Have you ever wished your systems could talk to each other automatically without you having to constantly check for updates? That’s where webhooks come in. Webhooks are like messengers that instantly notify your system when something important happens. This way, you can automate processes and get real-time updates without any manual intervention.

What’s new?

We’ve recently rolled out enhancements to our webhook system to make them more efficient and valuable.

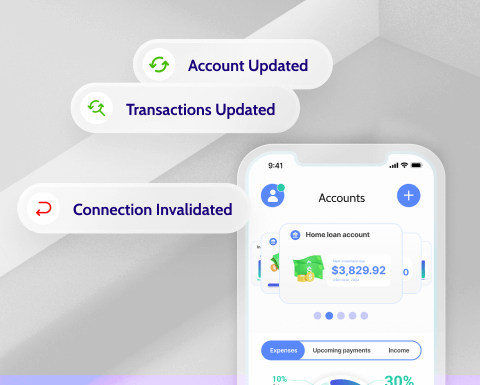

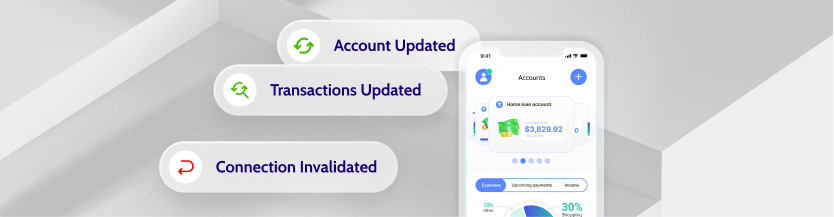

Hello to meaningful events

account.updated: This event is triggered when there are changes to an account’s details (excluding balance changes). This means you’ll get notified if any details like account name or type change, but not for balance changes.

transactions.updated: This event is triggered whenever new transactions are added for a user. This helps you keep track of all transaction activities without being bogged down by minor updates.

connection.invalidated: This event will notify you when there’s an issue refreshing data due to user-related errors like password changes or multi-factor authentication (MFA) issues. This way, you’ll know when something requires your immediate attention.

Why the change? Previously, the connection.updated events were overwhelming and often required multiple API calls to find relevant information. This made the data less meaningful and actionable. Our goal with these new events is to provide updates that are directly useful and can help you make informed decisions quickly.

A few examples of how you can use events and webhooks in your application

Lending and Financial Decisions

transactions.updated: Lenders can use this webhook to get real-time updates on a borrowers’ financial activities. For instance, when a borrower’s salary is deposited, you can automatically process loan payments.

connection.invalidated: This webhook alerts you when there’s an issue with user authentication. For lenders, this means you can quickly address authentication problems, ensuring a smooth customer experience.

Account Management

account.updated: Financial institutions can use this webhook to monitor changes in account details. For example, if a user updates their account information, you can automatically update your records, ensuring accuracy and compliance.

Future enhancements

We are continuously working on making our webhooks smarter and more intuitive. Stay tuned for future updates that will bring even more value to your automated processes.

Get started with webhooks

Are you ready to implement these enhanced webhooks in your products or applications? Don’t miss out on valuable insights and automation opportunities. Check out our developer documentation to get started today!

In a recent speech by Assistant Treasurer Stephen Jones at a CEDA (Committee for Economic Development of Australia) conference, significant changes were announced that aim to reshape Australia’s digital economy, focusing on the Consumer data right (CDR), privacy, and cybersecurity. The speech highlighted both the benefits and challenges brought by the digitisation of the economy, emphasising the need for stronger protections and more effective use of consumer data.

A focus on Privacy and Data protection

The speech underscored the importance of data in the digital economy, recognising the growing concerns among Australians about privacy due to rising incidents of cybercrime and data breaches. To address these concerns, the government is reviewing the Privacy Act to ensure it is fit for the digital age. This review will impose higher standards on businesses to protect customer data.

Heidi Richards’ CDR compliance costs review report, released by Assistant Treasurer Stephen Jones, found that the costs of the Consumer Data Right (CDR) have far exceeded original estimates, with large banks facing significant burdens due to complex technical requirements. The report raises concerns about the rapid changes to CDR rules, low customer usage, and the lack of innovation, partly due to restrictions on using CDR data. Businesses haven’t been incentivised to use CDR data, which has hindered broader adoption and innovation. The report calls for clearer strategic planning and prioritisation of future changes.

The speech acknowledged that the current implementation of the CDR has been flawed, with high regulatory burdens, low uptake, and limited innovation. To address these issues, the government is launching a reset of the CDR, focusing on several key areas that include:

Streamlining consent processes: The government will simplify how consumers give consent to use their data, allowing for multiple consents in a single action, making it easier and more user-friendly.

Improving business access: The government will mandate that data holders, such as banks, provide a straightforward process for businesses to access their own data. This will help businesses, especially small ones, to benefit from the CDR.

Consumption of CDR data: New rules now allow accredited deposit-taking institutions (ADIs) who are data holders to hold consumer data under the Consumer Data Right (CDR) when a consumer applies for or acquires a product. ADIs must notify consumers that their data will be held and inform them of relevant privacy safeguards. This could help accelerate the use of CDR data by banks who are data holders.

Reforming Standards and Costs: The government will introduce a more structured approach to making standards changes. This includes limiting changes to a few scheduled releases per year, ensuring longer lead times, and considering the cost and regulatory impacts on participants.

Focusing the scope of CDR: To reduce unnecessary costs, the government is examining the possibility of narrowing the scope of data included in the CDR, removing products unlikely to be used.

Prioritising high-value use cases: The reset will prioritise consumer finance, energy switching, and accounting services for small businesses, where the potential benefits to consumers are highest.

Sector expansion: It was confirmed that Data holders would be extended to non-bank lenders to be operational by mid 2026.

The speech also highlighted the ongoing efforts to strengthen cybersecurity through the National Cyber Security Strategy and modernise the payments system. The government is committed to ensuring that digital identity systems, which simplify and secure the verification process, will reduce the amount of data businesses and governments need to hold, further protecting consumers. There was also a commitment to align CDR development with Digital ID, Payment system reform and Privacy act reform.

A significant announcement was the government’s stance on screen scraping, a practice where businesses ask consumers to share their bank passwords. The government is considering a full ban on screen scraping, emphasising that it is fundamentally unsafe and that the CDR should become the system of choice for data sharing. With a commitment to phase out screen scraping, the next 12 months will see Treasury develop a full transition plan.

Since launch, the Consumer Data Right (CDR) has been “read-only,” allowing data recipients to access and use the data for purposes like lending assessments, budgeting tools, and product comparisons. However, the introduction of the new action initiation power will add a “write” capability, enabling recipients to not only view the data but also perform actions on behalf of customers, such as making a payment, switching providers and updating personal details using the CDR framework.

Amends the Competition and Consumer Act 2010 to establish action initiation reforms, enabling consumer data right (CDR) consumers to direct accredited persons to instruct on actions on their behalf, such as making a payment, opening and closing an account, switching providers and updating personal details, using the CDR framework.

On the same day as Assistant Treasurer Stephen Jones announced the CDR reforms, the Senate passed the CDR action initiation bill. While this is exciting news, the government will still need to consult with industry stakeholders to determine its application, and detailed rules will need to be established.

The speech marked a pivotal moment in the government’s approach to the digital economy, with a clear commitment to improving the CDR, enhancing privacy protections, and fostering innovation. The reset of the CDR aims to reduce costs, encourage adoption, and ensure that consumers truly benefit from the data they generate. By focusing on these areas, the government hopes to build a digital economy that is both safe and innovative, where consumers can trust that their data is protected.

To date, Basiq has enabled over 900,000 Open Banking connections between consumers and businesses to help with tasks such as budgeting, investing, tax reconciliation and loan applications. It’s expected that by December 2024, the number of Open Banking Connections will hit 1.3 million.

The report analyses connection data from the Basiq platform including volume, success rates and ongoing performance, benchmarking it against the performance of web scraping. Web scraping, also known as Digital Data Capture (DDC) or screen scraping, is the widely used alternative and predecessor to Open Banking.

Analysis of the data has revealed three key findings:

Finding 1: Open Banking growth is booming

The popularity of Open Banking is steadily increasing, challenging the perception of slow growth and minimal uptake. Between October 2022 and March 2024, Open Banking experienced a 30 per cent compounded growth rate on the Basiq platform, with connections rising from 10,400 to 777,000. In the last 12 months, almost 50 per cent of all new connections on the Basiq platform were made via Open Banking.

Finding 2: Open Banking leads to more customers

Contrary to the belief that Open Banking results in high consumer drop-off, Basiq has found its success rate is almost double that of web scraping, with 80 per cent chance of success compared to 42 per cent. Financial institutions implementing more robust anti-scraping measures and heightened business and consumer concerns regarding data security are impacting connection success rates.

Finding 3: Open Banking is superior for ongoing connections

Only 0.17 per cent of Open Banking connections face disruption after six months, compared to 15 per cent for web scraping, making Open Banking 88 times more reliable for businesses requiring ongoing connections, such as budgeting or investment apps.

“We wanted to release our findings publicly to challenge the existing negative Open Banking narrative and provide a more optimistic perspective backed by data,” said Damir.

“While Open Banking is far from perfect, the highly critical views circulating do not reflect the reality we see,” Damir continued. “Our platform data and customer feedback tell a very different story – one of growth and success.”

“Acknowledging that connection performance is only one factor impacting Open Banking’s growth, we intend to dive into other key topics, including data quality, in future reports,” closed Damir.

Trust accounts are a fundamental vehicle for individuals and organisations to safeguard and manage assets for designated beneficiaries. They play a vital role in protecting assets and ensuring their proper distribution, a common practice in industries such as medicine and law, as well as in charities, estate planning, and investments.

The challenges of reconciling Trust accounts

The reconciliation of trust accounts involves collating data from various sources including bank statements, client records, and internal systems. Consolidating and reconciling data from these disparate sources is a labour-intensive process.

It can involve requesting and uploading bank statements and meticulously matching transactions, a tedious process that consumes valuable time and resources. As a result, it can be prone to inefficiency and errors which can jeopardise the integrity of the trust and expose it to the risk of misappropriation.

Using Open Banking

Open Banking provides an avenue to optimise the trust account reconciliation process by enabling access to real-time data from banks.

1. Save time and money Say goodbye to manual requests and uploads. Open Banking facilitates swift access to real-time banking data, eliminating cumbersome paperwork and expediting the reconciliation process. By automating routine tasks, financial professionals can focus on value-added activities, saving time and reducing costs.

2. Streamlined access Navigate multiple consent flows with ease. Open Banking offers a unified method for accessing banking data from various accounts, simplifying workflows and enhancing convenience. With just one consent, financial professionals can access a wealth of information, making trust account management more efficient, especially when ongoing access to banking data is possible.

3. Easily spot irregularities Access to real-time banking data means the process of identifying discrepancies becomes straightforward. Whether it’s an outlier transaction or a mismatched entry, ensuring accuracy and compliance is a straightforward process.

4. Data insights Access to real-time banking data through Open Banking allows for data-driven insights that can inform strategic decision-making. Financial professionals can analyse trends, identify patterns, and make informed decisions to optimise trust account management strategies.

Accessing Open Banking with Basiq

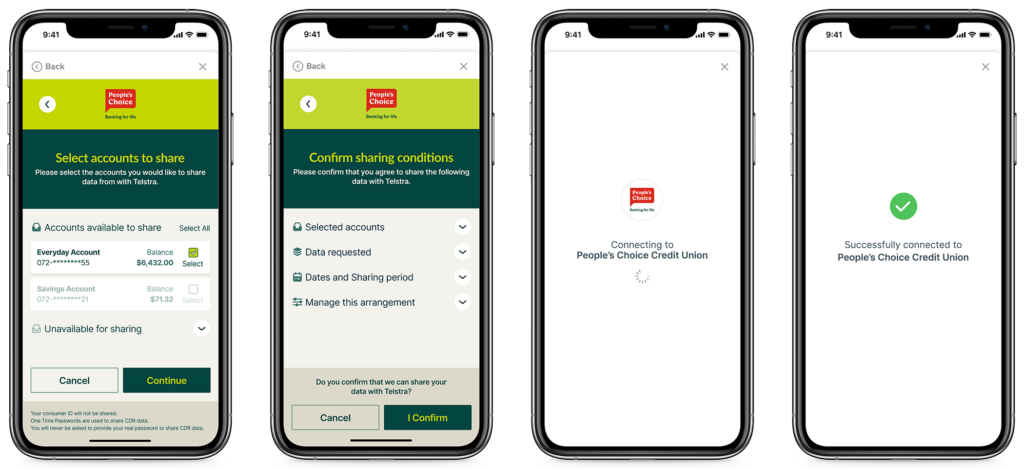

Accessing Open Banking via the CDR is a straightforward process where the owner of the bank account consents to their data being shared. The user is redirected to their respective bank to login via their Internet banking portal.

Once the respective bank account is selected the data can be shared with ERP systems, accounting software and specific trust accounting software to optimise the reconciliation process.

In today’s fast-paced financial world, lenders and brokers face the constant challenge of providing quick and accurate financial assessments to banks to process loans. Although core lending decisions often rely on comprehensive Consumer Affordability Reports, banks still require a traditional bank statement as part of the supporting documentation. Basiq’s new Bank Statements product is a tool that complements our existing insights affordability solution, offering a streamlined way for financial assessments to be shared with banks.

Traditionally, obtaining these statements involves a cumbersome, manual process that can delay decision-making and frustrate both lenders and customers alike. This need for speed and precision in financial assessments highlights a critical gap in the current tools available to lenders.

Understanding the pain points

Inefficiency: Traditional processes for retrieving and verifying bank statements are notoriously slow and can lead to significant delays in loan approval.

Lack of standardisation: Each bank may have different formats and data availability, complicating the assessment process for lenders who deal with multiple banks.

Compliance and accuracy concerns: Ensuring that the bank statements are compliant with regulatory requirements and accurately reflect the customer’s financial status is paramount, yet challenging due to varying data quality.

Bank Statements; a Basiq Insights solution

To address these industry-wide challenges, Basiq’s Bank Statements innovate on how financial assessments are conducted and shared with banks. Bank Statements compliments our existing Insights Affordability solution, providing a seamless and efficient method for generating accurate, compliant bank statements for lenders.

Key Features of Basiq’s Bank Statements

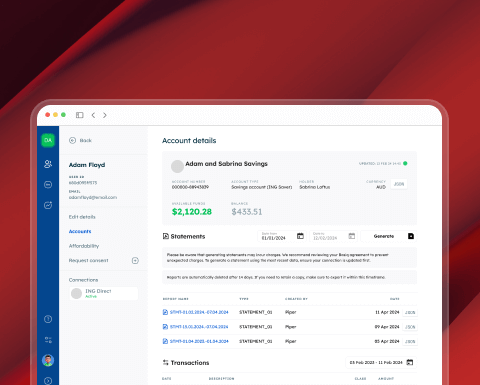

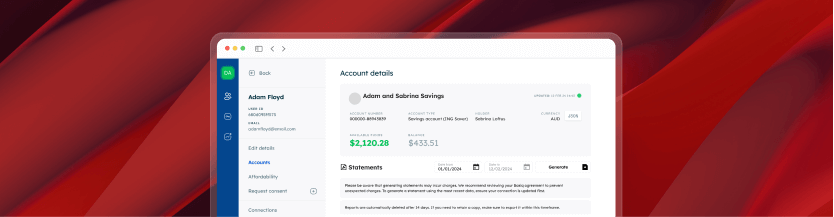

Access via API or our no code dashboard: Basiq’s Bank Statements can be generated through two convenient methods: via our robust API for seamless integration into existing systems, or through our intuitive no-code dashboard, which allows partners to generate and download statements in a PDF or JSON format without any technical expertise.

Single account focus: Tailors statements for individual or joint accounts while presenting details clearly and compliantly.

Custom date ranges: Enables customisation of the statement period by allowing users to easily select how far back they want to go, with the ‘To Date’ automatically set to the date the account was last refreshed to ensure the data is timely and relevant.

Logical running balances: Calculates logical running balances based on the transaction order, providing a comprehensive financial overview even when CDR data lacks a running balance.

Accreditation and Branding: Includes the logo and accreditation details of the institution, enhancing trust and credibility in the statements provided.

Basiq’s Bank Statements is an exciting step in the journey towards making financial processes more efficient and less burdensome for lenders. By addressing the key pain points in traditional bank statement processes, it enhances both the speed and quality of financial assessments, empowering our customers to make faster and more informed lending decisions.

Developer Resources

Explore our Basiq developer resources to understand more how you can integrate bank statements into your solution.

The Consumer Data Right (CDR) in Australia has recently undergone significant updates, especially with the introduction of Business Consumer Disclosure Consent. This new form of consent broadens the horizon for business consumers, allowing them to share their CDR data with a wider array of service providers, beyond the traditional “Trusted Adviser” list. This list initially included professionals such as accountants and lawyers but now extends to include service providers like bookkeepers, finance brokers, insurance brokers, and business coaches.

So what’s the TLDR around business consumer consent?

Getting straight to the point, the new CDR updates include:

Introduction of Business Consumer Disclosure Consent: Expands data sharing options for business consumers, facilitating sharing with a broader range of third party service providers.

Greater Flexibility with CDR Data: The V5 Rules update permits data sharing with software applications used for financial administration, offering substantial benefits for service providers and small businesses.

Encouraging Open Banking Adoption: Tailored for “business consumers,” this update opens up new opportunities for sharing financial data, crucial for accessing various funding options.

So what are the benefits for service providers?

Expanding Data Sharing Capabilities with less legal requirements: Service providers are able to access valuable CDR data and use it based on their existing business agreements without being bound by CDR rules.

Streamlining Financial Operations: With access to a broader range of applications for financial administration, businesses can streamline operations such as payroll, invoicing, and more.

Facilitating Access to Funding: The ability to share bank statements with finance brokers more efficiently opens up a plethora of funding options for businesses.

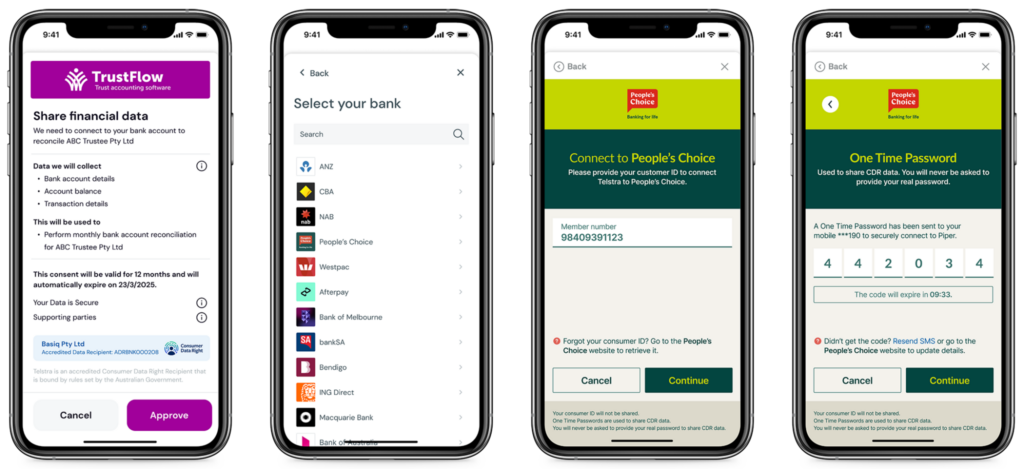

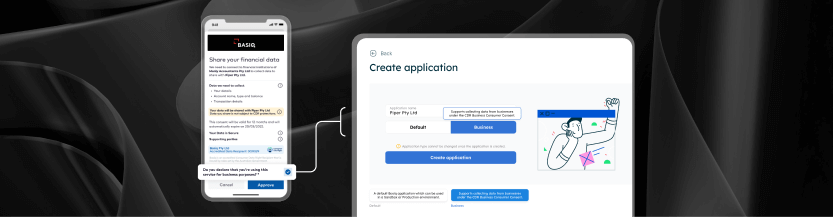

Business Consumer Disclosure Consent via Basiq’s consent UI

The recent updates to the CDR, present a new opportunity for businesses to engage in data sharing. Basiq’s consent UI has been enhanced to accommodate these changes, ensuring that businesses can leverage our platform to share financial data with a broader array of service providers. This enhancement is integrated into our existing consent UI, ensuring that the user experience remains consistent and intuitive.

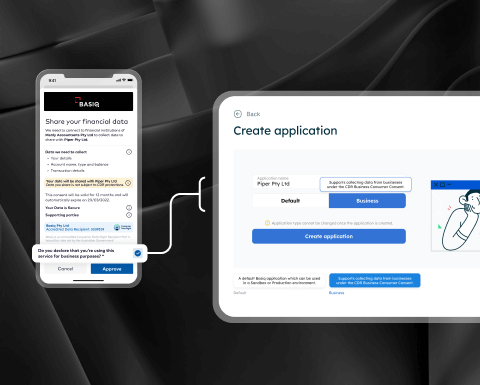

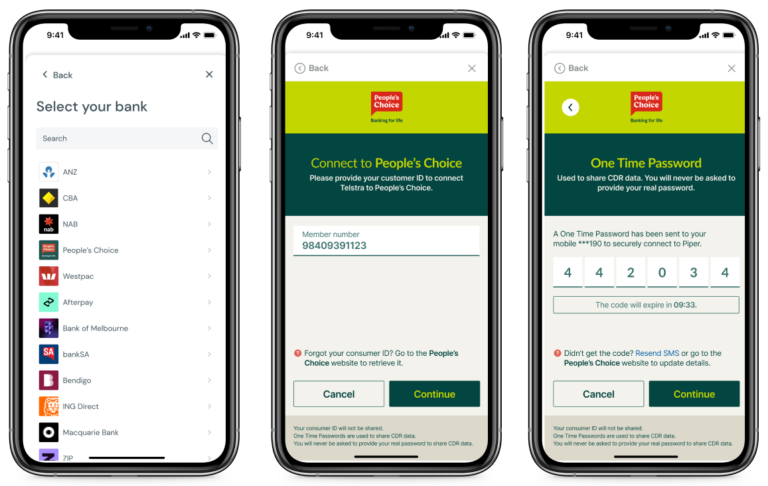

So let’s take a closer look The service provider Piper is wanting to collect business account details from a customer so they can offer a better service for their customer. They have integrated with Basiq to use their consent UI solution to allow their business customers to securely connect and share their bank account details in order to speed up this process and reduce manual processing.

The customer is met with a pre-consent screen within the piper application.

When they agree to continue they are taken to Basiq’s consent UI flow to facilitate the secure access to account details through a relevant financial institution.

The user is presented with details on; who has requested them to share the data (piper) and who is securely collecting it on Piper’s behalf (the ADR – Basiq), what details are being collected, for what purpose and for how long this consent will be valid for.

The Basiq consent UI simplifies the complex and verbose consent flow established by the ACCC and DSB CX (Customer Experience) guidelines. Our focus has always been to strike the perfect balance between compliance with the Consumer Data Right (CDR) regulations and offering an intuitive, user-friendly experience that maximises conversion rates. It aims to:

Reduce Drop-offs: By simplifying the consent flow, we aim to decrease the likelihood of users abandoning the process.

Increase Transparency: Users are well-informed about the specifics of the data sharing agreement, fostering trust and confidence in the process.

Maximise Engagement: A streamlined and user-friendly consent process encourages higher engagement rates, benefiting all parties involved.

The updates to Australia’s Consumer Data Right (CDR), featuring Business Consumer Disclosure Consent, significantly broaden the scope for financial data sharing, enhancing operational efficiency and financial management for businesses. The integration of these updates into the Basiq consent UI simplifies the data consent process, ensuring compliance while optimising user engagement. It enables service providers to offer more tailored solutions, streamlining operations and reinforcing trust in data sharing.

As open banking evolves, Basiq continues to innovate, empowering clients and their customers to maximise the value of their financial data.

Resources Have a read of our developer documentation to understand how you can get started with BCDC.

The closure of more than 1.4 million superannuation accounts in 20231, accompanied by disbursements exceeding $58 billion1, creates ample opportunities for exploitation by fraudsters. Manual methods employed for verifying bank account information are not only time-consuming but also prone to errors, providing openings for fraudsters to gain access to these substantial funds.

Unauthorised access to Superanuation funds

Incidents of identity theft further contribute to fraudulent activities, enabling unauthorised access to superannuation accounts. The prevalence of data breaches over the last few years, leading to the exposure of personal and financial data, offers fraudsters the necessary information for the manipulation or misuse of superannuation accounts.

Armed with this stolen identity data, perpetrators are able to assume the identity of their victims, navigating past security protocols to gain unauthorised access to superannuation accounts. Once inside, they are able to execute unauthorised withdrawals of substantial sums of funds.

As criminals evolve in their strategies, the urgency to fortify the security measures within the superannuation sector becomes increasingly apparent.

The use of Open Banking

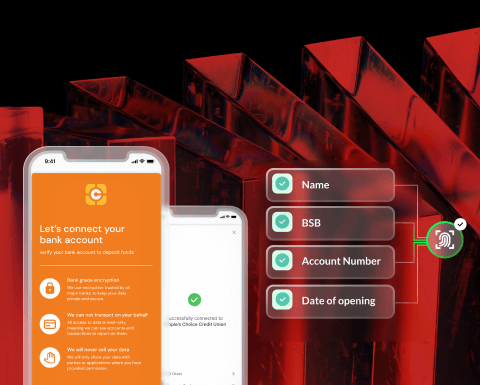

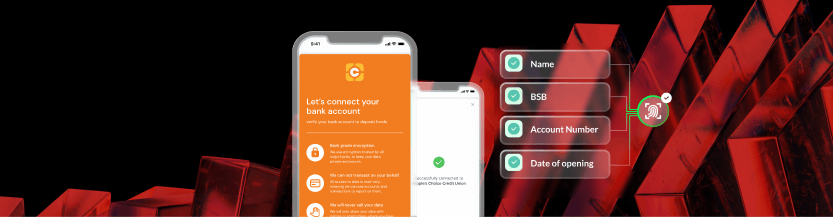

Connect by Basiq offers a comprehensive solution to fight fraud through real-time bank account verification, ensuring that superannuation withdrawals are seamlessly transferred to the intended recipients. Basiq streamlines the account verification process through secure Open Banking authentication, eliminating the need for consumers to disclose sensitive login/password information. Members initiating fund withdrawals online are simply redirected to the website/app of their nominated bank account, creating a secure and user-friendly experience while eliminating traditional steps of asking for bank account details.

TelstraSuper has embraced Open Banking to mitigate the risk of fraud. By leveraging Open Banking, TelstraSuper validates member bank account information swiftly and securely, facilitating faster transactions without the need for cumbersome hard-copy documentation.

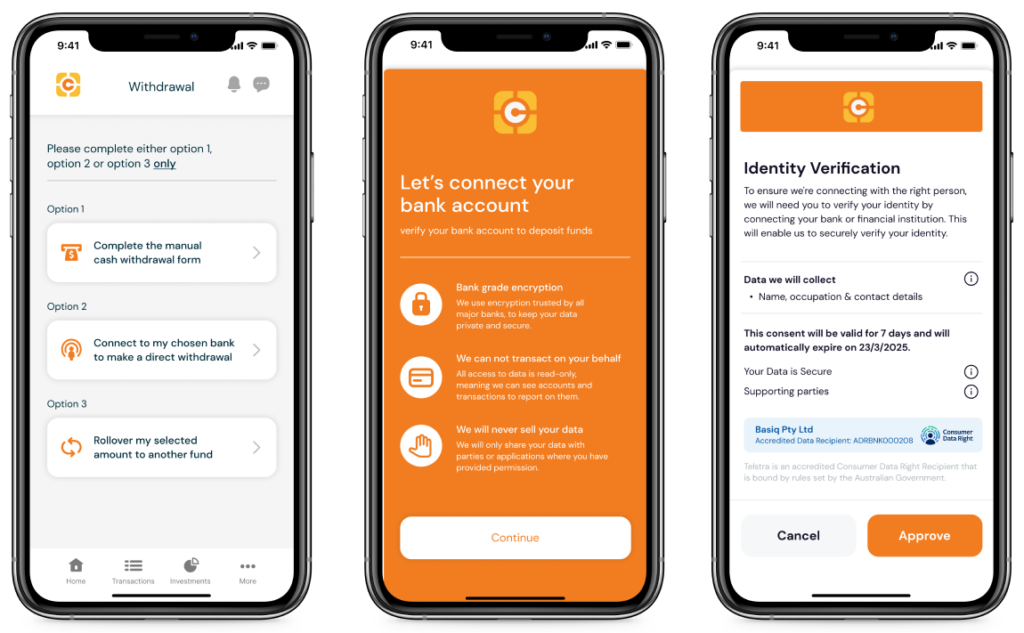

How does it work?

Step 1 – Member opts to transfer funds into their bank account

Step 2 – Member verifies by logging into their bank account

Step 3 – Once their bank account is successfully verified and connected, the amount to be withdrawn can be processed

Other benefits of Open Banking for Superannuation

Connecting a user’s bank account extends beyond verifying the account for transferring Superannuation funds. Financial data retrieved through the member’s various financial institutions helps create a comprehensive financial picture. Such insights enable financial advisors to provide more accurate and tailored advice, enhancing the overall financial guidance provided to superannuation members.

In addition, financial data can be used to help improve member engagement. By integrating a member’s financial data from different institutions with their superannuation data, a consolidated view of their net wealth can be created. This consolidated view allows for the development of user-friendly tools like dashboards and real-time alerts, helping members stay up to date and engaged with their financial journey and goals.

1Based on analysis from publicly available information on superannuation funds and administrators

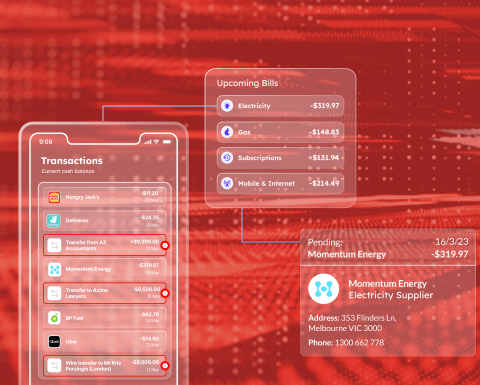

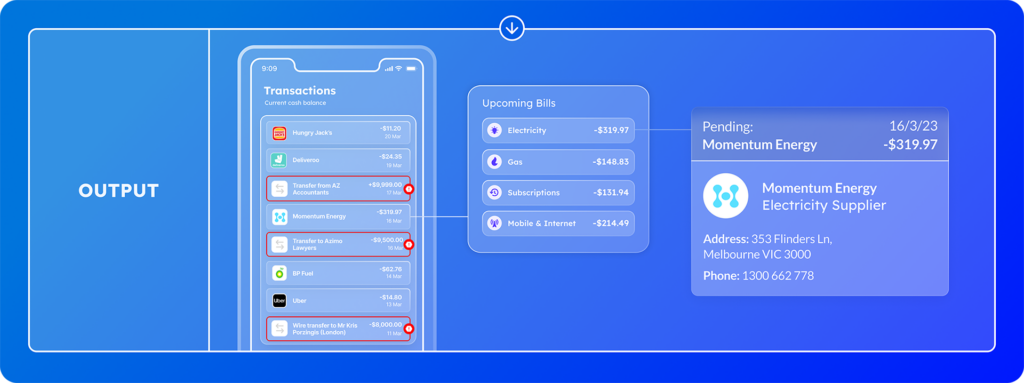

Looking at your banking app, what was the last purchase you made? Depending on your bank, you might see the:

merchant name (maybe even their logo?)

amount spent

time of purchase

geographic location

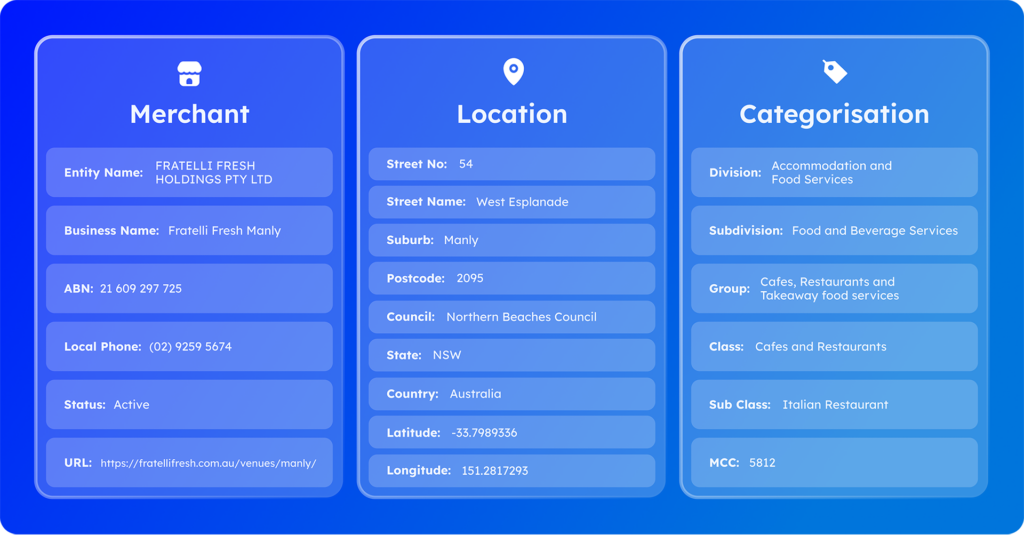

What you don’t see is the refinement process the transaction data goes through before it’s displayed. This is called data enrichment. It takes the messy raw transaction data and turns it into clean descriptions by adding the merchant’s identity, location and categorisation details (as seen below).

Let’s go behind the scenes and explore how we turn data into insights using Basiq Enrich.

The data enrichment process

Enriching banking data via the Basiq platform is a four-step process:

Data access

Data tagging, cleaning and tokenisation

Data enrichment

Machine Learning and final output

Let’s go over each in more detail.

Step 1: Data access

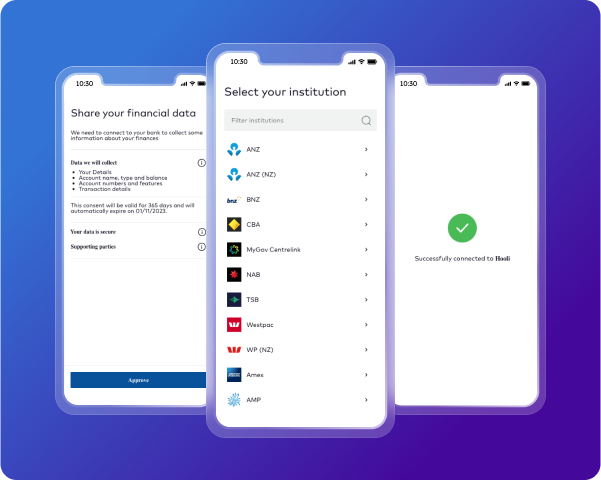

The first step is accessing a customer’s transaction data. To do this, customers consent to securely link their bank accounts using Basiq Connect.

Step 2: Tag, clean and tokenise

Once the raw banking data is collected from a user’s account, transactions are separated into debits or credits

Debit

Bank fee: A fee incurred by the user from their bank e.g. ATM withdrawal fee

Payment: Payment made to a merchant

Cash withdrawal: Funds withdrawn via an ATM

Transfer: Funds transferred to an account

Loan interest: Interest charged on a loan account

Credit

Refund: Funds returned to account due to refund

Interest: Interest earned

Transfer: Funds received from an account

Loan repayment: Loan repayment credited to a loan account

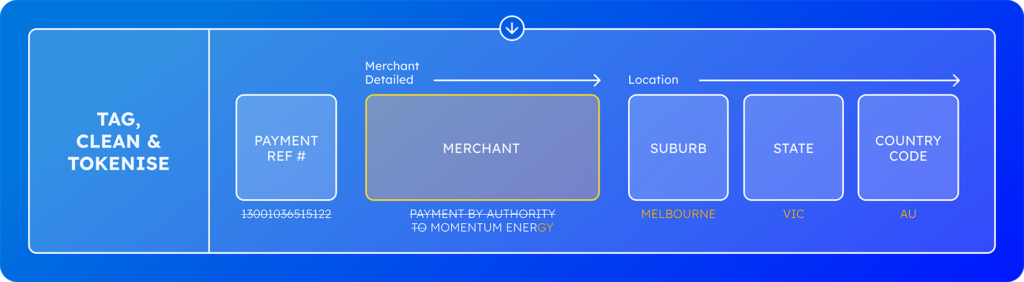

Once transactions are identified, the Basiq platform uses the transaction metadata to clean and standardise the data ready for enrichment. Below is an example of this process using a purchase from energy provider, Momentum Energy.

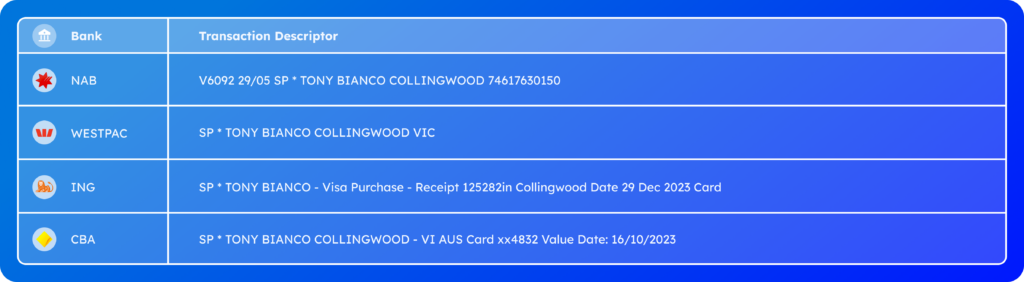

Unfortunately, there is no consistent format for transaction data across banks, so standardisation is a crucial step. For example, the image below illustrates how a transaction with footwear retailer, Tony Bianco, is returned from four different banks. To meet this challenge Basiq maintains a database of transaction description patterns by bank so enrichment can be customised depending on the institution.

Step 3: Data enrichment

Once tagged, cleaned and tokenised, the Basiq platform enriches the payment data by searching for a match in our curated merchant database which includes the identity, location and categorisation details.

When it comes to categorisation, we provide five levels of categorisation enabling greater granularity and richer insights. This includes four levels of ANZSIC categorisation (‘Division’, ‘Sub Division’, ‘Group’ and ‘Class’) and an additional ‘Sub Class’ using Basiq’s unique categorisation database.

Step 4: Machine Learning and final output

In our enrichment process, when a transaction cannot be initially categorised and enriched, our advanced machine learning model intervenes. This model leverages additional data sources, meticulously analysing transactions to fill any gaps that might remain after the initial steps.

Our goal with this approach is to ensure near-perfect accuracy in the data output. What sets it apart is its dynamic learning capability. With each transaction it processes, the ML model evolves improving its efficiency and accuracy. After the data has been enriched the process is complete and it’s ready for output – like your banking app.

Basiq Enrich transforms transaction data from banking apps into clear insights. How? By securely accessing transaction data (with permission) and applying magic—tagging, cleaning, and enrichment across each transaction using our vast merchant database and advanced machine learning.

Our goal? To make your financial data easy to understand and insightful. With Basiq Enrich, you don’t just see numbers and codes; you see your spending story unfold. It’s all about clarity, insight, and helping you make sense of where your money goes, making your banking experience not just informative but genuinely enlightening.

Want to know more?

Check out how Basiq customers are using Enrich; PokitPal and TaxTank.

This year, Australia’s Consumer Data Right (CDR) is expanding to include the non-bank lending sector. Specific Non-bank Lenders will be designated as ‘Data Holders’ within the CDR framework, requiring them to implement systems to facilitate consumers in being able to transfer their data to accredited third parties.

This builds upon the designations in the Banking and Energy sectors, where Data Holders are already operational, allowing consumers to effectively transfer their data.

November 2024 marks the first milestone for Non-bank Lenders. So what do Non-Bank Lenders need to be aware of?

Quick recap

The Consumer Data Right (CDR) is an economy wide designed to empower consumers with greater control over their data. It facilitates the secure sharing of data, currently housed in various organisations, with third parties in taking up new services. Banking was the first implementation of the CDR, commonly known as Open Banking, allowing consumers to consent to sharing their banking data with accredited third parties. For more detailed information on Open Banking, refer to Basiq’s definitive guide.

Following Banking, the Energy sector adopted the CDR and soon, Non-bank Lenders will join this initiative. Presently there are over 90 Banks and Energy providers acting as data holders. To see the complete list.

Which Non-Bank Lenders must serve as Data Holders?

Treasury has delineated two categories of providers:

Initial provider: A non-bank lender that on the commencement date has over $10 billion in loans/leases and has averaged over $10 billion for the preceding 11 months.

Large provider: A non-bank lender that on the commencement date has over $500 million but less than $10 billion in loans/leases, averaged over $500 million for the preceding 11 months, has more than 500 customers.

What types of Non-Bank Lenders does it apply to?

Some examples of organisations it applies to include:

Mortgage lenders

Consumer finance companies

Buy Now Pay Later (BNPL) providers

Leasing and hire purchase providers

Marketplace lenders

Payday lender

Peer-to-peer lenders

Salary advance providers

What are Data Holders required to do?

Data Holders must be authorised by the ACCC, fulfilling specific criteria for data security, privacy, and technical capabilities. The implementation of robust security measures, such as encryption and access controls is required to safeguard data. Privacy compliance is crucial, ensuring data use aligns with relevant privacy laws.

Data Holders are obligated to adopt technical standards to facilitate seamless data sharing across entities within the CDR ecosystem. This involves establishing a consent management framework to obtain and manage consent from consumers.

Furthermore, ongoing regulatory oversight requires Data Holders to submit regular compliance reports to the ACCC and promptly address any inquiries and issues that may arise.

What are the key dates?

What is a complex request? A “complex request” under the draft rules is a consumer data request that:

Is made on behalf of a secondary user of the consumer

Relates to a joint account or a partnership account

Is made on behalf of a non-individual CDR consumer whose authorisations are handled by a nominated representative

I’ll be required to be a Data Holder, what should I do?

While providing access to consumer and product data via APIs seem straightforward, the process of becoming a Data Holder is a complex undertaking. Beyond initial requirements, there are continuous obligations related to regulatory changes, maintenance and reporting. Based on feedback from existing Data Holders in the banking sector, it’s prudent to consider engaging a Partner with the requisite expertise, experience and knowledge.

Given the urgency and complex requirements, Non-bank Lenders falling under the scope of becoming a Data Holder should take proactive steps in initiating their CDR implementation projects. Here are our recommended actions.

Step 1: Requirements and Timing Familiarise yourself with what’s required and “go-live” deadlines

Step 2: Engage a Partner Work with a Partner that can help you navigate the complex build and maintenance requirements

Step 3: API development Start building the internal API layer to surface Users, Accounts, Transactions – needs to be done regardless of whether you engage a Partner or not.

An inside look at Open Banking performance and adoption in Australia.

Consumer Data Right

There is a lot of talk about how the Consumer Data Right (CDR) and Open Banking are performing and the majority of commentary is negative. We have found this public perception of Open Banking doesn’t align with our experience or the experience of our customers.

Basiq is one of the few data aggregators that offer both Open Banking and web scraping services. With a substantial user base across various use cases, Basiq can effectively measure the performance of Open Banking against the performance of web scraping. For the first time, we are sharing data from the Basiq platform to provide a different side of the story.

1. Open Banking has a higher growth rate than web scraping

Compounded monthly growth rate of Open Banking connections – 30%

Compounded monthly growth rate of web scraping connections – 4%

How? Data from the Basiq platform shows that Open Banking is increasingly the preferred option for data access, with its growth rate now surpassing that of web scraping. Over an 18-month period, Open Banking connections surged from 10,400 in October 2022 to 777,000 in March 2024, resulting in a compounded monthly growth rate of 30 per cent. In contrast, web scraping connectors grew by only 4 per cent during the same period.

Why? So, what’s the reason for the observed heightened growth? We attribute it to four key factors:

The Government’s introduction of new CDR access models has reduced barriers to access for businesses

An increase in the rate of significant data breaches among large corporate organisations

Open Banking is a viable option for businesses previously unable to use web scraping

Basiq enables customers to trial Open Banking before committing

2. Open Banking has a significantly higher connection success rate

Open Banking 80% Success rate – Failed connections are a result of invalid usernames/passwords, poor banking consent flow, CDR outages and potential fraudulent activities

Web Scraping 42% Success rate – The majority of failed connections are a result of invalid usernames/passwords

How? It’s a common assumption that businesses lose more customers and, therefore, revenue using Open Banking over alternatives like web scraping when connecting customer bank accounts. The logic is that the friction caused by the length of the CDR data connection process results in consumers becoming frustrated and abandoning their attempt to connect their account/s.

Data from the Basiq platform shows the opposite is true. When comparing the success rate of connecting a customer’s bank account, Open Banking has a 80 per cent success rate versus 42 per cent for web scraping.

In essence, our data shows that businesses using Open Banking end up with more customers.

Why? There are a number of events impacting the higher success rate of Open Banking versus screen scraping on the Basiq platform. These include:

Consumer enters an invalid banking username or password

Consumers don’t want to share their login or password details with a third-party

Bank implements anti-scraping measures

Planned maintenance of banking apps and online banking platforms

3. Open Banking is by far the more reliable option for ongoing connections

Failed connections after a 6 month period – 15% Web Scraping and 0.17% Open Banking

How? For businesses requiring an ongoing connection to a consumer’s account, such as budgeting or investment apps, data from the Basiq platform shows that Open Banking is highly reliable.

Connection disruption can be a major issue for businesses, increasing the risk of customer churn. Consumers must complete the connection process again to establish a new connection.

Connection data across all customers on the Basiq platform indicates that 15 per cent of all consumers using web scraping will experience a disruption to their connection after six months On the other hand, connection rates using Open Banking remain consistent with less than 0.17 per cent likelihood of disruption.

Why? Connection issues happen for a number of reasons including: