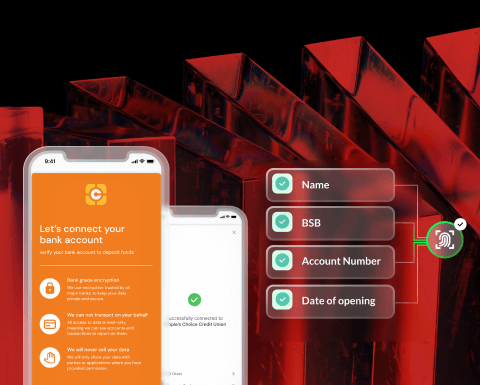

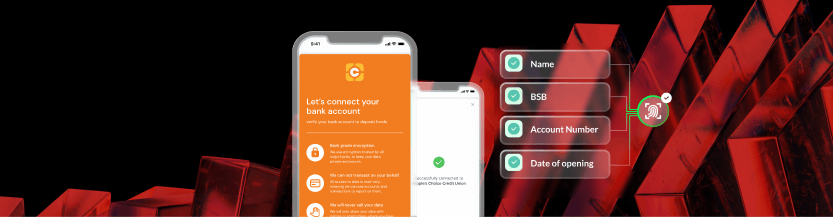

Fraud and scams are rising, and they’re shaking customer confidence at its foundation. Every scam attempt is a moment of vulnerability for your customers. Based on Cuscal’s Quarterly Insights research with over 2,000 Australian consumers, 57% of respondents face scam attempts weekly, and almost one in three has been impacted. Behind every statistic is a person who wants to feel safe when they bank with you.

Trust Starts with Security

Security and trust go hand in hand. Customers expect robust protection, but they also value reassurance that you genuinely have their best interests at heart. Trust drives loyalty, and loyalty translates into retention and revenue. When customers feel both protected and valued, they stay.

Security as a Strategic Advantage

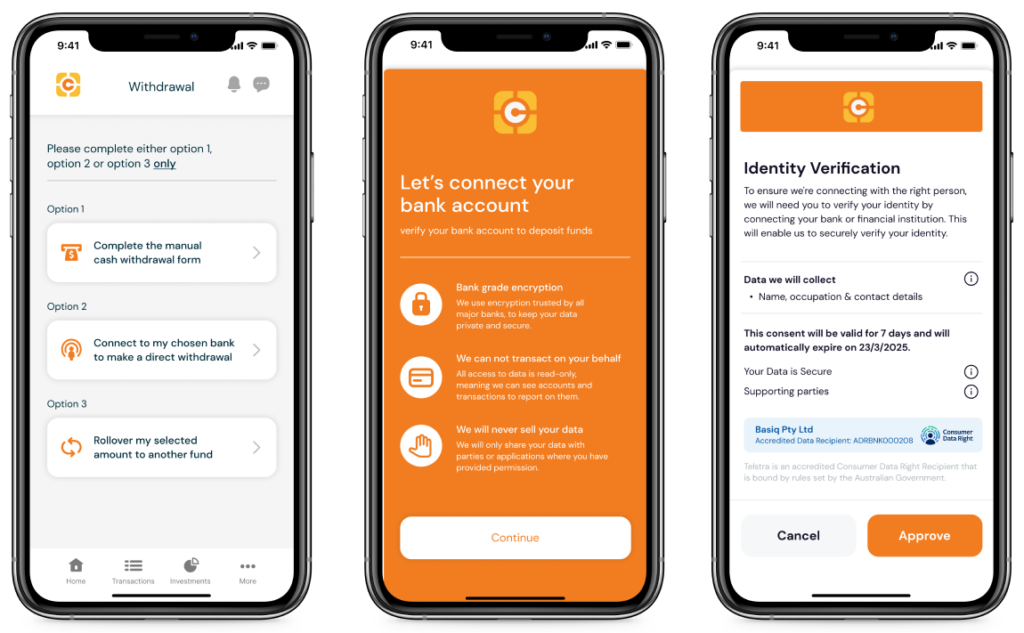

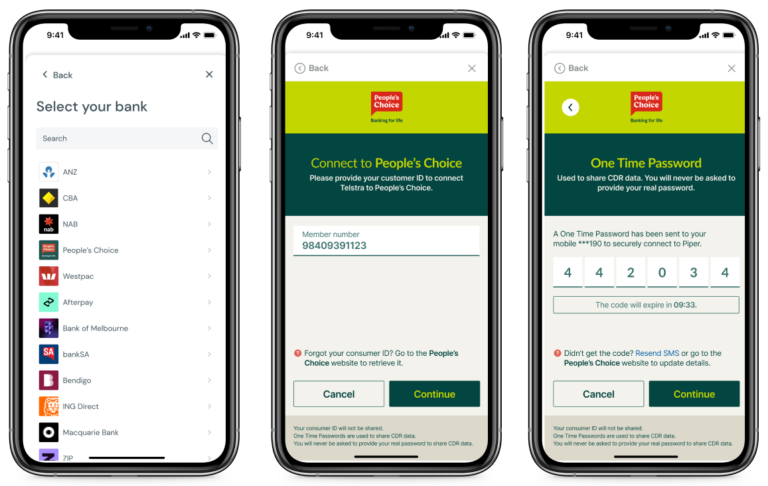

As confirmed by our latest survey and qualitative community study, communication plays a critical role in building that trust. Nine out of ten respondents believe their financial institution should do more to protect them, and 86% want regular updates on new scam tactics. Security has evolved beyond compliance. Today, it’s a competitive advantage and a core promise that influences why customers choose you and stay with you.

Our insights point to five essentials:

- Visible, robust protection such as multi-factor authentication and real-time alerts.

- Proactive education through scam alerts via SMS, in-app notifications, and targeted campaigns.

- Empathetic support with fast, human responses when things go wrong.

- Transparent communication that keeps customers informed every step of the way.

- Customisable security options that give customers control and confidence.

Strengthening Your Fraud Defences

Fraud prevention goes beyond protection. You’re earning trust when it matters most, and that trust becomes the foundation of lasting customer relationships. Cuscal can help you deliver on that promise with advanced fraud monitoring for cards and real-time payments, AI-driven detection tools, and comprehensive financial crime solutions that keep you ahead of emerging threats.

Stay Ahead of Fraud Threats

Explore the full report for practical strategies, real-world case studies, and industry benchmarks that can help you stay ahead of emerging threats.

Get the White Paper

[gpsa required_form_ids=”8″ requires_access_message=”Complete the below form and we will email you the PDF.” fallback_behavior=”show_message” access_duration_type=”custom” access_duration_value=”365″

access_duration_unit=”days” content_loading_message=”Loading…”]Thanks for requesting this White Paper, you will have it in your inbox in the next 5 mins.[/gpsa]

Important Information: Information in this web copy and White Paper are current as at 04 March 2026 and is subject to change. This information is provided for general information purposes only and not for the purpose of providing legal, financial or investment advice. The information contained in the web copy and White Paper does not constitute an offer, a solicitation of an offer or to enter a legally binding contract. The web copy and White Paper contains material provided by third parties. While such material is published with the necessary permission, Cuscal does not accept any responsibility for the accuracy or completeness of any such material. Although Cuscal has made every effort to ensure the information is free from error, Cuscal does not warrant the accuracy, adequacy or completeness of the information. Except where contrary to law, Cuscal intends by this notice to exclude liability for the information. This web copy and White Paper is not to be distributed to any other party without Cuscal’s prior written consent. Cuscal Limited ABN 95 087 822 455.