Building financial wellness has big benefits for both customers and financial service providers in deepening relationships and sustainability. But learning how to wrangle our finances can seem complex, tedious and even overwhelming.

For banks, lenders and financial institutions, finding innovative ways to engage customers helps them stand out in a competitive landscape. For customers, being disengaged with their finances means they are missing out on big opportunities to grow their wealth, and for small banks & financial institutions, this poses a risk to relevancy & retention.

That’s where generating behavioural data within a game-based framework comes in. Moroku is leading the way in pioneering the next generation of online banking experiences. Founder Colin Weir believes that gamification and behavioural economics can revolutionise financial education and help people build better financial habits.

By recognising the need for play, our inherent love of challenges and incentives and rewards, Moroku is helping banks, wealth providers and fintechs to win by helping customers win.

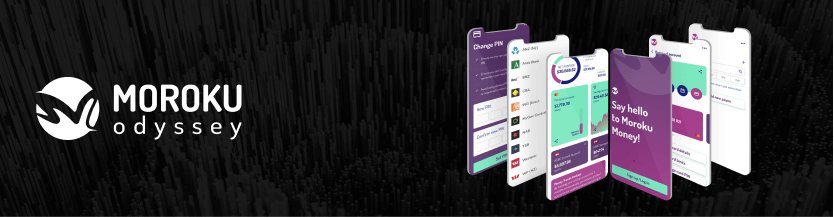

What is Moroku?

The aim of Moroku is two-fold: gamifying the banking experience helps financial institutions deeply engage with their customers, while also empowering customers to foster better money habits to grow their wealth.

Moroku builds disruptive, digital banking experiences designed to inject fun into banking. The team’s cutting-edge behavioural banking engine uses AI and the power of game design to help financial service providers acquire, engage and retain customers.

With more competition in the financial services space than ever before, finding ways to stand out has never been more important. But according to Cap Gemini’s 2022 retail banking report, nearly half of the respondents feel their current banking relationships aren’t rewarding them (49%).

By tapping into the power of AI, Moroku is passionate about helping institutions deeply understand the needs of customers and deliver hyper-personalised, engaging user experiences.

Colin believes, “the future of banking is focused on the customer and helping them thrive with their money.”

Moroku, through their Odyssey platform, helps customers build financial fitness with personalised, game-inspired journeys that offer helpful nudges, tailored support and the ability to unlock content, money systems, rewards and awards that recognise and reward effort and loyalty.

The Moroku founder story

Moroku’s founder Colin has always had a passion for the power of data and AI.

Before founding Moroku, Colin used his background in forestry and data science to build models for predicting ecosystem growth. This experience sparked the idea of using data to understand customer growth in banking.

With a deep interest in what the next generation of banking looks like, Colin left Microsoft to set Moroku up as a “laboratory for figuring out where customers are on the journey, and how they’re growing. Thinking about how we understand that growth and how to build a data model around this growth.”

Who is Moroku for?

At the core of Moroku’s mission is the question: “How do we help banks win by helping their customers win?”

The platform has been developed with two core audiences in mind: the financial institutions that integrate Moroku into their operations, and the customers of these institutions who are interested in learning more about making their money work harder for them.

It’s the perfect solution for banks and fintechs who want to stay ahead of the competition by putting financial education and customer success at the centre of their decision-making.

“For us, we’re here to help banks and fintechs support, reward, and encourage customers as they start to build good money habits.”

Whether it’s first home buyers, budding investors, or helping Gen Z’s learn the basics of managing their money, Moroku’s AI gaming models reward customers for learning more about money and building good financial habits.

How does Moroku work?

Moroku’s flexible platform integrates with each service provider’s core banking system and user apps, helping to gamify the everyday experiences of mobile banking (from paying bills to hitting savings goals).

Its main purpose is to provide a unique and engaging customer experience by offering three key components:

Player Maps – this feature provides knowledge of where a customer is on their player journey, from novice to master.

Money Systems and Subsystems – these are money tools and capabilities that are unlocked by players as they master their money.

Rewards and Awards – these are the ‘nudges’ that support the customers, incentivise engagement and let them know how they’re progressing on their journey.

Player Maps are inherent to games. As players level up they are presented with increasing levels of difficulty, missions and challenges (all link back to elements of money, from saving to investing). This keeps the game interesting and potentially endless while sparking meaningful behaviour change.

Banks have enormous numbers of tools and systems available for customers to take the guesswork out of money mastery. Yet knowing when and how to use all of these money systems is not obvious.

A good example of this is PayID in Australia. Being able to send money to someone’s mobile phone number or email address is a fabulous innovation. Yet less than half the country has set theirs up. Unlocking PayID as a spending weapon once you have passed level one makes this task fun, flipping it from a chore to an award to be won.

By sitting in the background of an institution’s existing architecture, Moroku’s engagement engine allows for a more authentic way to connect with the customer. It helps them build skills, overcome challenges and provides an enormous number of moments to engage customers and deepen the relationship.

It’s a win-win situation for both financial institutions and their customers.

Using games and data to build financial wellness

Why is it so hard to create (and sustain) good money habits? Colin points to two things: present bias and the need for immediate gratification, two key principles in behavioural economics.

“Part of behavioural economics is the idea of present bias. It’s this idea that we overly discount future gain. We’d rather have $1 now than have $2 tomorrow. We immediately feel a sense of loss,” Colin explains.

The science here is fascinating. Instead of focusing on long-term goals (which can feel abstract and even unattainable), Moroku helps customers celebrate small wins that get them closer to their end money goal. Colin goes on to explain how saving often feels like a loss, and why speaking to logic isn’t always the answer.

“We connect with people on an emotional level. As soon as the brain activity starts to move here, we move out of fight, flight or freeze and into solution mode. Money is very hard to use, and it’s full of emotion. So that’s where you have to go to get the results.”

By designing customer journeys around game principles, Moroku has found a way to make finance engaging, fun, and accessible for everyone.

Learning new skills (like building financial fitness or learning how to invest) can be a daunting task. But Moroku is breaking down these barriers with their gaming experiences, such as their virtual trading platform.

“Customers are provided with a safe place to try some things out, to understand the core principles in a virtual world where they could build these sorts of skills up. This is a space where they could fail, they could learn, and ultimately where they could overcome these challenges.”

Moroku uses individual missions, such as opening up a trading account or paying down a mortgage, which is tailored to a customer’s unique money goals.

With awards and incentives along the way, customers are rewarded for engaging with the platform and taking practical steps towards building financial literacy.

Improving Moroku’s customer journey using Open Banking

When it comes to Open Banking, Colin says that Basiq has helped Moroku get a deep dive into customer data.

“Once we transitioned to Open Banking, we got more data into the engine. That means we can take customers on a more accurate journey. Artificial Intelligence is incredibly data hungry. Whilst some generative models can quite literally generate their own data, gathering more behavioural data from customers’ broader financial relationships allows us to hyper-personalise journeys a lot faster.”

Using Open Banking, Moroku gains a comprehensive understanding of a customer’s financial history, habits, and situation, allowing them to build a personalised journey to help customers achieve their financial goals.

With 72% of customers expecting to receive a personalised banking experience, integrating this data into unique customer journeys has never been easier.

Colin says working with Basiq to integrate Open Banking data into the Odyssey platform has been a natural fit.

“The more data that we get, the easier those algorithms are to multiply to the point where we can have a hyper-personalised individual algorithm for every customer because we have access to the unique data to do that through Basiq’s Open Banking platform.”

What’s next for Moroku

Colin’s main focus is on rebuilding the banking experience in Australia with a mission-driven approach. He’s looking forward to making some big moves globally in the future, but at the forefront of his attention right now is getting Odyssey integrated into banks across Australia.

With the right support in place, Moroku is well-positioned to scale its offering, partner with more financial service providers across Australia and enable more Australians to build financial fitness and grow their wealth.

Dealing with different platforms doesn’t have to be stressful

Basiq has launched a partnerships program providing greater capability and more value to customers. We are collaborating with a curated list of Open Banking enabled integration partners, as well as development and community partners, to meet the needs offintechs, financial institutions and lending providers alike.

Organisations relying on customer financial data for product or service delivery often require support from multiple providers to access data across many sources and ensure it is fit for purpose.

Finding and integrating with the necessary solutions can be a time consuming and technically complex process, particularly when it comes to Open Banking. Basiq’s partnership program has been designed to reduce the burden to business, saving them time, money and stress.

A list of trusted providers at your fingertips

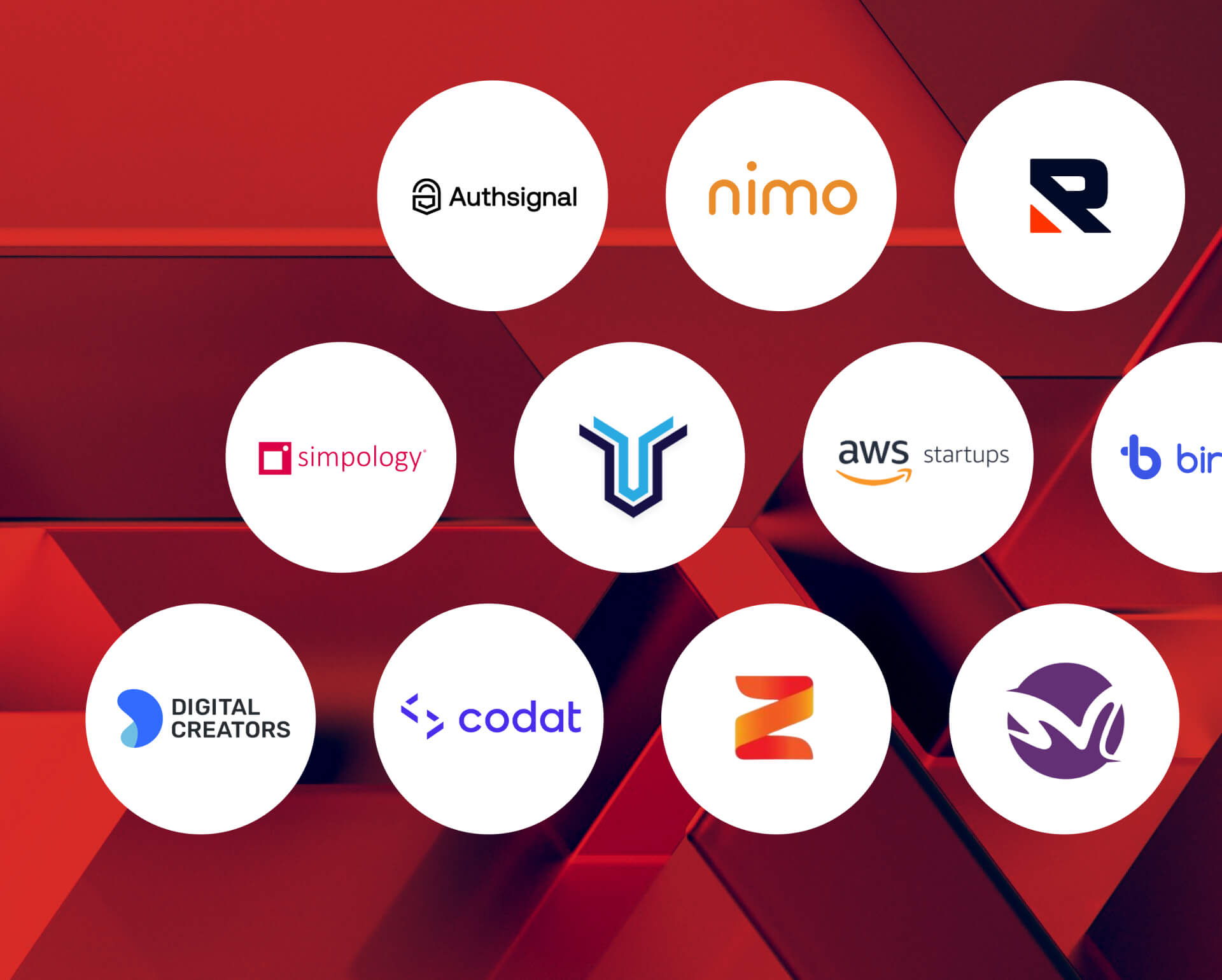

Basiq’s Head of Accounts and Partnerships, Rebecca Tissington, says she is pleased to announce Simpology, Moroku, Zeal, Nimo, Authsignal and Codat as its flagship Integration Partners, that are leaders across lending, collections, fraud operations and financial management – for both business and personal.

“We understand that businesses rely on multiple cloud-based platforms and data points to automate decisions, manage processes and increase customer conversion. We want to ensure the experience is frictionless so they can focus on what they do best– growing their business,” said Rebecca.

“Basiq has always been about supporting the end-to-end experience of customers. Offering access to a range of trusted partners specialising in everything from loan origination to customer authentication is another step towards this goal.”

This is significant for the maturation of Open Banking. By offering access to specialised, CDR-enabled service providers, Basiq is expanding the possibilities when it comes to new use cases that will help promote and accelerate the uptake of Open Banking.

Open Banking represents a seismic shift in the fabric of financial services. It allows consumers to have greater control over their financial data, which stimulates competition, allowing smaller institutions, startups and fintechs to leverage financial data in order to compete with incumbent institutions who have dominated the industry for so long.

What is Open Banking?

Open Banking is an innovative and legislated financial services practice which gives consumers the option of sharing their personal information and financial data with accredited third parties, through the use of application programming interfaces (APIs). This creates an unprecedented ‘open’ network of shareable data between financial institutions, who hold consumer data, and service providers, who use the data to create new offerings under the express consent of the consumer.

Why does Open Banking matter? Open Banking will change the way consumers and businesses interact with their finances, and increase the ease and efficiency of data sharing between financial institutions. Open Banking gives consumers more control over their financial data and makes it easier to share their data with companies they trust. This efficient transfer of data will also make it easier for companies to offer new products and services, powered by a technical and regulatory framework to allow consumers to securely share their information in a secure manner. Open Banking is the future of financial services.

What are the main benefits of Open Banking?

Open Banking gives accredited businesses access to valuable data that was previously siloed and held within larger financial institutions. In this sense, Open Banking ‘levels the playing field’ for businesses who wish to create new products and services without the overhead of manually integrating with a number of financial institutions. Consumers will now be able to access and share their banking data with trusted and registered third parties in order to improve their own financial situations, for example, by comparing accounts or accessing new products.

Open Banking is dictated by federal legislation known as the Consumer Data Right (CDR), providing a set of mandated APIs that will provide a stable and reliable connection to customer & financial data, reduce engineering effort, and ultimately improve the customer experience and efficiency of data sharing. These APIs also provide universal data standards across financial institutions, which allows for improved interoperability across financial institutions.

Value for Consumers Open Banking will simplify switching banks and sharing information regarding your account information, transaction history and other financial details. This information can be used to analyse, optimise and enhance your financial situation. This concept also applies to a number of use cases, such as: ease by which you will be able to sign up for new credit or debit card, manage your joint accounts, apply for investment loans, and utilise financial products and budgeting tools which track and plan expenditures – ultimately making your money and general financial wellness a more enjoyable and interactive experience. As the Open Banking ecosystem continues to mature, more and more use cases will arise across a number of different segments.

Benefits for Fintechs, Banks and other Organisations Open Banking is empowering for the financial services industry, creating a number of use cases for those who are using financial data in a novel way. First and foremost, the Open Banking legislation creates competition, challenges the status quo, and levels the playing field of banking, allowing smaller companies and financial institutions equal access to a market which major banks have oligopolised for so long.

With the data sharing pipes laid, it will be much easier to initiate consumer data sharing between data holders (those that have traditionally held financial data such as banks) and data recipient (accredited third parties). Through easier access to financial data, this will encourage competition in the financial services sector, bringing with it a level of innovation that benefits consumers and businesses. It will also enable smaller banks and fintechs to compete with their larger counterparts.

Introduction to the Consumer Data Right

What is the Consumer Data Right? The Consumer Data Right (CDR) is an initiative to drive competition and the development of new financial products and services. It gives consumers greater control over their data and the ability to securely share their data with third parties. CDR dictates a granular, consent-driven set of rules that allows consumers to share their data with accredited third parties in order for them to provide products and services. CDR exists as federal legislation at the Treasury level, while the Australian Competition and Consumer Commission (ACCC) is accountable for accrediting potential data recipients, co-regulating compliance with the Office of the Australian Information Commissioner (OAIC) and providing guidance to stakeholders about their rights and obligations.

CDR is an economy-wide reform that will be rolled out sector by sector. It has been rolled out for the Banking and Energy sectors with Telecommunications to come.

What are the steps to get access? The government has mandated a number of ways to gain access to Open Banking data. There are a number of different models to get access to Open Banking data which brings with it different requirements. The Federal Government has incentivised smaller institutions and fintechs to drive innovation and competition in the market, which has led to the roll out of a number of access models to make Open Banking more accessible.

What are the Open Banking access models available?

Unrestricted ADR – Provides full unrestricted access to receive raw CDR data. Enables organisations to provide CDR services and act as a sponsor or principal.

Sponsored Affiliate The sponsorship model allows organisations to gain access to CDR data by using an unrestricted ADR as a sponsor. This model allows Sponsored Affiliates the same privileges and access to CDR data as an ADR, but at a lower cost and in less time

Principal Representative – This is primarily a business arrangement between an unrestricted ADR and an organisation, however it differs from the Sponsored Affiliate Model as there is no official accreditation required. Under this arrangement, a CDR Representative may only disclose data to their principal (each CDR may have one principal only under this model). This arrangement would also place responsibility (and liability) of the data squarely on the ADR.

Trusted Advisor – This model allows CDR data to be shared with trusted advisors, including financial advisors, mortgage brokers, accountants, tax agents and/or lawyers. Again, no external accreditation would be needed, just targeted access to specific data with the customer’s consent through an unrestricted ADR.

CDR Insights Model – This arrangement also does not require external accreditation, and can be utilised with any organisation who works with an unrestricted ADR. Under the CDR Insights Model, non-accredited parties would receive low-risk insights and data which would benefit their customers in specific ways. This could include verification and management of customer accounts, income, expenses and account balances.

Outsourced Service Provider – While not an access model, an ADR can disclose CDR data to a unaccredited Outsourced Service Provider (OSP) whom they choose to engage. An outsourcing arrangement must exist between the ADR and OSP. These services include the collection of CDR data on behalf of the ADR and the provision of goods or service using the CDR data that the OSP collected on behalf of the ADR.

CDR business consumer – A CDR business consumer is an entity, not an individual, that holds an active ABN. These entities must operate a B2B business and have the authority to consent to sharing their CDR data with various unaccredited third parties, under what is known as “Business Consumer Disclosure Consent.” Eligible third parties include lawyers, accountants, accounting platforms, bookkeepers, consultants, and other advisers.

How Open Banking works

Open Banking provides a secure method by which data can be shared by consumers to accredited third party organisations.

Mechanics of Open Banking Open Banking was designed to promote ability for consumers to be in control of who and how they share their data with accredited third parties. As such, the process is stringent considering the privacy and security concerns related to sensitive data. For consumers to share their data via Open Banking, the following steps will likely occur:

Consent Open Banking cannot exist without the consumers consent. Before anything happens, you must give permission for the provider to access your data, which you can do through the third party’s webpage or application. Equally as important is the concept of “ongoing consent”. The CDR has laid out key principles that must be abided by, and one of these is that consent must be “current”. Consent is only as current as the consumer’s original intent, so if attitudes and behaviours change over time, or are impacted by external events or consumer awareness, consumers can choose to revoke consent at their discretion.

Verify identity Verification of identity is key when dealing with sensitive information. Consumers will be required to identify themselves in order to share data to chosen third parties.

Confirm data sharing These checks and balances may seem tedious at first, but it is for the benefit of consumers. Consumers who use open banking will always be in charge of their data, and will need to provide granular consent whenever it is accessed by third parties. When consumers give access to a third party, the bank will confirm with the consumer the data to be shared, the intended purpose, and for how long, before they do so.

Data is shared and used Once confirmed, the data will be transferred using an API to the third party and it can then be utilised in providing the service to the consumer. Again, this will all be consented to by the consumer, who will always have the option of stopping data sharing, deleting data stored by third parties or changing the process in any way they see fit. Open Banking exists enable consumers to be in control of their data.

CDR’s Open Banking rollout in Australia

Open Banking will foster innovation and competition which benefits businesses and consumers. What made the concept feasible in Australia was the Murray (2014) and Harper (2015) reviews, followed by the Federal Government’s 2017 commission’s inquiry into Data Availability, which later triggered the Farrell report the following year which proposed the establishment of the CDR. This sparked the beginning of the CDR rollout which has matured over the years with an increasing number of participants joining the Open Banking ecosystem.

The Open Banking Timeline:

May 2017 – Government announces CDR commision

May 2018 – Government accepts recommendations and approves the phased implementation of Consumer Data Right. Four major banks are approached to make their data available

July 2019 – Major Banks provide product reference data on Phase 1 products, which include personal basic accounts, GST and Tax accounts, savings accounts and credit and charge cards. Visit the Australian government website for a full list of Phase 1 products

February 2020 – Participating banks provide product reference data on Phase 2 products like home loans, investment property loans and personal loans. Visit the Australian government website for a full list of Phase 2 products

July 2020 – Participating banks provide product reference for Phase 3 products, such as business finances, lines of credit and cash management accounts, as well as account and transaction data

November 2020 – Participating banks provide access to mortgaged personal loans

July 2021 – Other banks must join the participating banks in providing access to data for savings and transaction accounts (Phase 1)

November 2021 – Other banks must join the participating banks in providing access to home and personal loan data (Phase 2)

February 2022 – Other banks must join in providing access to business products, retirement accounts and foreign currency accounts (Phase 3)

July 2022 – Major banks to implement joint accounts changes for primary brands

October 2022 – Major banks’ secondary brands and other banks to implement joint accounts changes

November 2022 – All major banks’ secondary brands and other banks to implement phase 3 products

May 2023 – The Australian Government announces a further $88.8 million over two years from 2023–24 to support the operation of the Consumer Data Right across the banking, energy and non-bank lending sectors. The funding will also help progress design of action initiation and improvements to cyber security

June 2023 – Statutory Review of the Consumer Data Right outlines the Australian Government’s commitment to continue developing the CDR framework – See statement

Visit the CDR website and to learn more about the Rollout.

Which banks use Open Banking? All the major Authorised Deposit Taking Institutions in Australia are required to operate under the Open Banking framework, and many of the smaller and mid-sized banks such as non-bank lenders expected to come on board. See the full list of current data holders and recipients on the Consumer Data Right website.

Current state of Open Banking Over 100 data holder brands are now actively sharing data via Open Banking including Major banks and financial institutions. The Consumer Data Right website provides a view of who the Data Holders and their performance and availability.

How safe is open banking in Australia? Open Banking is a carefully regulated government initiative which can only be used by ADRs registered with the ACCC. When sharing financial data, a consumer is not required to to disclose their login and password details to an ADR (as they log in via the interface of the financial institution), meaning it a very secure method of sharing data using the financial institutions’ security measures. Consumers also have full visibility of who they have consented to sharing their financial data with, for what purpose and for what duration, with the ability to revoke consent and have their data deleted at any time.

What data is shared under CDR Open Banking? Open banking is used to provide insights into your financial data, and to allow ADRs to use your personal information in providing financial services products. This could involve providing services for lending, wealth and investing, personal finance management and many others. In order to do this, they need access to data related to your accounts, balance details and transaction details.

What data guidelines does the CDR prescribe? Stringent Consumer Data Standard (CDS guidelines) have been developed by the Australian Government to ensure that Consumer Data Right legislation gives Australians greater control over their data. These guidelines cover general standards, security profiles, consumer experience, banking, admin and common APIs, schemas, known issues and non-functional requirements.

Each organisation is also bound by the mandated security guidelines, and must have advanced security measures to ensure data can be shared without being compromised. These security protocols prevent security breaches, efficiently deal with breaches in the unlikely case that they occur, automatically review and prevent incidents happening in the future and optimise performance overall.

Open Banking on the global stage

Who are global Open Banking leaders? The Competition and Markets Authority (CMA) initiated open banking in the UK to generate competition and innovation in a market heavily dominated by large financial institutions. A similar concept was formulated under the name Second Payment Services Directive (or PSD2, for short) which Governed the EU. In 2018, and, under their mandate, nine of the largest banks in the UK began to implement open banking and produce open APIs to assist with the process.

Open Banking in Australia does have some key differences compared to its earlier counterparts in the UK and the EU. The core principles of Open Banking are the same between the two regions, however there are differences in approach, mechanisms and scope. For instance licensing is different, with Australia not having an equivalent to the UKs Payment Services Regulations (2017), however the overall requirements in both regions accomplish similar outcomes regarding regulation.

There are also many similarities. Firstly, the reasoning behind Open Banking is the same — to encourage competition in the market. Like Australia, the Open Banking ecosystem and its participants in the UK are strictly registered, and there is a standardised and mandatory way of collecting and sharing data, as well as how banks and third parties connect. Both regions use a central authority to prevent mishandling of data, issue certificates to trusted affiliates and identify each other.

Looking to the future of Open Banking

Open Banking has created new ways for consumers interact with their data, change the way businesses operate and yield economy-wide benefits. The ecosystem has continued to accelerate with more participants leveraging Open banking data to deliver their products and services to market. The new pathways to access Open Banking data announced in February 2022 has encouraged more participation as evidenced by the number of CDR representative arrangements.

To learn more about the future use case for Open Banking read the white paper.

Examples of Open Banking at work

Basiq allows customers all the tools they need to leverage financial data, access account and transaction data in real time, enhance transactions with merchant data, gain deeper insights into customer’s finances and, will eventually be equipped with insight-driven automation.

Open Banking – Frequently Asked Questions

What is Open Banking in Australia? Open Banking is an exciting initiative in Australia, and one which is primed to explode as more and more consumers uptake services with Open Banking-enabled capabilities and more companies realise the benefits for them and their customers.

Is sharing my financial data safe? Yes. In sharing your personal and financial data you are afforded the utmost consumer protections, architected by years of regulatory policy, technical design with privacy at the forefront., This is a highly secure initiative which is just as safe as sharing your personal data with your financial institution. Authorised banks and third parties must adhere to strict accreditation criteria to be eligible, so there is absolutely nothing to worry about. Your data is safe.

It is also important to keep in mind that you are completely in control of what data you share, and can revoke consent to share it at any time. In this case, all personally identifiable data will be deleted.

What banks use Open Banking? All the big banks now provide open banking, with many of the smaller and mid-sized banks quickly following suit. Over 200 Fintechs and banks rely on Basiq’s platform to share data and deliver innovative financial solutions across lending, payments, wealth and digital banking. The potential of Open Banking is generating huge growth and transition in the banking sector, and experts expect a boom in usage in the future.

See the full list of current data holders and recipients at the Consumer Data Right to familiarise yourself with the institutions involved in open data sharing.

What are some Open Banking examples? All of your banking, including changing banks, signing up for new credit cards or applying for loans or mortgages, will eventually ALL be able to be done over the internet through sharing of CDR data.

Investing can seem like a scene out of The Wolf of Wall Street. The stakes are high, the cash is thrown around like Monopoly money, and stock levels rise and fall like a rollercoaster. It’s loud, it’s fast and only a handful of people know the rules.

But this boys’ club vision of investing isn’t the only option. While getting into the market used to come with a big initial investment, things are changing. New fintechs are launching and listening to what today’s investors care about.

Research from the Responsible Investment Association Australasia (RIAA) reveals four in five Australians expect their money to be invested responsibly by super funds, banks and other financial institutions. Interestingly, 17% are already putting their money where their mouth is and investing in ethical products.

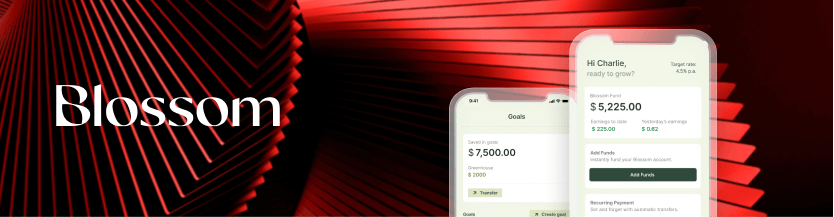

That’s exactly what fintech Blossom is committed to delivering. Blossom helps everyday Australians access fixed-income assets to watch their savings grow while knowing they’re putting their money into companies that are doing good.

We sat down with Blossom’s Co-Founder, Gaby Rosenberg to find out how Blossom approaches ethical investing and how they’re helping Australians reach their savings goals faster.

What is Blossom?

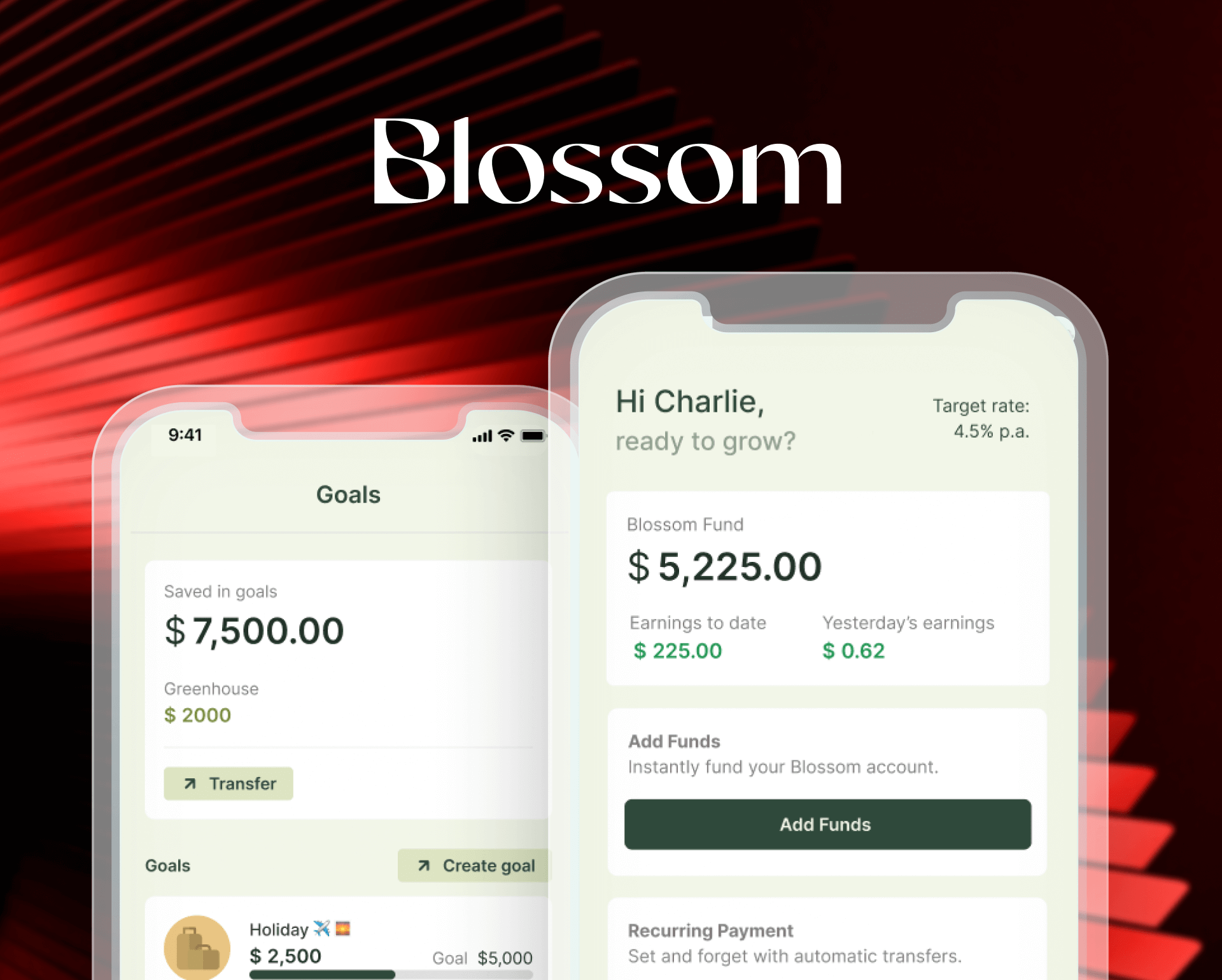

Blossom is an investing app helping everyday Australians access fixed-income assets to grow their savings.

Typically, fixed-income assets (which include corporate bonds, government bonds mortgage-backed securities, and more) have been only accessible to financial institutions, super funds, hedge funds, and high-net-worth individuals.

But, Blossom flips things on their head by allowing anyone to get started with no minimum investments, low fees and flexible withdrawals.

“Blossom democratises access to fixed income so that Aussies can grow their savings faster, easier and smarter,” explains Gaby.

Who is it for?

Blossom is an app for everyone. Rosenberg herself says the whole point of the app is to level the playing field to help everyday Australians take control of their savings.

Unsurprisingly, the Blossom app has already been a big hit with millennial investors, many of which care about where they’re putting their money. Interestingly, users aged 55+ are a growing cohort of users for Blossom, too. While it’s been a surprise to the team, Blossom is thrilled to be helping all Australians diversify their investments and add alternative assets to their portfolio mix.

“I think that the female demographic is really seeing themselves in what we’re trying to build from a responsible investment perspective… that’s becoming more and more important to this demographic,” tells Gaby.

How does it work?

Blossom makes it easy for users to get started and grow their wealth.

Download the Blossom app and make an account.

Transfer money into the account, whether that’s as low as $1, $5 or $10. There are no sign-up, transfer or withdrawal fees.

Set a savings goal.

Blossom posts users’ earnings daily so they can track and watch their savings grow.

Plus, users can link up their bank account and set up auto-grow (which offers round-ups on everyday purchases as well as instant PayID transfers).

The Blossom founder story

It was during COVID when the idea for Blossom started to form. After trying to get a handle on her own personal finances, Gaby started considering new ways to make her money work harder.

Luckily enough, she had a bunch of finance professionals in her family who would bring a lot of innovative ideas to the dinner table.

One week, fixed income was brought up and piqued her interest.

“It was an extremely attractive asset class for me, but something that I hadn’t made any investments in before. I felt immediately pressed out of the market and I decided that this was likely an opportunity that would be attractive to some of my friends, and some of my colleagues.

Then I started thinking about ways to tap into the trend of micro-investing by democratising access to new asset classes, like fixed income.”

Since launching in 2021, Blossom now boasts over 8,600+ customers and has $36 million (and counting) under management.

How does Blossom approach ethical investing?

Australian consumers are increasingly looking for sustainable, environmentally friendly and ethical products. In fact, 1 in 5 Millennials and Gen Xers are investing responsibly and making choices based on environmental and social issues.

But, companies are increasingly engaging in the practice of greenwashing.

Last year Australian Competition & Consumer Commission (ACCC) launched an investigation into misrepresentative environmental claims across a bunch of business sectors and the Australian Securities and Investments Commission (ASIC) is actively monitoring the market, taking action against greenwashing.

Gaby says responsible investing is at the heart of their brand with strict exclusion criteria around who they invest in (along with specific exclusions for industries like coal, oil, gas, child slavery, and weapons).

“Responsible investing is absolutely at the heart of our investment management philosophy and we care a lot about it at Blossom. Doing good for the world and the environment and delivering strong financial returns for investors is a moral and financial imperative for us,” explains Gaby.

Helping Australians ease money-related stress

It’s been a financially difficult time for many Australians with the annual inflation rate rising to 7.8% (the highest level since 1990). That means it has never been more important to build a healthy savings buffer and make our money work harder for us.

Blossom helps users grow their savings, currently offering 4.5% p.a. targeted returns.

To date, Blossom’s tools have helped real Australians reach big milestones, from saving up a deposit for their first home to growing a ‘rainy day’ fund and even preparing to start a family, too.

“We know that saving money starts with a plan, which is why we have savings calculators and savings goals built within the functionality of the app. Users can use Blossom to really build that plan as well as track and reach those savings goals,” reveals Gaby.

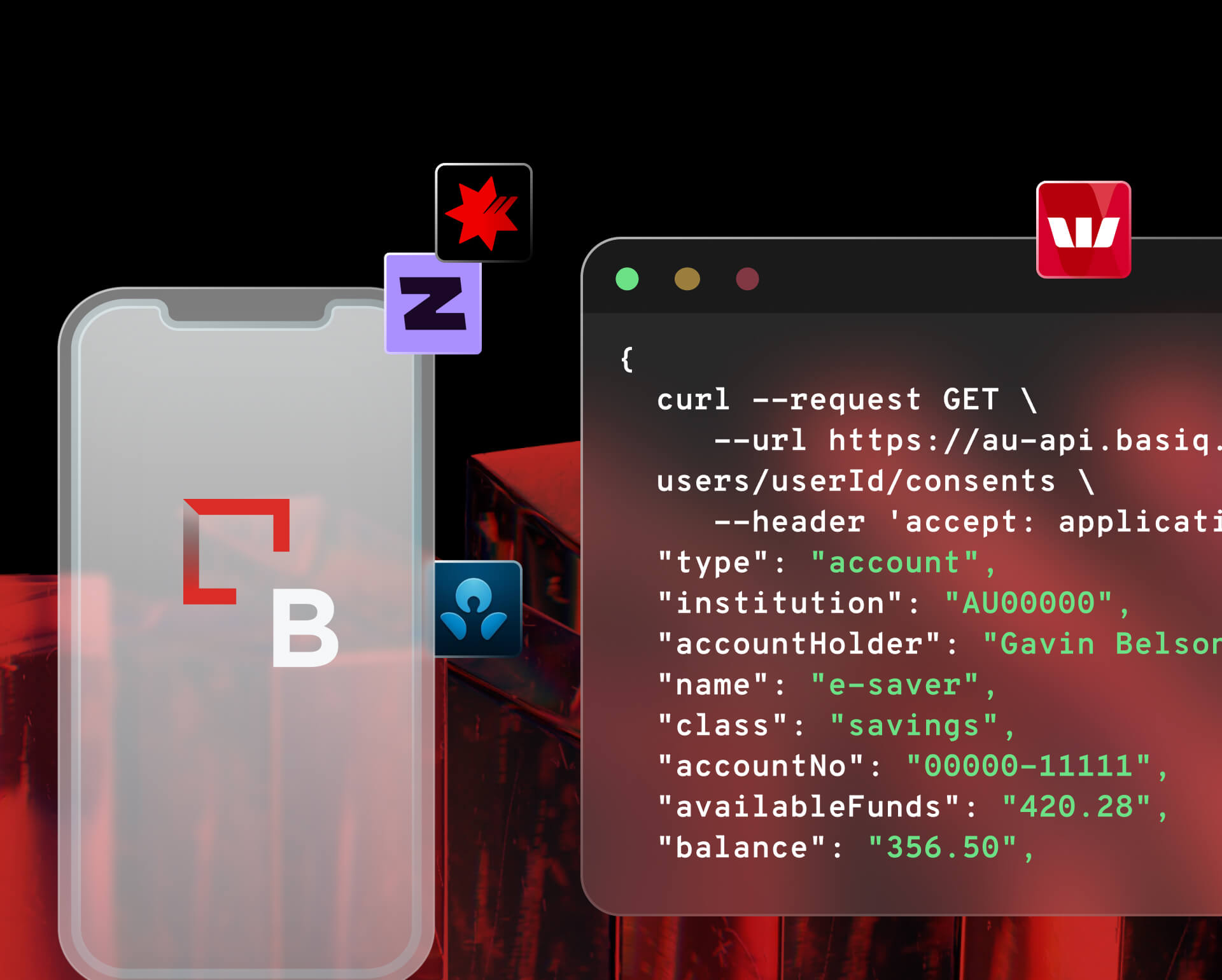

Accessing customer data via Basiq and the need for Open Banking

Gaby says Blossom has gained a lot of value from Basiq, specifically around accessing customer data to enable some of the app’s most important features.

“We take data from Basiq and we use it to enable our auto grow feature, which basically helps our customers round up their virtual spare change. With our auto-grow feature, users have really small and easy access to diversified portfolios like the Blossom fund. It gives customers an awesome way to get on top of their financial habits, build better financial habits and start investing in small and consistent ways.

We needed to access consented customer data across multiple institutions. Open Banking through Basiq was the best way for us to access that. It actually offers us strong fraud protection, which is not something that I hear people speak to often.

It helps us put protections in place to keep our customer’s savings, their accounts, all their data and information safe from financial crime, so that was a key piece of value we gained from Basiq,” tells Gaby.

A high level of support and a hands-on onboarding approach were big priorities for Gaby and the Blossom team, which is what attracted them to use Basiq as their Open Banking provider.

“We’ve had nothing short of an excellent experience so far. Every interaction we’ve had with the team from the moment of signing until we finished the signup and integration was professional, helpful, and super informative. Basiq is hyper-focused on Australia… they’re building a product that’s fit for purpose for us and the Australian market.

In terms of coverage, they offer the best Aussie bank coverage for Blossom to service our customers all over Australia (inclusive of customers who are banking with smaller institutions, too).”

What’s next for Blossom

Gaby says democratising access to fixed-income assets for Australians is Blossom’s main goal, along with helping users reach their financial goals.

The Blossom team are also working hard on a tonne of new features, including new investment offerings which will be announced later this year. Plus, they’re rolling out Blossom For Kids and working on a white-labelled partner offering called Blossom-as-a-service.

“This will allow partners of Blossom to unplug the Blossom app and plug in their own front end so that they can white label blossom and make it look and feel as they please and distribute it to their existing audience,” shares Gaby.

As a lender, you want to do everything you can to fast-track approval times, boost conversion rates and deliver a seamless customer experience.

But if you’re relying on web connectors (often referred to as ‘screen scraping’) alone to access customers’ financial data, you’re leaving your business vulnerable to disruptions that could encourage customers to abandon their loan application and take their business elsewhere.

Increasingly, Open Banking is becoming the preferred option for innovative lenders looking to stand out in a competitive market. In fact, lending is one of the most popular use cases for Open Banking.

With improved speed, connectivity, security and greater customer control, Open Banking benefits both the lender and their customers by enabling faster, more informed lending decisions that will help boost conversation rates.

The risks of accessing financial data via screen scraping

Imagine losing the ability to connect to customer financial data that sits with the major banks for a lending assessment. Whether you’ve encountered issues with transaction data to date or not, the consensus is clear: screen scraping to access banking data is on its way out.

Screen scraping is a degrading data access method, leaving lenders vulnerable to increased customer churn and negative brand perceptions, ultimately impacting the ability to attract new customers and their bottom line.

If access to financial data via screen scraping goes down during the application process, you lose access to the information needed to quickly and efficiently make a lending decision, leaving you unable to service that customer at that time.

Consumers have hundreds of options at their fingertips and are likely to look elsewhere if they encounter errors, issues or roadblocks such as failed screen scraping in the application process. Plus, screen scraping’s reliance on a customer remembering their online banking details can prove a major drop-off point, too.

Here’s what we know:

Online fraud is on the rise: Australian customers and businesses lost an estimated $4 billion to scams in 2022 (nearly double the losses reported in 2021). In the wake of major data breaches, banks are levelling up their security measures through steps such as multi-factor authentication.

The consequence? When it comes to web connectors, we are seeing a reduction in the speed data is returned, a decline in the reliability of some connectors and, in worst case scenarios, access to customer banking data is banned and only available via Open Banking (including Macquarie, HSBC and Qudos banks).

Consumers are hyper-security conscious: there have been a number of high-profile data breaches impacting Australian consumers over the past 12 months. With online fraud top-of-mind, consumers are more vigilant than ever when it comes to sharing their personal information. This could impact their willingness to share the login details required to access data via web connectors.

Screen scraping will be banned: significantly, the final paper from the Statutory Review of the CDR recommended banning web connectors in the near future when a viable alternative, such as Open Banking, is available. Our observations of CDR’s maturation indicates this day is quickly approaching and businesses will be forced to make the switch.

In contrast, Open Banking platforms will only get better with maturity. Already, the Open Banking ecosystem boasts 114 banks providing access to Open Banking data with a 98.88% connectivity success rate when data is requested (as of 1/3/23).

What is Open Banking?

Launched in 2020, Open Banking is part of the Australian Government’s Consumer Data Right (CDR). Its aim is to give consumers greater control over their data, enabling them to securely share it with service providers (like lenders), drive industry competition, and support the development of new, innovative financial products and services.

Ultimately, it’s the best way to future-proof data access, particularly for lenders looking to provide a fast, convenient digital experience to their customers.

The benefits of Open Banking for lending

At all stages of the lending lifecycle (from credit risk analysis and credit checks to settlement and repayments), creating and delivering value to your customers, while minimising risk to your business, is a top priority.

Open Banking gives you the speed, reliability and security you need to get to ‘yes’ sooner, enabling automated credit decisioning and reducing loan application abandonment.

Along with helping to adhere to responsible lending guidelines, Open Banking offers rich data and insights your business needs to proactively identify new opportunities to support and service your customers.

For lenders, Open Banking:

Boosts conversion rates and lowers credit application abandonment: we have already mentioned customers expect a fast and streamlined application experience that Open Banking can help deliver.

For major banks, the average connection time with Open Banking is 5x faster than via screen scraping.

Plus, rather than relying on customers to remember their banking password (a significant issue when it comes to failed access via screen scraping), with Open Banking they securely login using their banking ID, mobile number and a one time password which boosts the chance of a successful connection by 30%.

Frictionless access to customer data means a faster time to ‘yes’ and makes for a winning customer experience.

Expands the scope of products and services lenders can provide and recommend: Open Banking enables access to more data attributes (more info below), in real time, via a one-time consent process where ongoing data access is available to the lender until it is withdrawn by the customer.

This is a game changer for lenders, enabling them to shift from a single to multi-use service. Continued access to data via Open Banking means they can maintain their responsible lending obligations through the entire loan lifecycle and nip issues in the bud before they arise.

For example, lenders could check whether customers have sufficient funds before taking a payment that could prevent dishonour fees if the funds are not available. They could proactively offer budgeting tools or tailored payment plans for customers experiencing financial hardship, or dynamic interest rates that adjust depending on financial behaviours.

Open Banking allows lenders to service and support their customers better, leading to greater customer satisfaction and retention.

More customer information at a lender’s fingertips to assist with credit decisioning: As we mentioned above, Open Banking allows access to data attributes not available via screen scraping, including additional account and transaction information.

Account data via Open Banking offers a host of additional attributes relating to product interest rates and fees. When it comes to joint accounts, lenders can identify whether a customer is the owner of the account and from July this year they can view the number of account owners.

For transaction data, Open Banking offers a lot more data relating to payees and direct debits, as well as merchant name and merchant category code.

Enables access to a wider pool of potential customers: as more institutions prevent screen scraping access to banking data and fully commit to Open Banking, lenders are able to service more customers than ever before. For example, HSBC, Qudos and Macquarie Bank don’t allow access to customer banking data unless it’s via Open Banking. What does this mean for lenders relying on screen scraping? Potential customers with these institutions will find it difficult to apply for products because they aren’t able to share their data during the application process.

Unprecedented collaboration with financial institutions: Open Banking has seen banks and Accredited Data Recipients (ADRs) like Basiq working collaboratively to improve the reliability of connections, fix data and access issues and enhance performance.

Open Banking empowers lenders to upgrade and reimagine the experience of accessing online loans. With assessment tools and ongoing access to customer data at their fingertips, they can make more informed decisions, improve approval times and boost conversions.

How Basiq is helping lenders transition to Open Banking

The benefits of Open Banking for lending are clear, but we know that making the switch from screen scraping can seem daunting and complex.

The future is now, which is why we’re calling on businesses (like lenders) to make the switch to Open Banking.

Sydney, 15 June, 2017 – Samsung Electronics Australia today announced a partnership with Cuscal, Australia’s leading independent provider of payment solutions that will enable 38 financial institutions to offer Samsung Pay.

Samsung Pay is a secure and easy-to-use mobile payments service available on compatible Samsung devices including the Gear S3 smartwatch and the Galaxy S8 and S8+ smartphones1.

People’s Choice Credit Union, Credit Union Australia (CUA), and Teachers Mutual Bank are among some of Cuscal’s clients now offering Samsung Pay and the partnership will enable mobile payments for a combined total of 1.7 million cardholders.

Cuscal joins Westpac, Citibank and American Express as Samsung Pay partners.

Richard Fink, Vice President, Mobile Division at Samsung Australia said:

Through Samsung Pay’s partnership with Cuscal we are providing millions of Australians a convenient and safe payment option. Every partner we bring onboard, whether it be a financial institution or retail brand through our Samsung Pay loyalty functionality, brings us a step closer to helping customers replace their wallets with their Samsung smartphone or smartwatch.

The announcement comes as Samsung Pay marks its first anniversary in Australia. During its year of operation in this country, Samsung has now partnered with over 40 payment card brands and has over 100 different types of loyalty cards loaded onto Samsung Pay – making everyday payments and loyalty point collections simple and secure for Australians.

Robert Bell, General Manager of Product & Service at Cuscal said:

We’re really pleased that our clients’ customers can now use Samsung Pay. Our aim is to allow all of our clients to offer their customers the newest and best payment options available, to help them compete with much larger players. With the addition of Samsung Pay we continue to fulfil this promise to them.

Cuscal’s 38 financial institutions now available on Samsung Pay are: Australian Unity, Bank Australia, Bank of Sydney, Beyond Bank Australia, Big Sky Building Society, Catalyst Money, Central Coast Credit Union, Central Murray Credit Union, Community First Credit Union, Credit Union SA, CUA, Customs Bank, Defence Bank, Firefighters Mutual Bank, First Option Credit Union, Holiday Coast Credit Union, Horizon Credit Union, Illawarra Credit Union, Intech Bank, MyState, Nexus Mutual, Northern Beaches Credit Union, P&N Bank, People’s Choice Credit Union, Police Bank, QT Mutual Bank, Queenslanders Credit Union, Reliance Bank, SCU, Select ENCOMPASS Credit Union, South West Slopes Credit Union, Teachers Mutual Bank, The Mac, The Rock, UniBank, Unity Bank, WAW Credit Union Co-Operative, Woolworths Employees’ Credit Union Limited.

Samsung Pay has more than 870 bank partnerships worldwide and there has been more than 240 million transactions processed over the past year and a half.

1 Samsung Pay is available on the Samsung Galaxy Note 5, Galaxy S6, S6 edge, S6 edge+, Galaxy A5, Galaxy A7, Galaxy S7 and S7 edge and from April 28, 2017, the Galaxy S8 and S8+. Compatible wearable devices include the Gear S2 and Gear S3 smartwatches. Samsung Galaxy S6 and S6 edge do not support the MST functionality of Samsung Pay.