Times have changed. It’s now normal for consumers to buy their groceries, clothes and travel, read news, socialise and research major purchases via their phones. Even essential government services like Centrelink and Medicare are encouraging their customers to use their digital channels rather than face-to-face contact. Financial institutions must also provide opportunities for customers to complete more of their banking via digital channels.

A recent McKinsey and Company report[i] shows that customers across Asia – including Australia – have made a clear shift to digital banking in line with smartphone usage.

Mobile banking is now the preferred option for standard banking transactions such as checking account balances and paying bills. The report highlighted that deep digital engagement with customers can generate considerable value for banks: digitally active customers are stickier – they purchase 1.6 products per year, compared to 0.5 on average for non-digital customers; and active digital customers also own 1.5 times more banking products than their non-digital peers.

Enabling digital engagement at the front-end, where consumers interact with their bank’s services, is a crucial part of developing digitally active customers. Banking apps that are easy to navigate and rich in features provide a myriad of benefits to customers – and ultimately to financial institutions too.

Driving engagement with card and PIN controls

You can improve the richness of your existing digital channels, like banking apps, by introducing new functionality. This can increase your customers’ ability to self-service, encouraging ongoing, regular use of your banking services and improving their loyalty to your brand.

For a customer managing their banking, the ability to manage their card PIN through their banking app – rather than having to make time to visit the branch – is a perfect example of how a banking app which is rich in functionality can better meet customers’ needs. Indeed, for a customer with a crisis out of hours where they need money and have forgotten their PIN, the ability to take control and solve the problem themselves, using their banking app, can be an instant stress reliever.

Implementing enhanced card controls within a banking app is another great way to engage customers by giving them the tangible benefit of real-time management of their cards. Allowing customers to turn certain transaction types on and off with a swipe of their finger, or activate limit-based transaction blocks, creates both financially savvy and digitally engaged customers.

Enabling or disabling contactless payments, switching online or card not present transactions on and off, activating or de-activating ATM transactions (for domestic or overseas transactions) are all examples of everyday interactions banks can create for customers within their banking app. Some customers are asking for further controls, such as setting blocks on merchant categories and being notified when transactions are approved or declined.

Benefits for financial institutions

There is benefit for banks in moving functionality into online or digital channels.

Empowering customers to self-serve helps to lower cost-to-service metrics and enables customer service staff to focus on other priorities and higher value transactions.

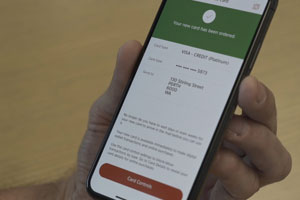

Using a banking app as a delivery channel can help solve pain points for both customers and financial institutions. A good example of this is the emergence of virtual card capabilities, to support instant card issuance. This technology allows a financial institution to digitally issue a card to a customer via their banking app or internet banking platform. The customer receives their digital card almost immediately after the order is processed. They can set their PIN, activate the card and use it online straight away. The card can also be provisioned to a digital wallet such as Apple Pay, Google Pay, Samsung Pay or a wearable like Fitbit Pay or Garmin Pay, and be used straight away, anywhere contactless transactions are accepted. No more waiting for several days for the plastic card to arrive before you can start spending.

Instant card issuance is a win for both institutions and customers. The financial institution earns transaction revenue sooner than with the traditional card and PIN ordering process, and saves money because plastic cards and PINs don’t need to be created or sent to customers. Cardholders benefit as they no longer need to worry about their PIN falling into the wrong hands, or wait for their card to arrive before spending in stores or online.

Your best friend when disaster strikes

Digitally issued cards also go a long way to solving the lost card problem – because there isn’t a card to lose! And a virtual card on the phone, even if it is lost, is protected by the phone’s security.

And finally, if a customer loses their physical card – especially if they are travelling – being able to issue a virtual card instantly means that the customer isn’t stranded. It’s conceivable that they could lose their plastic card at breakfast on their last day, login to the app, cancel the old card and set up a new virtual card on their phone in time to check out of their hotel and go to the airport.

Without instant card issuance, the customer could have been stranded for days, or even a week.

At Cuscal, we are collaborating with our clients to help them offer engaging and innovative banking experiences to their customers. Our current suite of products is designed to promote efficiencies in banking operations and create self-service opportunities for cardholders. Our API suite includes enhanced card control APIs, PIN management APIs (including PIN change and PIN set functionality) and a virtual card set to facilitate instant card issuance.

These are dynamic times for financial institutions and we are excited to be assisting our clients to develop solutions that support a more digital way of banking.

By Lauren McCormack, Head of EFT, Acquiring and Digital

[i] Sonia Barquin, Viniyak, HV, Duhita Shrikhande, Asia’s digital banking race: giving customers what they want, McKinsey & Company, Global Banking Practice, April 2018