In the time it takes to buy your morning coffee, over 1,500 invisible transactions have already silently pulsed across Australia. Each one representing a meal purchased, a bill paid, or a business deal closed.

This invisible network is the heartbeat of our economy, powering everything from everyday payments at the checkout to multi-million-dollar business deals. Yet few stop to think about the sophisticated technology behind it all.

From Cash to Code: The Seismic Shift in How We Pay

Not so long ago, cash was king, cheques were more common, and digital wallets were science fiction. Today, we’re living in a payment revolution that’s transforming how business gets done.

From tap-and-go to PayIDs and digital wallets, we’ve shifted from physical to digital, from delayed to real-time, and from passive transactions to dynamic customer experiences. This isn’t just evolution—it’s a complete reinvention of how money moves.

Rethinking Payments: Your Untapped Business Advantage

For today’s businesses, payments aren’t just a necessity—they’re a strategic advantage. They’re how innovative companies:

Deepen loyalty and lifetime value.

Streamline operations and scale efficiently.

Unlock insights through data.

Deliver better customer outcomes, faster.

Businesses like yours are behind some of the most cutting-edge payment experiences used today. And who is powering those experiences? We are.

Powering $450B+ in Payments Per Year: The Cuscal Story

Today, we’re tackling the big challenges: advancing open banking, fighting sophisticated fraud, and building tomorrow’s payment infrastructure.

Outside of the major banks, we’re the largest centralised provider of payment infrastructure connectivity in the Australian payments industry. We combine:

The licensing, capital strength, and regulatory credibility of an ADI,

The agility and innovation of a fintech,

A history of disciplined disruption, and

The resilience and security of a trusted, long-term partner.

We’re transforming the future of how money moves and how Australia does business.

Cuscal’s Impact in Numbers

Since our inception, we’ve partnered with forward-thinking businesses.

Payments aren’t one-size-fits-all. We collaborate with financial institutions, fintechs, and corporates — from superannuation funds and insurers to loyalty program providers — to enhance their customer experience through payments, working with them to deliver tailored solutions to meet their unique needs.

What’s Next: The Future of Digital Payments

The payment landscape continues to evolve at breakneck speed. From blockchain to biometrics, from embedded finance to invisible payments—the next wave of innovation is already here.

By delivering faster, safer, and smarter payment experiences, we’re transforming how money moves, supporting competition, and powering Australia’s progress—one transaction at a time.

Whether you’re a bank expanding its offering, a fintech scaling new products or any enterprise- sized business that’s powered by the ability to take and make payments, we’re your partner for what’s next.

Important Information: Information in this article is current as at 27 August 2025 and is subject to change. This article is provided for general information purposes only and does not have regard to the situation or needs of any reader and must not be relied upon as advice. Before acting on this information, consider its appropriateness to your business Cuscal Limited ABN 95 087 822 455.

The way Australians pay is changing rapidly. Industry leaders discussed the technology reshaping the future of payments in Australia at Cuscal’s Curious Thinkers 2024.

From speed and security to customer experience and fraud prevention, these innovations are creating new opportunities (and challenges) for the payments landscape.

Below, we recap four key technologies discussed by panelists: Real-time Payments, Digital Wallets, Digital Identity, and Data.

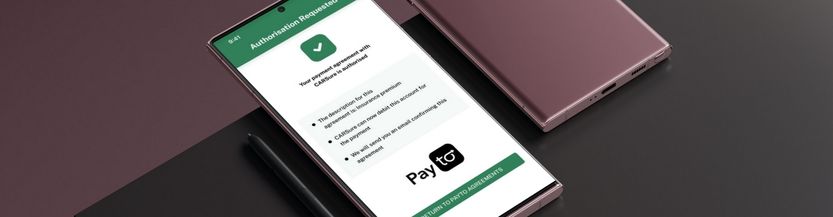

1. Real-time Payments

Real-time payments deliver instant, account-to-account transfers, boosting cash flow and eliminating settlement delays. PayTo, a feature of Australia’s New Payments Platform (NPP), offers both businesses and consumers more visibility and control over their payments while maintaining security and privacy.

Real-time payments are already proving effective across multiple industries, including retail, utilities, and government transactions, reinforcing their long-term viability and reliability.

Many Australians still default to traditional card payments, making widespread adoption slower than expected. However, panelists noted that once users try PayTo, they consistently choose it for its convenience and security.

“What we are finding is people, once they’ve used it … they really like it…We’re certainly seeing the proof that real-time account-to-account can be used in many, many situations.” Tom Rundle, Chief Product Officer, Azupay

Set-up for success

Driving adoption of real-time payments will take effort from both banks and businesses, including:

Optimising business integration: Ensuring backend systems support real-time reconciliation and reporting will help businesses transition smoothly.

Strengthening security and trust: Clear fraud prevention measures and robust consumer protections will reassure users and encourage uptake.

Raising consumer awareness: Educating customers on the benefits of real-time payments, such as speed, reliability, and security, will boost confidence and usage.

2. Digital Wallets

Digital wallets let users store payment cards on their smartphones or wearable devices to make quick, secure payments in stores, online, and in apps. Instead of using a physical card, users can tap and pay at contactless terminals or authorise transactions digitally.

Digital wallets have become a go-to payment method in Australia.

According to the RBA, Australians made over 398 million mobile wallet payments in February 2025, totaling more than $16.6 billion across both credit and debit cards.

“Consumers expect payments to be as seamless as the services they use. Digital wallets fit that expectation.” Tom Rundle, Chief Product Officer, Azupay

Set-up for success

Key enablers that will help drive adoption include:

Provider agnostic solutions: Implementing solutions that support multiple digital wallet providers.

Complementing real-time payments: Understanding when and how to offer both digital wallets and real-time payments to meet consumer expectations for convenience and security.

3. Digital Identity

Digital identity will play a key role in the future of payments in Australia. Strong verification mechanisms, such as biometric authentication and government-issued digital IDs, will be crucial in reducing fraud and enhancing transaction security.

Biometric authentication is already playing a role in how Australians access financial services, with many institutions using tools like facial recognition and fingerprint scanning to verify users.

“Digital identity [enables] two things. It’s who are you? And the other thing is what are you allowed to do? And often [not all parties to a payment] need both of those pieces.” Tom Rundle, Chief Product Officer, Azupay

Set-up for success

Key enablers that will help drive adoption include:

Building consumer trust: Consumers need confidence that their digital identity is secure, private, and protected against misuse.

Interoperability across systems: A widely accepted digital identity must integrate seamlessly across financial institutions, businesses, and government services.

4. Transaction Data

Data is transforming payment ecosystems, helping businesses enhance fraud detection, improve customer experiences, and streamline reconciliation.

More Australian businesses are harnessing structured payment data to improve reconciliation and fraud detection. AI-powered analytics are enabling financial institutions to identify suspicious transactions in real time. Additionally, data-driven decision-making is helping businesses streamline payments, cut operational costs, and enhance security.

Set-up for success

Key enablers that will help drive adoption include:

Accurate data: Ensure data accuracy to prevent processing errors.

Data standardisation: Industry-standard formats to ensure interoperability across financial networks.

Prioritise privacy and security: Strong security and privacy measures to maintain consumer trust and regulatory compliance.

Bringing it all together

The payments landscape in Australia is evolving rapidly, driven by real-time transactions, digital wallets, digital identity, and data innovation.

These technologies offer immense benefits, from faster and more secure payments to enhanced customer experiences. However, successful adoption depends on trust, seamless integration, and consumer awareness.

References Reserve Bank of Australia, ‘C1.1 Credit and Charge Cards – Original Series’ and ‘C2.1 Debit Cards – Original Series’, Reserve Bank of Australia website, statistical tables, February 2025, accessed 30 April 2025, <https://www.rba.gov.au/statistics/tables/xls/c01-1-hist.xlsx, and https://www.rba.gov.au/statistics/tables/xls/c02-1-hist.xlsx>

Important Information: Information in this article is current as at 16 May 2025 and is subject to change. This article is provided for general information purposes only and does not have regard to the situation or needs of any reader and must not be relied upon as advice. Before acting on this information, consider its appropriateness to your business Cuscal Limited ABN 95 087 822 455.

Did you know that, according to a recent report from Xero, 25% of consumers would visit another business if their preferred payment method wasn’t available? These days, payments are more than just transactions – they are make-or-break moments for customer retention.

The importance of consumer-centred payment systems was a key theme at Cuscal’s Curious Thinkers 2024 event. The panel highlighted why businesses must rethink their payment systems to align with consumer expectations and offer seamless, secure, and flexible options.

Below, we explore the shifting landscape of consumer payments, why businesses must prioritise a consumer-centred approach, and steps they can take to enhance the payment experience for their customers.

Meeting Consumer Expectations: The Changing Payments Landscape Consumers today expect more choice, transparency, and security in their payment interactions. The rise of digital wallets, real-time payments, and buy-now-pay-later (BNPL) solutions reflect this demand.

The report from Xero on how businesses and consumers are making and taking payments found that:

38% of consumers experience frustration when their preferred payment method isn’t available.

26% cite limited payment options as a reason for dissatisfaction.

25% would visit another business that accepts more payment methods.

These statistics underscore the need for businesses to offer diverse, frictionless payment options to meet evolving consumer expectations.

Beyond Transactions: Why Payment Experience Matters Have you ever abandoned a purchase because the checkout process was too complicated or a payment option you preferred wasn’t available?

Payments are an essential touchpoint in the purchase process that can influence customer satisfaction and brand perception, for better or worse. Whether it’s a quick tap at a café or a major online purchase, a seamless payment experience can foster trust and build loyalty.

The rapid growth of e-commerce has been a major driver of this shift. Take Amazon, for example. Its one-click payment system revolutionised online shopping by eliminating unnecessary steps and reducing checkout friction. Similarly, Apple Pay and Google PayTM have redefined mobile transactions by allowing secure, instant payments with minimal effort.

Consumers accustomed to fast and frictionless online payments expect the same convenience across all channels. For businesses, this means:

Delivering on speed and simplicity: Customers expect fast and intuitive transactions.

Ensuring security and privacy to build trust: Clear authentication measures without unnecessary hurdles.

Offering choice and flexibility: Multiple payment options to cater to different preferences.

Managing complexity: Ensuring smooth integration and efficient backend systems while offering more payment options.

How Businesses Can Create Better Payment Experiences Developing a consumer-centred payment system requires practical steps and thoughtful strategies. Below are recommendations from Cuscal’s Head of Payments & Innovation, Nathan Churchward, on how businesses can create a better payment experience for customers.

Know Your Customers, Meet Their Needs Businesses must assess their customers’ behaviour and preferences to tailor payment solutions. Different demographics and business types have unique payment needs, so offering a one-size-fits-all solution may not be effective. Local payment providers can offer practical solutions to help businesses choose the best payment options for their customers.

Listening to consumer feedback is also key. Understanding and addressing pain points in the payment journey helps refine strategies, improve the experience, and build trust with customers.

Make Payments Effortless and Secure A great payment experience should be both effortless and secure. Tokenisation helps by reducing the number of times customers need to enter their card details, making transactions smoother while keeping data safe. Digital wallets like Apple Pay simplify the process even further, allowing for fast, secure payments with a single tap. The best solutions remove friction and enhance security without adding extra steps.

Empower Customers Through Information Customers feel more confident when they understand how different payment options work and what benefits they offer. Businesses that educate customers on their choices (especially when encouraging a preferred payment method) build trust and transparency.

If using surcharges to guide payment decisions, pairing them with clear explanations ensures customers see the value rather than just the cost. It’s also important to reassure customers about security, especially for prepaid services or payments made in advance, by highlighting measures in place to protect their funds.

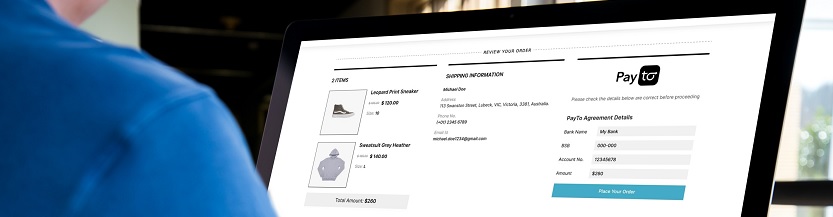

Seamless Payments, Streamlined Experience Payments should work in real-time and integrate seamlessly into business operations. Traditionally, card payments have led the way in integration and instant processing, but newer options like NPP and PayTo are catching up. The challenge has been ensuring these payment types update systems in real-time for smoother reconciliation and automation.

Businesses should seek payment providers that offer real-time payment APIs to maintain efficiency without compromise. PayTo, for example, enhances integration by eliminating the need for customers to manually enter details, allowing businesses to pass transaction data directly to the customer’s bank for easy authorisation. The right payment solutions should support automation, reduce manual processing, and improve the overall payment experience for both businesses and customers.

Prioritising Consumer Needs for Long-Term Success A truly consumer-centred payment system goes beyond technology. It requires a deep understanding of customer behaviour, a commitment to security, and an effort to educate users. Businesses that align their payment strategies with consumer needs will enhance customer satisfaction and drive loyalty and long-term growth.

References ANZ Subject Matter Experts 2024, ‘The digital payment revolution: what businesses need to know’, ANZ Insights website, article, 6 November 2024, article, accessed 17 February 2025, <https://www.anz.com/institutional/insights/articles/2024-10/the-digital-payment-revolution>

ANZ Worldline 2024, ‘Why Chief Market Officers should prioritise their payment strategy Part I’, ANZ Worldline website, article, 9 September 2022, accessed 17 February 2025, <https://anzworldline.com.au/en/home/knowledge-hub/blogs/why-chief-market-officers-should-prioritise-their-payment-strate>

Xero 2024, ‘I want to pay that way’, Xero website, report, 2024, accessed 17 February 2025, <http://www.xero.com/campaign/i-want-to-pay-that-way>

Knowledge at Wharton Staff 2017, ‘Why Amazon’s ‘1-Click’ Ordering Was a Game Changer’, Knowledge at Wharton website, podcast and article, 14 September 2017, accessed 11 March 2025, <https://knowledge.wharton.upenn.edu/podcast/knowledge-at-wharton-podcast/amazons-1-click-goes-off-patent>

Google Pay is a trademark of Google LLC. Apple Pay is a trademark of Apple Inc., registered in the U.S. and other countries.

Important Information: Information in this article is current as at 14 March 2025 and is subject to change. This article is provided for general information purposes only and does not have regard to the situation or needs of any reader and must not be relied upon as advice. Before acting on this information, consider its appropriateness to your business Cuscal Limited ABN 95 087 822 455.

A further 10 authorised deposit-taking institutions (ADIs) have been enabled by Cuscal to offer PayTo services to customers. This brings the total number of ADIs connected to PayTo through Cuscal to 26, covering 33 bank brands, with eight payment service providers certified to provide PayTo Payment Initiation services to businesses.

The latest ADIs to be certified by Cuscal as Payer Participants are: Australian Mutual Bank Limited, Community First Credit Union, Central Murray Credit Union, Geelong Bank, Goulburn Murray Credit Union, Illawarra Credit Union, Orange Credit Union, South West Slopes Credit Union, The Mac and Unity Bank Limited (Unity Bank, Reliance Bank).

Clients certified to offer PayTo will make services available to their customers over the coming days and weeks, based upon their individual service delivery strategies and rollout plans.

About Cuscal

Cuscal was the first directly connected participant to be certified by NPPA as an Initiating Participant and Payer Participant for PayTo Cuscal facilitated the creation, orchestration and initiation of the first live PayTo payment on the NPP.

Cuscal’s NPP solution is the only fully compliant solution currently in market delivering all the features of the NPP, with access to all the flows and options for NPP messaging and services, optimising the PayTo and real-time payment experience for customers.

With over 4 years NPP implementation experience, enabling 60+ implementations since 2018, Cuscal has helped more organisations to access the NPP than anyone else, including more than half of all financial institutions and all of the payment service providers that are providing payments on the Platform today.

About the New Payments Platform (NPP)

The NPP enables smarter, faster and simpler payments for businesses and consumers, including PayID and PayTo, a new digital way for merchants and businesses to initiate real-time payments from customers’ bank accounts. PayID is a registered trademark of NPP Australia Limited. Osko is a registered trademark of BPAY Pty Ltd. NPP Australia Limited and BPAY Pty Ltd are part of the of Australian Payments Plus group. For more information visit www.nppa.com.au

As more banks (and by extension millions of customers) progressively connect to the PayTo ecosystem, attention is shifting to those businesses that have been enabled as PayTo Users and the innovative use cases that they are bringing to market.

But in an ecosystem of directly and indirectly connected participants, what pathways are open to businesses to access PayTo and the New Payments Platform (NPP)? And what role do different PayTo Users play in the creation, initiation and settlement of payments?

In this article we aim to shine a light on these questions.

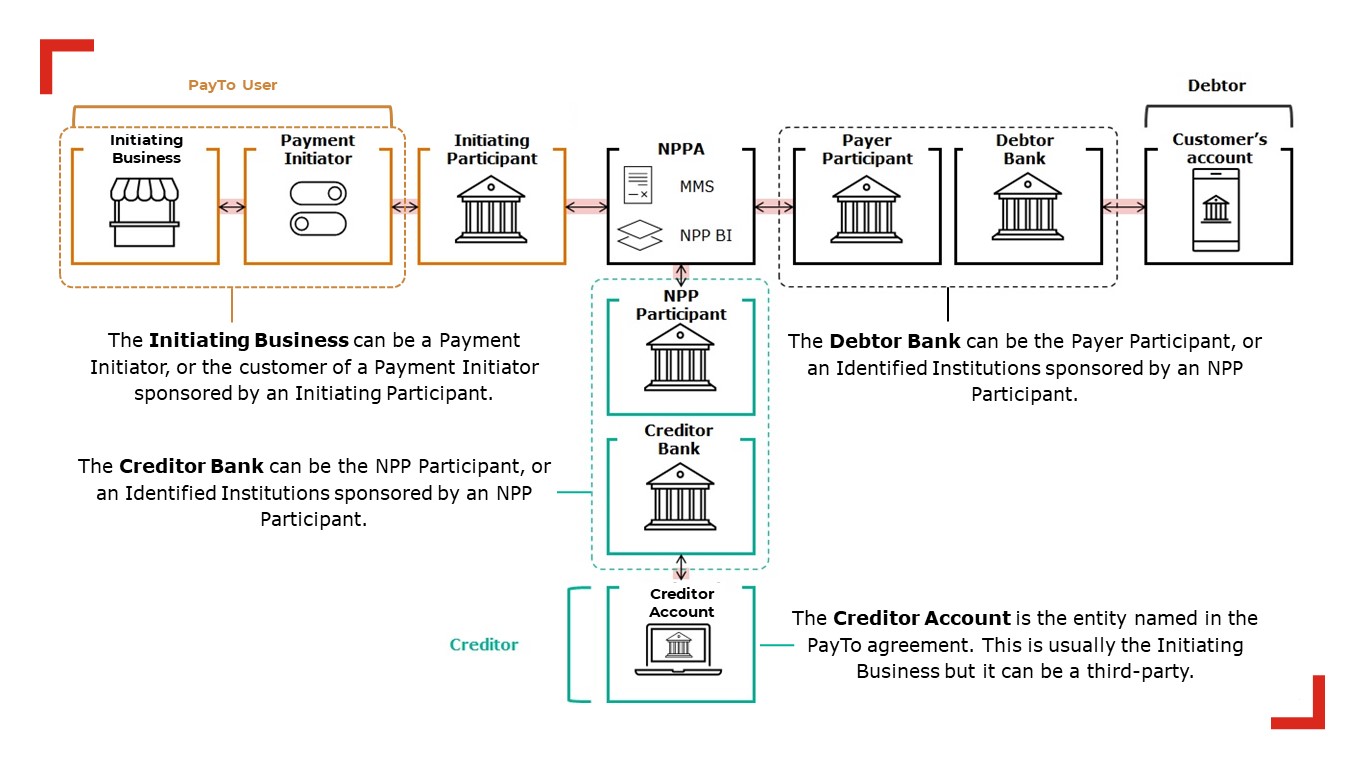

The PayTo ecosystem

PayTo is an interconnected network of participants that connects customers, business and their financial institutions, facilitating the creation of PayTo agreements and ensuring the smooth flow of payment initiation requests and settlement of funds in real-time.

Figure 1: PayTo participant ecosystem

While banks are instrumental when it comes to facilitating the authorisation and management of PayTo agreements by customers and settling funds when valid payment initiation requests are received, PayTo Users are the main players when it comes to the creation and initiation of PayTo agreements.

PayTo Users

In the PayTo ecosystem there are two types of PayTo Users: the Initiating Business and the Payment Initiator.

Initiating Businesses are responsible for entering into PayTo agreements with the debtor customer, defining the PayTo agreement terms that will be registered in NPPA’s Mandate Management Service (MMS) and authorised by the customer through their digital banking channel, and initiating requests for payment in accordance with the agreed terms.

Payment Initiators are responsible for the exchange of PayTo agreement creation and payment messages to/from the Initiating Businesses with the wider PayTo ecosystem, via APIs provided by the sponsoring Initiating Participant.

Initiating Participants

To access PayTo as a Payment Initiator, businesses need to be sponsored by an Initiating Participant: either a Connected Institution or an NPP Participant or Identified Institution that has been certified as a Payment Initiator.

Connected Institutions are only able to use the non-value messaging capabilities of the NPP Basic Infrastructure to create a PayTo mandate and send a Payment Initiation Request. They cannot clear or settle payments or issue or manage PayIDs.

NPP Participants and Identified Institutions that have been certified as a Payment Initiator have access to all flows and options for NPP messaging and services, delivering end-to-end payment initiation, PayID issuance and management, and clearing and settlement services through a single provider.

Clearing and settlement services can only be provided by an NPP Participant licensed by APRA as an Authorised Deposit-Taking Institution (ADI)This helps to keep payments safe because as ADIs, NPP Participants meet the prudential requirements set by the Australian Prudential Regulation Authority (APRA) to operate in the regulated payments environment and have access to RBA settlement facilities. Like in other payment systems, the NPP Participant can sponsor other organisations to provide clearing and settlement services on their behalf, and in the NPP, these entities are referred to as Identified Institutions.

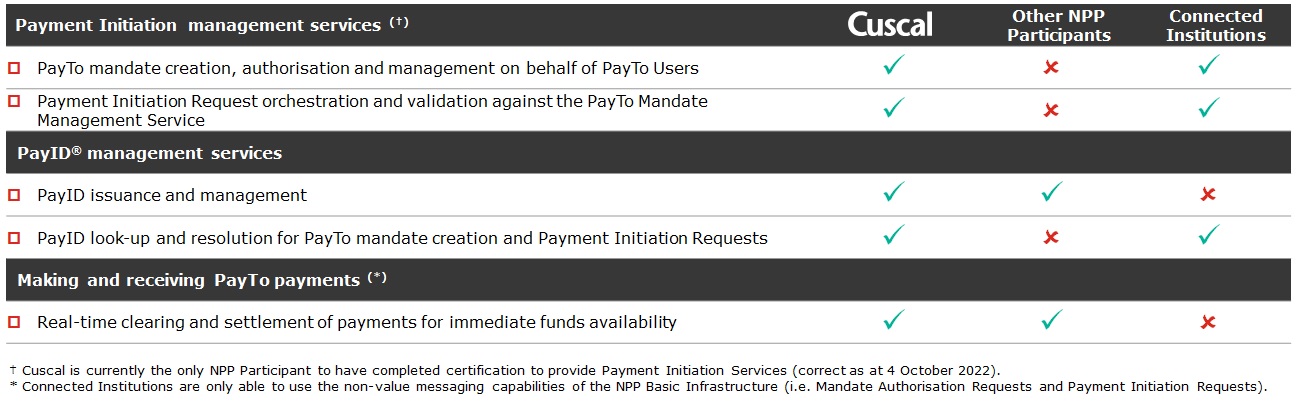

Figure 2: Cuscal NPP services compared to other directly connected participants

Why Cuscal

As the first directly connected participant to be certified by NPP Australia (NPPA) as an Initiating Participant and Payer Participant, Cuscal plays a unique role in the PayTo ecosystem.

As a certified Initiating Participant, Cuscal connects high volume and high growth businesses, payment service providers, platforms and payment facilitators to the NPP as Identified Institutions and Payment Initiators, providing access to all the features of the NPP under a sponsorship arrangement. Businesses can connect to PayTo as an Initiating Business through a Payment Initiator under a proprietary commercial arrangement with a Payment Initiator that has been connected to the Platform by Cuscal.

As a certified Payer Participant, Cuscal provides banks, credit unions and mutual banks with access to the services required to receive, process and manage PayTo agreements and payment initiation requests, as well as the infrastructure required to clear and settle payments.

At Cuscal we have been helping our clients to access Australia’s payment systems with innovative solutions for over 50 years. As the market leader in providing NPP services, with over 4 years NPP experience enabling 60+ implementations since 2018, we’ve helped more organisations to access the NPP than anyone else, including more than half of all financial institutions and all of the payment service providers that are providing payments on the Platform today.

With the launch of PayTo, Cuscal has the scale, expertise, trusted industry position and comprehensive real-time account-based payment and payment initiation solutions required by Payment Initiators.

To find out more about connecting to PayTo as a Payment Initiator and how you can provide PayTo services to your business customers, contact Cuscal.

Cuscal Limited today announced that 12 clients have been approved to offer PayTo services to consumers and businesses, expanding the number of Identified Institutions certified as Payer Participants and Initiating Participants.

Payer Participants enabled by Cuscal The following clients have been certified by Cuscal as Payer Participants: Bank Australia, BankWAW, Broken Hill Community Credit Union, Credit Union SA, Defence Bank, First Option Bank, Horizon Bank, Laboratories Credit Union, Police & Nurses Limited (P&N Bank, bcu) and RACQ Bank, joining Bendigo and Adelaide Bank, Great Southern Bank and People’s Choice that received certification from NPP Australia Limited (NPPA) in September.

Each of these organisations will now make PayTo available within their digital banking channels.

Initiating Participants enabled by Cuscal Global Payments (eway, ezidebit) and Merchant Warrior have been certified by Cuscal to provide PayTo initiation services to businesses, joining Azupay, Ezypay, Monoova, Paypa Plane and Zai as Initiating Participants.

Commenting on the growing number of participants connected to PayTo through Cuscal, Nathan Churchward, Head of Product, Emerging Services said:

Successful completion of the certification process by such a diverse group of Identified Institutions at the same time is testament to the value of partnership and collaboration when it comes to advancing complex industry programs like PayTo. With over 14 bank and credit union brands and 8 payments service providers now connected to the PayTo ecosystem through Cuscal, we are cementing our position as the undisputed leader in the provision of enterprise NPP services.

About Cuscal Cuscal was the first participant to be certified by NPPA as both an Initiating Participant and Payer Participant for PayTo. Cuscal facilitated the creation, orchestration, and initiation of the first live PayTo payment on the NPP.

Cuscal’s NPP solution is the only fully compliant solution currently in market delivering all the features of the NPP, with access to all the flows and options for NPP messaging and services, optimising the PayTo and real-time payment experience for customers.

With over 4 years NPP implementation experience, enabling 60+ implementations since 2018, Cuscal has helped more organisations to access the NPP than anyone else, including more than half of all financial institutions and all the payment service providers that are providing their customers with payments on the Platform today.

About the New Payments Platform (NPP) The NPP enables smarter, faster and simpler payments for businesses and consumers, including PayID and PayTo, a new digital way for merchants and businesses to initiate real-time payments from customers’ bank accounts. PayID is a registered trademark of NPP Australia Limited. Osko is a registered trademark of BPAY Pty Ltd. NPP Australia Limited and BPAY Pty Ltd are part of the of Australian Payments Plus group. For more information visit www.nppa.com.au

The rollout of PayTo capabilities to online banking channels, with Great Southern Bank leading the way, has sharpened focus on ‘how’ and ‘why’ businesses should become initiating participants to enable real-time and future dated payments from their customers’ bank accounts.

In this post we look at how PayTo can help initiating businesses thrive in a digital economy with fast, reliable and secure payments that keeps money moving 24/7.

The case for PayTo

As an enabler of real-time digital commerce, PayTo supports a broad range of use cases, delivering tangible benefits for the initiating business, including:

Explicit customer authorisation before any payments can be processed from bank accounts, addressing one of its biggest payment challenges facing businesses today; the requirement for consent via Strong Customer Authentication to reduce the risk of fraud, unauthorised payments and chargebacks.

Message response times that are delivered in seconds, confirming that valid account details have been provided, that payment has been authorised by the account owner, and that funds are available at time of payment, improving the certainty of successful payment outcomes for the initiating business.

The real-time settlement of funds at time of payment to improve cashflow availability for reinvestment in the business.

From an operational perspective the data-rich ISO messaging capabilities of the NPP enables more precise transaction data to be included within payment initiation and clearing and settlement messages. Data that more accurately describes the terms of the payer customer’s authorisation, including; payment type (recurring, one-off or ad hoc), any ultimate creditor’s name, descriptions and creditor’s reference(s), all support the easier reconciliation of payments. This also provides richer data insights that businesses can use to tailor their products and services to optimise customer experience.

The format of PayTo mandates and the data that can be included offers significant benefits in terms of data quality and visibility, compared to the relatively opaque nature of direct debit arrangements established under the BECS Direct Entry system, particularly if the payment is being facilitated via an intermediary.

Taken individually, each feature of a PayTo mandate improves an aspect of the payment experience. Taken together they can help lower the total cost of payment acceptance for the initiating business.

How to connect to PayTo as a Payment Initiator or Initiating Business

Payment service providers, platforms and payment facilitators that process payments on behalf of other businesses, as well as high volume and high growth businesses that process their own payments, can connect to PayTo as a Payment Initiator through Cuscal, the market leader in NPP. Benefits include:

Only one access point required to initiate payments with all financial institutions connected to the NPP.

APIs supporting seamless integration and straight-through processes.

Structured data capabilities to support automated reconciliation.

Centralised, secure storage of PayTo mandates reducing the reputational risk from payments data breeches.

Real-time account validation when a mandate is created.

PayTo authorisation by the account owner through secure bank channels.

Real-time funds verification at the time of payment.

Real-time notification of payment outcomes.

Faster settlement compared to other payment methods.

Integration of notifications into customer service and support processes when a PayTo mandate is paused, changed or cancelled.

With PayTo now live in banking channels are you ready to transform your business with PayTo? To find out more about connecting to PayTo as a Payment Initiator, contact Cuscal.

Leveraging the data-rich capabilities of the New Payments Platform (NPP), PayTo delivers insight rich, convenient and trusted payment arrangements for merchants, businesses and government agencies, while consumers benefit from having more control and visibility over payments set up from their bank account.

As PayTo commences rolling out to payments service providers and financial institutions over the coming months it is set to modernise the way bank accounts are used for payments, underpinning innovation for years to come in how we pay and get paid. Representing a step change in account-to-account payments, PayTo is much more than just a real-time alternative to direct debit. PayTo streamlines in-app payments, card-on-file arrangements, funding for digital wallet and buy-now-pay-later services and recurring e-commerce payments.

Accessing PayTo

Payments service providers, fintech and enterprise interested in initiating payments themselves, or on behalf of another third-party, can connect to PayTo via Cuscal. As a market leader in the NPP, Cuscal has the scale, experience, technical knowledge and trusted industry position to help payments service providers, fintech and enterprise compete and succeed with PayTo.

Merchants, businesses and government agencies interested in offering PayTo as a payment option for customers can now access PayTo services through a payments service provider connected to the Platform. Some of the leading innovators on the Platform today have integrated with PayTo through Cuscal’s Payment Initiator Service, building on top of our service to bring to life new innovative PayTo propositions.

Azupay

Established in 2019, Azupay is an Australian fintech focused on payment solutions using the New Payments Platform (NPP) technology, specialising in real-time payments using NPP and PayID to help government, business and consumers pay and get paid faster. www.azupay.com.au

Eway

Eway is a global omnichannel payment provider, processing ecommerce payments for merchants through a secure and reliable online payment gateway that makes it easy to accept payments from anyone, anywhere, from any device. www.eway.com.au

Ezidebit

Ezidebit is one of Australia’s leading online payment solution provider specialising in securely collecting Direct Debit, BPAY, EFTPOS and real-time payments for businesses. www.ezidebit.com

Ezypay

As one of Australia’s leading subscription payment providers, Ezypay offers a suite of easy-to-use subscription management services through their cloud-based payment platform, making it easy for businesses to settle payments and generate revenue through a standalone web interface, or directly integrated into a range of industry specific partner platforms. www.ezypay.com.au

GoCardless

GoCardless is a global leader in account-to-account payments, helping businesses accelerate the collection and management of recurring and one-off payments directly from customers’ bank accounts. With a global payments network and technology platform, GoCardless processes US$30 billion of payments for 65,000 businesses across more than 30 countries every year. www.gocardless.com

Monoova

Monoova supports scaling businesses with large, and often complex, ongoing transaction flows to fully automate how they receive, manage, pay and request payment of funds through one simple API integration. Its proprietary platform allows businesses to access a variety of payments functions, comprehensive reconciliation and reporting options and entirely customised real-time data. www.monoova.com

Paypa Plane

Australian fintech Paypa Plane helps banks and PSPs rapidly evolve product offerings without changing existing infrastructure through it’s simple ‘plug-in’ over the top bank-grade platform and white-label solutions, helping banks and PSPs create closer, more valuable and long term relationships with their small and medium business customers. www.paypaplane.com

Zai

Zai helps mid-market and enterprise-level business customers in the world of integrated financial services automate complex payment workflows and reconcile pay ins and payouts, helping them operate more effectively by saving time and money so they can scale and grow. www.hellozai.com

Cuscal was one of the founding financial institutions that established the New Payments Platform (NPP), Australia’s real-time payment system, and enabled over 60% of the financial institutions that were live on Day 1.

Since that time, Cuscal has strengthened its position as the market leader in NPP services, building a strong foundation of clients, industry relationships, expertise and scale over the last five years.

Cuscal currently:

Provides access to the NPP for over half of all financial institutions and payment service providers on the platform that offer real time payments to their customers

Processes 18% of payments made and 19% of payments received on the NPP

Cuscal is working closely with a large group of banks, payments service providers and software providers to support the ramp up of PayTo over the next few months. Cuscal’s PayTo development and implementation project has included many financial institutions and PSPs who wish to drive payment innovation and improved customer experiences using PayTo.

Cuscal is able to support a wide range of capabilities. We are about enabling competition. We provide services that let our clients innovate and develop their businesses. It has been a rewarding process to work with our financial institution and payment service provider clients to enable them to be the early adopters for PayTo.

The first group of financial institutions and payment service providers integrating with PayTo through Cuscal will go-live between July and September, followed by fast followers between October and December. The gradual ramp up of PayTo is expected to be completed in 2023 with full industry adoption.

Cuscal’s NPP infrastructure, scalable solution design and modular API services have made it possible for both existing and new clients who are focused on investing in innovation for their customers, to extend their NPP services to access PayTo, ensuring they are at the forefront of future payments innovation across subscription and bill payments, ecommerce and in app transactions, embedded finance and account funding, and the bulk disbursement of funds.

Cuscal has also partnered with software providers to ensure that Cuscal’s NPP Payments and PayTo services are integrated seamlessly into all clients’ digital channels to deliver an optimum customer experience.

Cuscal’s expertise and scale has also attracted clients who are nimble, innovative and focused to take advantage of one seamless onboarding to enable them to be first to market with Cuscal’s NPP Payments and PayTo services.

James Foster, Chief Executive Officer, Ezypay, commented:

We chose to partner with Cuscal as we knew they could deliver on our requirements to be live with PayTo on Day 1. We are a leading subscription payments fintech and it’s comforting to know that Cuscal’s vision for the future of payments in Australia is strongly aligned with ours.

NPP’s PayTo will be a new, digital way for merchants and businesses to initiate real-time payments from their customers’ bank accounts while allowing customers to see and control all recurring payments through their account. With the introduction of PayTo from mid-2022 all financial institutions that offer customer-initiated real-time payments will need to make significant changes to their back-office processes and technology in order to support receiving and actioning PayTo messages and payment initiation requests.

Ben Vivoda, Head of Client Services and Nathan Churchward, Head of Product Emerging Services, from Cuscal met virtually with members of the SAM Network to discuss this next phase of the NPP and the opportunities that PayTo will create.

Figure 2: Cuscal NPP services compared to other directly connected participants

Figure 2: Cuscal NPP services compared to other directly connected participants