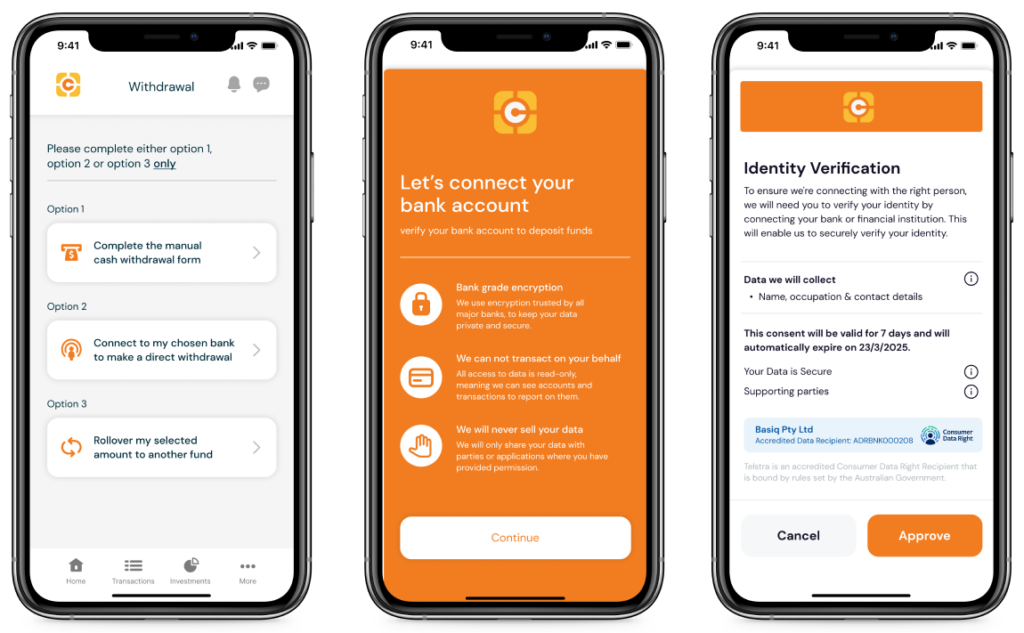

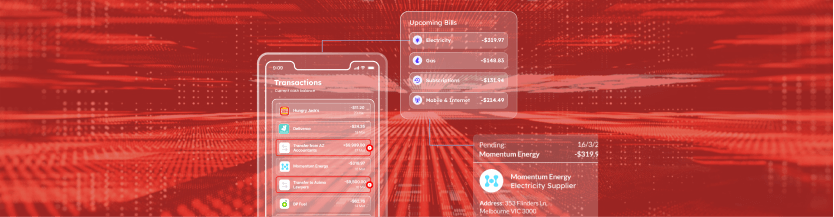

In today’s fast-paced financial world, lenders and brokers face the constant challenge of providing quick and accurate financial assessments to banks to process loans. Although core lending decisions often rely on comprehensive Consumer Affordability Reports, banks still require a traditional bank statement as part of the supporting documentation. Basiq’s new Bank Statements product is a tool that complements our existing insights affordability solution, offering a streamlined way for financial assessments to be shared with banks.

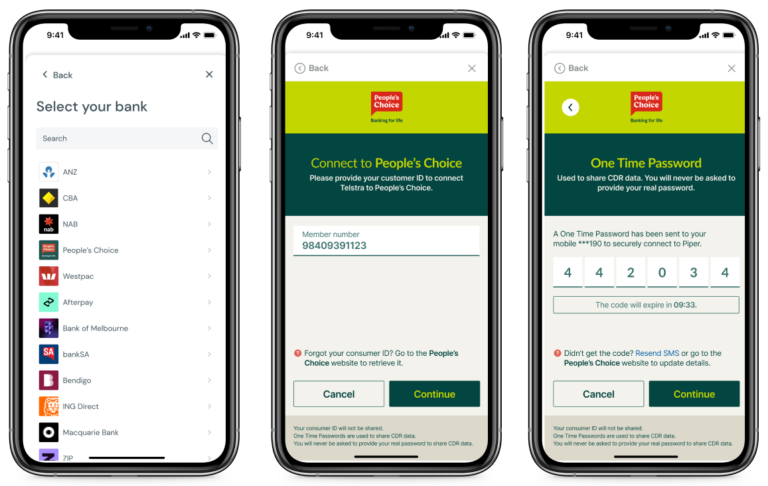

Traditionally, obtaining these statements involves a cumbersome, manual process that can delay decision-making and frustrate both lenders and customers alike. This need for speed and precision in financial assessments highlights a critical gap in the current tools available to lenders.

Understanding the pain points

- Inefficiency: Traditional processes for retrieving and verifying bank statements are notoriously slow and can lead to significant delays in loan approval.

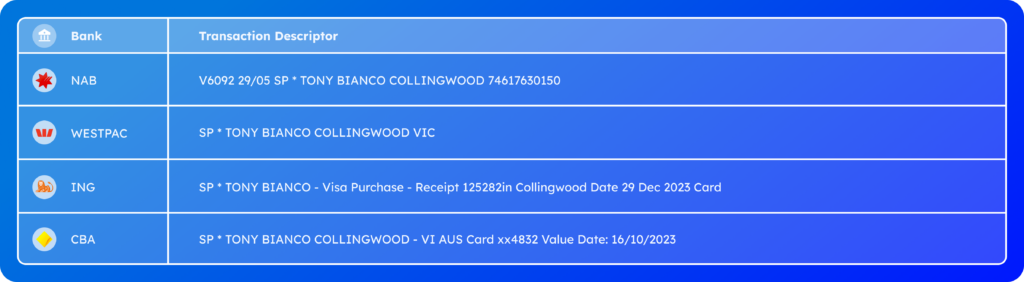

- Lack of standardisation: Each bank may have different formats and data availability, complicating the assessment process for lenders who deal with multiple banks.

- Compliance and accuracy concerns: Ensuring that the bank statements are compliant with regulatory requirements and accurately reflect the customer’s financial status is paramount, yet challenging due to varying data quality.

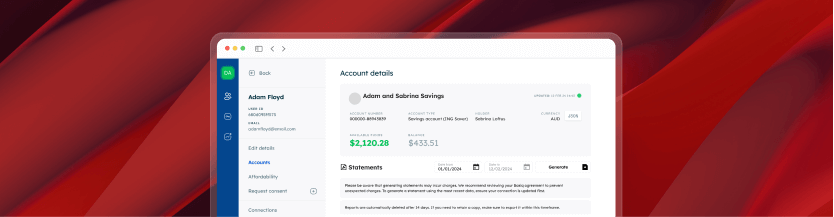

Bank Statements; a Basiq Insights solution

To address these industry-wide challenges, Basiq’s Bank Statements innovate on how financial assessments are conducted and shared with banks. Bank Statements compliments our existing Insights Affordability solution, providing a seamless and efficient method for generating accurate, compliant bank statements for lenders.

Key Features of Basiq’s Bank Statements

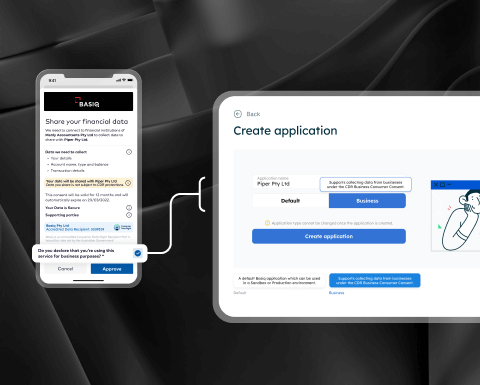

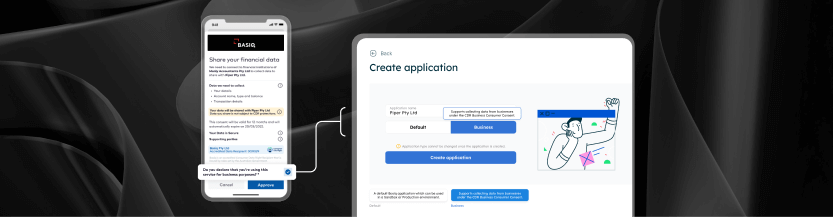

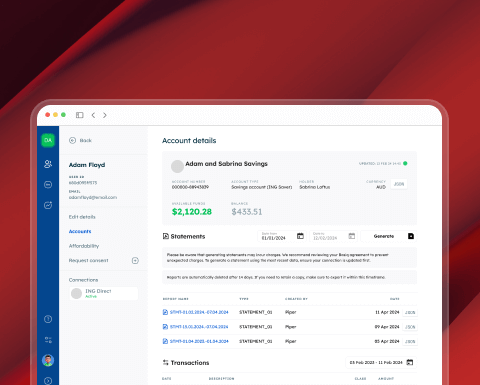

- Access via API or our no code dashboard: Basiq’s Bank Statements can be generated through two convenient methods: via our robust API for seamless integration into existing systems, or through our intuitive no-code dashboard, which allows partners to generate and download statements in a PDF or JSON format without any technical expertise.

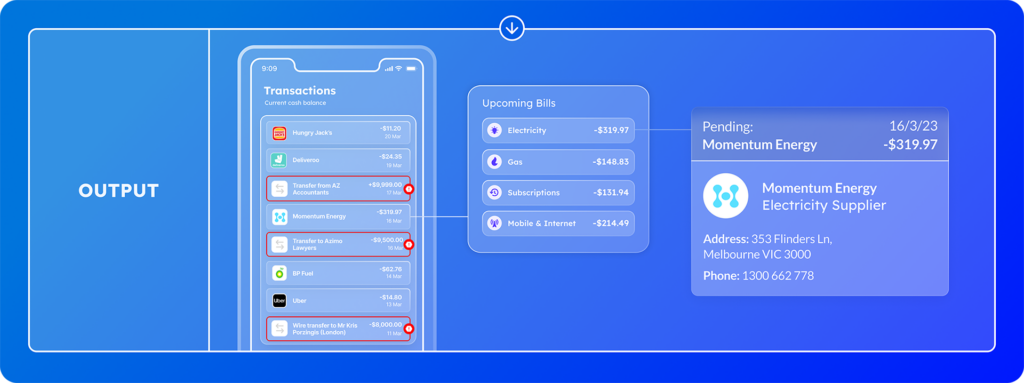

- Single account focus: Tailors statements for individual or joint accounts while presenting details clearly and compliantly.

- Custom date ranges: Enables customisation of the statement period by allowing users to easily select how far back they want to go, with the ‘To Date’ automatically set to the date the account was last refreshed to ensure the data is timely and relevant.

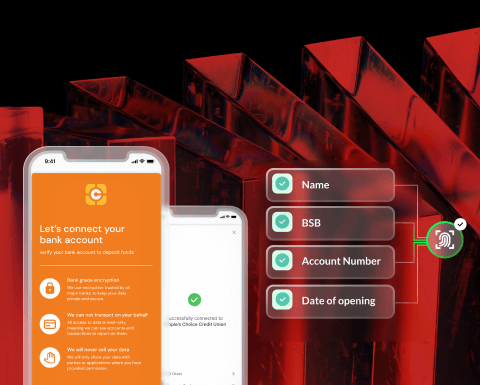

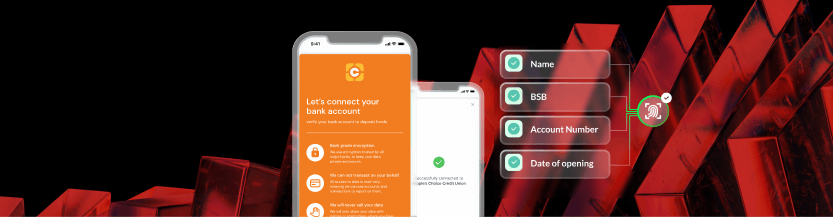

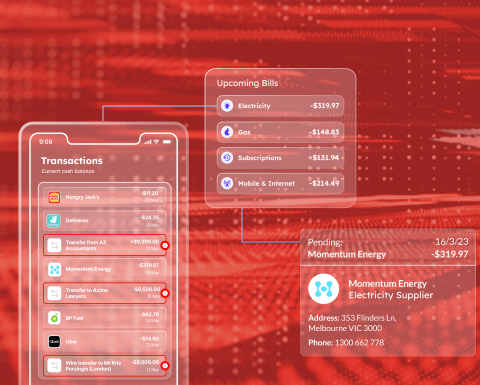

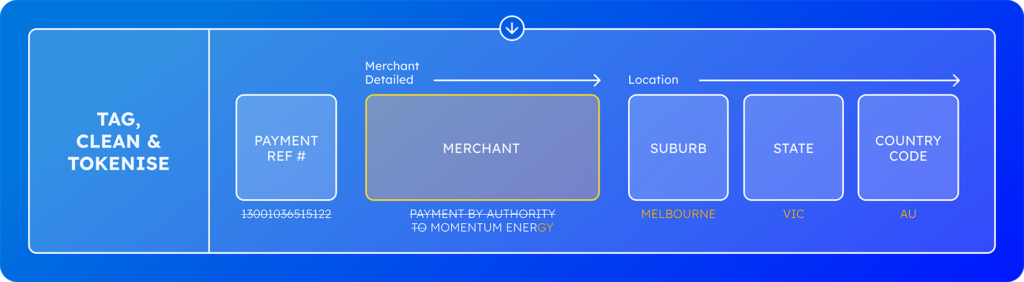

- Logical running balances: Calculates logical running balances based on the transaction order, providing a comprehensive financial overview even when CDR data lacks a running balance.

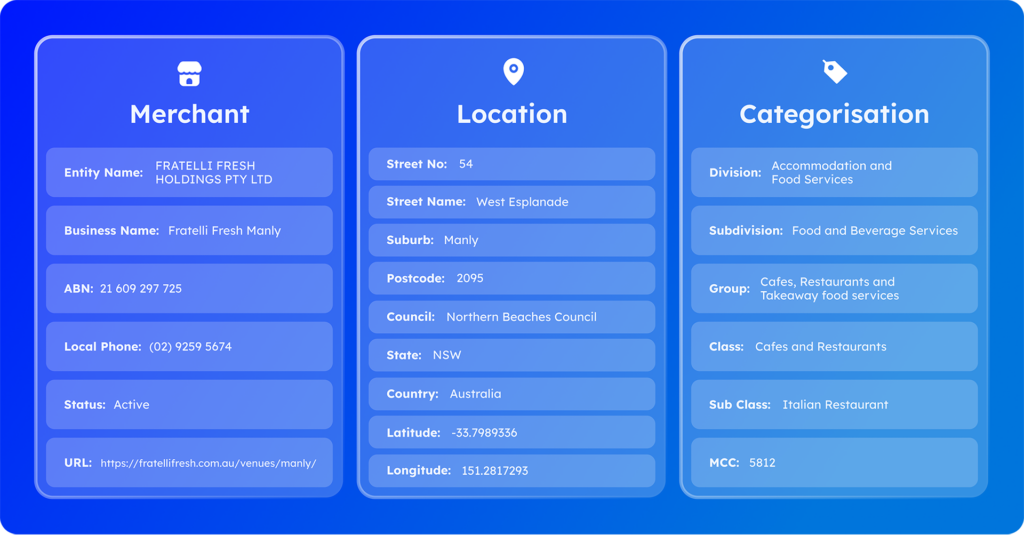

- Accreditation and Branding: Includes the logo and accreditation details of the institution, enhancing trust and credibility in the statements provided.

Basiq’s Bank Statements is an exciting step in the journey towards making financial processes more efficient and less burdensome for lenders. By addressing the key pain points in traditional bank statement processes, it enhances both the speed and quality of financial assessments, empowering our customers to make faster and more informed lending decisions.

Developer Resources

Explore our Basiq developer resources to understand more how you can integrate bank statements into your solution.

Important Information: This article has been prepared by Basiq Pty Ltd (ABN 95 616 592 011) (Company), and was originally published on 3 May 2024 on www.basiq.io. Information is current as at the publication date, and the Company has no obligation to update or correct this article. The information contained in this article is of a general nature and is not intended to address the objectives or needs of any particular individual entity, and should not be regarded in any manner as advice. To the extent permitted by law, the Company and its related bodies corporate will not be liable for any errors, omissions, defects or misrepresentations in the information in this article or for any loss or damage suffered by persons who use or rely on such information (including for reasons of negligence, negligent misstatement or otherwise. © 2024 Basiq Pty Ltd