Sydney, 6 February 2018: eftpos, Australia’s own debit payments network, today announced eftpos-only cardholders from six Cuscal sponsored financial institutions can now use Apple Pay, which is transforming mobile payments with an easy, secure and private way to pay that’s fast and convenient.

eftpos Acting CEO, Mr Paul Jennings, said that leading independent payments company Cuscal has worked with eftpos to enable six financial institutions to launch eftpos for Apple Pay today, offering their eftpos cardholders the choice of using Apple Pay with eftpos.

The Cuscal sponsored financial institutions include CUA, FCCS, Nexus Mutual, People’s Choice Credit Union, SCU More Generous Banking, and Woolworths Employees’ Credit Union.

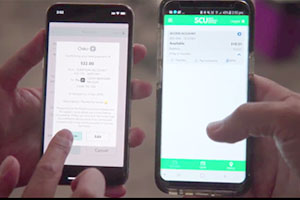

Mr Jennings said Apple Pay with eftpos will provide eligible eftpos cardholders with the ability to make eftpos purchases on their iPhone or Apple Watch using their own money, processed in real time.

Security and privacy is at the core of Apple Pay. When you use an eftpos card from participating financial institutions with Apple Pay, the actual card numbers are not stored on the device, nor on Apple servers. Instead, a unique Device Account Number is assigned, encrypted and securely stored in the Secure Element on your device. Each transaction is authorised with a one-time unique dynamic security code.

“Today marks another significant milestone for eftpos as we enable more consumers with an iPhone or Apple Watch to choose eftpos to make a transaction from their CHQ or SAV account,” Mr Jennings said. “As Australia’s most used debit card network, we are thrilled to provide consumers from these participating financial institutions with more payment choice, with added benefits of enhanced security and convenience.”

In stores, Apple Pay works with iPhone SE, iPhone 6 and later, and Apple Watch. To set up Apple Pay, cardholders from participating banks and credit unions simply need to open the Apple Wallet app in iOS 11 and follow the prompts.

Cuscal’s General Manager Product and Service, Robert Bell said: “Tens of thousands of eftpos cardholders can now pay with their iPhones, providing greater choice for our clients’ customers. We provide leading digital payment solutions to our clients, helping them to compete on a more level playing field with the big banks.”

For more information on Apple Pay, visit: http://www.apple.com/au/apple-pay/

This press release was originally published by eftpos.

About eftpos

eftpos is the most widely used debit card system in Australia, accounting about 2 billion CHQ and SAV transactions in 2017 worth more than $130 billion. For more information on eftpos, please visit: www.eftposaustralia.com.au

About Cuscal

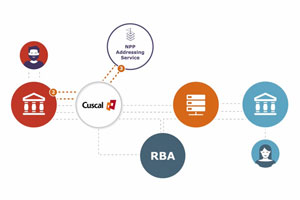

Cuscal is Australia’s leading independent provider of payment solutions including card and acquiring products, mobile payments, NPP, fraud prevention, EFT switching and direct entry. We process 14% of Australia’s EFT transactions, have over 7.5 million cards under management and switch and acquire for around 35% of Australia’s ATMs. W: www.cuscal.com/ L: www.linkedin.com/company/cuscal

Media inquiries:

Warwick Ponder, eftpos

0408 410 593

WPonder@eftposaustralia.com.au

Jo Savill, Cuscal

0447555018

jsavill@cuscal.com.au

Cuscal has appointed Bianca Bates to the role of Chief Client Officer, as part of Cuscal’s Leadership Team. This role replaces the role of General Manager, Product & Service, which Bianca has been acting in since February 2018.

Cuscal has appointed Bianca Bates to the role of Chief Client Officer, as part of Cuscal’s Leadership Team. This role replaces the role of General Manager, Product & Service, which Bianca has been acting in since February 2018.