I recently returned from a study tour to the world’s largest fintech event, the Money 20/20 conference in Copenhagen. We also met with major banks in Poland, which has one of the fastest growing economies in Europe and a payments industry with similar challenges to those in Australia. I was joined on the trip by my colleagues Bianca Bates, Head of Client Services and Rob Bell, General Manager, Product & Service.

Here are my reflections on how financial institutions are responding to the changing payments sector in Europe.

The dual threats to European payments: global tech giants & fintechs

Traditional banks are facing significant challenges in Europe. On the one side, global tech giants such as Alibaba, Amazon, Apple, Google and Facebook are capitalising on their significant scale and consumer trust to grow their share of the finance value chain, particularly the relationship with the customer. On the other side, small fintechs are able to innovate much more quickly than banks.

The threat posed by global tech giants and small fintechs is growing with Payments Service Directive 2 (PSD2) coming into force in 2018. PSD2 mandates for financial institutions to make cardholder data accessible to third-parties. It will mean that the end-user will own their transaction data and be able to choose who sees and uses the information. This open data directive will promote competition and innovation in the payments sector, meaning it will be much easier for tech giants and fintechs to take market share from traditional banks.

The threats to large financial institutions presented by PSD2 in Europe could soon be seen in Australia, with the Australian Productivity Commission’s recent report on data availability and use favouring open data, and the resulting transformation of our financial system and economy. This makes the insights on how European banks are responding to the directive particularly pertinent to Australian banks.

European financial institutions are responding to these threats in four main ways:

1. Collaborate to fend off competition

We saw examples of strong collaboration in both Poland and Denmark in response to these emerging competitors.

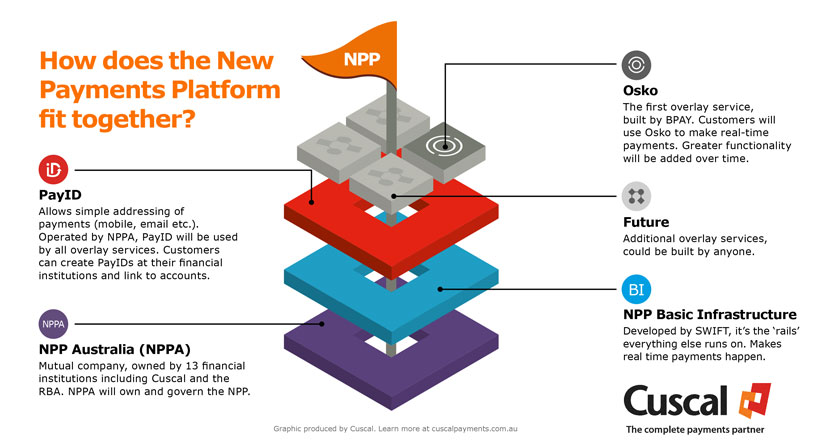

Danish banks, through aggregator company Nets, launched a very successful real time payments system, RealTime24/7, in the domestic market in 2014. This is the equivalent of the New Payments Platform (NPP), launching in Australia later this year.

The faster payments platform implementation in Denmark saw strong collaboration across the industry – they did not compete on their front end applications or by customising the solution for each bank. All Danish banks share the real time payments app, MobilePay, which uses its faster payments platform. The system has 4 million users (out of a population of 5.5 million), and 7 out of 8 transactions are originated by the app, largely replacing cash transactions.

Danish banks have also enabled Bluetooth at POS terminals so customers can use their mobile to pay via the faster payments platform.

Collaborating to make the most of the faster payments platform and making its use easy for consumers has helped financial institutions in Denmark to retain market share.

2. Invest in innovation hubs outside of financial institutions

Many banks have responded to the threat posed by fintech innovation by creating their own ‘incubators’, but generally they are still unable to move as quickly as nimbler, smaller fintech companies. Many speakers at Money 20/20 believe that partnering with smaller fintechs, or buying them, is a more successful strategy for innovation than trying to replicate them within a financial institution.

We saw a different approach in Poland, where a group of Visa clients from across Europe established an innovation hub with €20m budget in order to drive innovation across the payments ecosystem.

3. Innovate fast to compete directly with tech giants

PKO Bank Polski, the market-leading bank in Poland, developed an app to allow POS and P2P payments. The app lets customers generate a code for paying at POS terminals, or withdrawing cash at ATMs (similar to cardless cash in Australia). They sold the app into a joint venture with some of their competitors to get 60-70% of the market share. This is an example of a financial institution seizing an opportunity for technology to disrupt the payments market before the entrance of international competitors.

4. Focus on customer experience

A major theme emerging from our meetings and the Money 20/20 conference was the importance of the customer journey experience. This is an area that the global tech giants excel at, and something that financial institutions are increasingly concentrating on.

We heard that removing friction from the customer experience was critical for engagement. The slightest friction in a transaction can result in it being abandoned. Tech giants like Apple and Alibaba are very good at reducing friction for consumers, and banks are playing catch up to stay competitive.

Overall it was a valuable trip to learn about the challenges facing European financial institutions and the varying success of strategies to respond to those challenges, with many learnings for the Australian payments industry.

By Lauren McCormack, Senior Manager, EFT & rediATMs