out of fight, flight or freeze and into solution mode. Money is very hard to use, and it’s full of emotion. So that’s where you have to go to get the results.”

By designing customer journeys around game principles, Moroku has found a way to make finance engaging, fun, and accessible for everyone.

Learning new skills (like building financial fitness or learning how to invest) can be a daunting task. But Moroku is breaking down these barriers with their gaming experiences, such as their virtual trading platform.

“Customers are provided with a safe place to try some things out, to understand the core principles in a virtual world where they could build these sorts of skills up. This is a space where they could fail, they could learn, and ultimately where they could overcome these challenges.”

Moroku uses individual missions, such as opening up a trading account or paying down a mortgage, which is tailored to a customer’s unique money goals.

With awards and incentives along the way, customers are rewarded for engaging with the platform and taking practical steps towards building financial literacy.

Improving Moroku’s customer journey using Open Banking

When it comes to Open Banking, Colin says that Basiq has helped Moroku get a deep dive into customer data.

“Once we transitioned to Open Banking, we got more data into the engine. That means we can take customers on a more accurate journey. Artificial Intelligence is incredibly data hungry. Whilst some generative models can quite literally generate their own data, gathering more behavioural data from customers’ broader financial relationships allows us to hyper-personalise journeys a lot faster.”

Using Open Banking, Moroku gains a comprehensive understanding of a customer’s financial history, habits, and situation, allowing them to build a personalised journey to help customers achieve their financial goals.

With 72% of customers expecting to receive a personalised banking experience, integrating this data into unique customer journeys has never been easier.

Colin says working with Basiq to integrate Open Banking data into the Odyssey platform has been a natural fit.

“The more data that we get, the easier those algorithms are to multiply to the point where we can have a hyper-personalised individual algorithm for every customer because we have access to the unique data to do that through Basiq’s Open Banking platform.”

What’s next for Moroku

Colin’s main focus is on rebuilding the banking experience in Australia with a mission-driven approach. He’s looking forward to making some big moves globally in the future, but at the forefront of his attention right now is getting Odyssey integrated into banks across Australia.

With the right support in place, Moroku is well-positioned to scale its offering, partner with more financial service providers across Australia and enable more Australians to build financial fitness and grow their wealth.

Dealing with different platforms doesn’t have to be stressful

Basiq has launched a partnerships program providing greater capability and more value to customers. We are collaborating with a curated list of Open Banking enabled integration partners, as well as development and community partners, to meet the needs offintechs, financial institutions and lending providers alike.

Organisations relying on customer financial data for product or service delivery often require support from multiple providers to access data across many sources and ensure it is fit for purpose.

Finding and integrating with the necessary solutions can be a time consuming and technically complex process, particularly when it comes to Open Banking. Basiq’s partnership program has been designed to reduce the burden to business, saving them time, money and stress.

A list of trusted providers at your fingertips

Basiq’s Head of Accounts and Partnerships, Rebecca Tissington, says she is pleased to announce Simpology, Moroku, Zeal, Nimo, Authsignal and Codat as its flagship Integration Partners, that are leaders across lending, collections, fraud operations and financial management – for both business and personal.

“We understand that businesses rely on multiple cloud-based platforms and data points to automate decisions, manage processes and increase customer conversion. We want to ensure the experience is frictionless so they can focus on what they do best– growing their business,” said Rebecca.

“Basiq has always been about supporting the end-to-end experience of customers. Offering access to a range of trusted partners specialising in everything from loan origination to customer authentication is another step towards this goal.”

This is significant for the maturation of Open Banking. By offering access to specialised, CDR-enabled service providers, Basiq is expanding the possibilities when it comes to new use cases that will help promote and accelerate the uptake of Open Banking.